May 15, 2016

Picture the poor investor who leaves a meeting with their financial advisor followed by a Pig-Pen tangle of scribbled terms. Allocation, diversification, small cap, large cap, foreign and emerging markets, Treasuries, corporate bonds, real estate, and commodities. What happened to simplicity, they wonder? Paper route or babysitting money went into a savings account which earned interest and the account balance grew while they slept.

For those in retirement, it’s even worse. The savings, or accumulation, phase may be largely over but now the withdrawal phase begins and, of course, there needs to be a withdrawal strategy. Now there’s a gazillion more terms about withdrawal rates, maximum drawdowns and recovery rates, life expectancy, inflation and other mumbo jumbo that is more complicated than Donald Trump’s changing interpretations of his proposed tax plans.

Seeking simplicity, an investor might be tempted to put their money in a low cost life strategy fund or a target date fund, both of which put investing on automatic pilot. These are “fund of funds,” a single fund that invests in different funds in various allocations depending on one’s risk tolerance. There are income funds and growth funds and moderate growth funds within these categories. For a target date fund, what date should an investor use? It is starting to get complicated again.

Well, strap yourself into the mind drone because we are about to go global. Hewitt EnnisKnupp is an institutional consulting group within Aon, the giant financial services company. In 2014, they estimated the total global investable capital at a little over $100 trillion as of the middle of 2013. Let’s forget the trillion and call it $100.

Could an innocent investor take their cues from the rest of the world and invest their capital in the same percentages? Let’s look again at the categories presented by the Hewitt group. The four main categories, ranked in percentages, that jump off the page are:

Developed market bonds (23%),

U.S. Equities (18%),

U.S. Corporate Bonds (15%),

and Developed Market equities (14%).

The world keeps a cushion of investable cash at about 5% so let’s throw that into the mix for a total of 75%. Notice how many categories of investment there are that make up the other 25% of investable capital!

In the interest of simplification let’s consider only those four primary categories and the cash. Adjusting those percentages so that they total 100% (and a bit of rounding) gives us:

Developed Market bonds 30%,

U.S. Corporate Bonds 20%,

U.S. Equities 25%

Developed Market equities 19%,

Cash 6%.

Notice that this is a stock/bond mix of 44/56, a bit on the conservative side of a neutral 50/50 mix. Equities make up 44%, bonds and cash make up 56%.

I’ll call this the “World” portfolio and give some Vanguard ETF and Mutual Fund examples. Symbols that end in ‘X’, except BNDX, are mutual funds. Fidelity and other mutual fund groups will have similar products.

International bonds 30% – BNDX, and VTABX, VTIBX

U.S. Corporate Bonds 20% – BND and VBTLX, VBMFX

U.S. Equities 25% – VTI and VTSAX, VTSMX

Developed Market equities 19% – VEA and VTMGX, VDVIX

According to Portfolio Visualizer’s free backtesting tool this mix would have produced a total return of 5.41% over the past ten years, and had a maximum drawdown (loss of portfolio value) of about 22% during this period. For a comparison, an aggressive mix of 94% U.S. equities and 6% cash would have generated 7.06% during the same period, but the drawdown was almost 50% during the financial upheaval of 2007 – 2009.

There have been two financial crises in the past century: the Great Depression of the 1930s and this latest Great Recession. If the balanced portfolio above could generate almost 5-1/2% during such a severe crisis, an investor could feel sure that her inital portfolio balance would probably remain intact during a thirty year period of retirement. During a horrid five year period, from 2006-2010, with an annual withdrawal rate of 5%, the original portfolio balance was preserved, a hallmark of a steady ship in what some might call the perfect storm.

Finally, let’s look at a terrible ten year period, from January 2000 to December 2009, from the peak of the dot com bubble in 2000 to the beaten down prices of late 2009, shortly after the official end of the recession. This period included two prolonged slumps in stock prices, in which they lost about 50% of their value. A World portfolio with an initial balance of $100K enabled a 5% withdrawal each year, or $48K over a ten year period, and had a remaining balance of $90K. Using this strategy, one could have withdrawn a moderate to aggressive 5% of the portfolio each year, and survived the worst decade in recent market history with 90% of one’s portfolio balance still intact.

Advisors often recommend a 4% annual withdrawal rate as a conservative or safe rate that preserves one’s savings during the worst of times and this strategy would have done just that during this worst ten year period. Retirees who need more income than 4% may find the World portfolio a conservative compromise.

{ For those who are interested in a more granular breakdown of sectors within asset classes, check out this 2008 estimate of global investable capital.}

////////////////////////////

Productivity

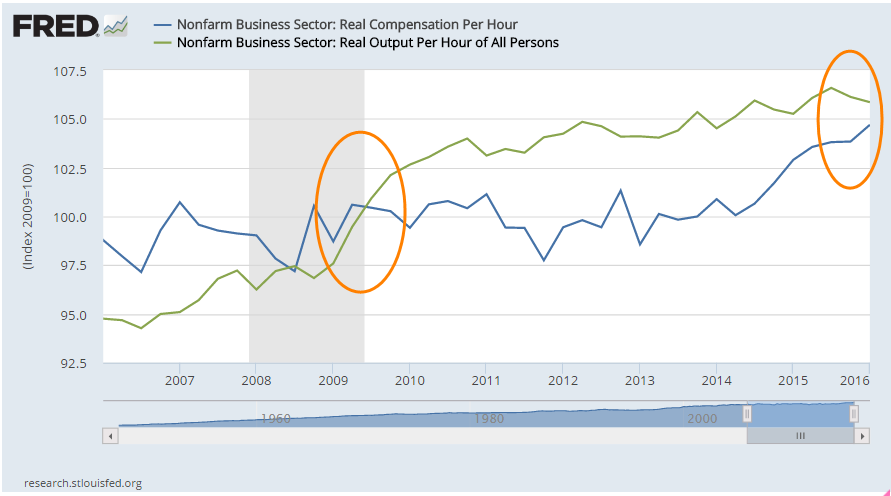

In a recent article, Jim Zarroli with NPR compared productivity growth with the weak growth of only the wages component of employee compensation. He did leave out an increasingly big chunk of total employee compensation: Federal and State mandated taxes, insurances and benefits. Since these are mandated costs, the income is not disposable. A term I have never liked for this package of additional costs and benefits is “employer burden.” The burden is really on the employee as we will see.

In the graph below are two indexes: total compensation per hour and output per hour. At the end of the last recession in the middle of 2009, the two indexes were the same. Seven years later, output is slightly higher than total compensation but the discrepancy is rather small compared to the dramatic graph difference shown in the NPR article. As output continues to level and compensation rises more rapidly, we can expect that compensation will again overtake output.

Over the past several decades, employees have voted in the politicians who promised more tax-free insurances and benefits. While the tax-free aspect of these benefits is an advantage, some employees may think they are freebies. Payroll stubs produced by more recent software programs enable employers to show the costs of these benefits to employees, who are often surprised at the amount of dollars that are spent on their behalf. While these benefits are welcome, they don’t pay school tuition, the rising costs of housing or repairs to the family car.

Many voters thought they could have it all because some politicians promised it all: more tax-free insurances and benefits, and higher disposable income. Total employee compensation, though, must be constrained by productivity growth. In the coming decade, legislators will put forth alternative baskets of total compensation. More benefits and insurances means less disposable income but a politician can not just say that outright and get re-elected. More disposable income means less insurances and benefits, which will anger other voters. In short, the political discourse in this country promises to only get more contentious.

You should read Tony Robbins' book “Money: Master the game.” He interviews approximately 50 of the world's best money managers to see how they do it. I think you'd be surprised at their balanced portfolio recommendations.. and how some of them just completely throw that out the window.

LikeLike

Brian,

This reviewer {https://investorjunkie.com/38192/money-master-game-review/} was not impressed with Robbin's book although there were a few takeaways that he noted. A 15% allocation to commodities and gold suggested in Robbin's book doesn't seem appropriate for an investor who wants to keep it simple and understandable. A reviewer at Market Watch {http://www.marketwatch.com/story/tony-robbins-doesnt-quite-master-the-game-of-money-in-his-new-book-2014-11-25} did not like some of the contradictions in the book, saw a few things that he did appreciate but couldn't recommend the book. You thought the 600 page read was worth it?

LikeLike