Ignorance has one virtue: persistence. – John Kramer, Blythe

September 23, 2018

by Steve Stofka

Ten years ago, the financial world cracked. Job losses during the first eight months of 2008 were definite signs of recession, but this correction to an overheated housing market had been expected for two years. In July 2008 came the news that June’s job losses had eased. The average duration of a post-WW2 recession was eight months, so the correction was nearing an end. More worrying were the high gas prices, which had topped $4 per gallon. Beginning in mid-July, the stock market rose more than 5% and traded in a consolidation level through August.

In early September, the market lost 3% when August job losses worsened. Within a week, the market recovered those losses and closed on Friday, September 12th at the consolidation level it had been at during August. Over that weekend, the Federal Reserve, U.S. Treasury and other banking agencies tried to arrange a rescue of the investment firm Lehman Brothers.

On September 15th, the world learned of the firm’s collapse. Within hours, the market lost almost 5% of its value, more than the market may gain or lose in a year. In busy urban areas, people stopped to stare at the market’s extraordinary volatility displayed on storefront TV screens. There were more such days to come. Over the next two weeks of turbulent price swings, the market stabilized at its mid-July low, closing September just below 11,000.

What stabilized the market in those closing days of September? On September 30th, the N.Y. Times reported that the Securities and Exchange Commission (SEC) might suspend a newly implemented FASB international accounting standard SFAS 157 (Note #1 and #2). This accounting rule required financial institutions to value loans and other assets on their books at market value, not by the present value of future cash flows (Note #3). In turbulent markets, when raw fear is the auctioneer, market prices do not reflect the future value of assets.

After a TARP bill (Note #4) failed to pass Congress on the first go, there would be another attempt by the end of the first week in October. Neither the Congress or the administration could summon the political will to temporarily suspend the accounting rule. The TARP bill that President Bush signed on Saturday, October 3rd, required only that the SEC study the accounting rule.

Investors ran for the exits. The financial carnage may have happened in September, but the market implosion happened in October. In seven consecutive days in early October, the Dow Jones Industrial Average lost almost 23% of its value (Note #5). Did an accounting standard cause the financial crisis? No, but it did intensify negative investor reaction to the financial crisis, which exacerbated the crisis in a negative feedback loop.

In early March 2009, after the market had lost 40% of the value it had in early October 2008, the FASB announced that they would modify the standard a month later (Note #6). By the time that modification was implemented on April 9, 2009, the SP500 had risen 20%.

Could the Bush administration have eased the response to the crisis? Yes. Did accounting standards cause the financial crisis? No. Can we expect another crisis sooner rather than later? Yes. Central bankers and Federal agencies that supervise the banking system cannot fully monitor modern credit markets in real time. When the horses are spooked, regulators sitting in the driver’s seat may hold the reins but have little control of the panicked animals.

Investors who maintain some balance in their savings portfolio can weather these market catastrophes. 50% market falls have occurred only three times in the past fifty years (Note #7). Investors with long time horizons can afford to take a less balanced approach.

//////////////////////

1. The FASB is a privately held international organization that sets accounting standards. Fair Value Accounting standard SFAS157 (“mark to market”) is one of their standards, implemented in 2006. An explanation of the standard from FASB in May 2008, before the crisis.

2. Suspension of the SFAS 157 standard would have allowed banks to report higher profits and relieve some of the capital pressures on bank balance sheets. Sept. 30th NY Times article.

3. FDR suspended mark-to-market accounting in 1938. See this March 2009 article for a review of the issue.

4. TARP – The Troubled Asset Relief Program was a compilation of many programs designed to support the automotive, housing and financial industries. On page 11, a reminder of the corruption of Wall Street and the incompetence in Washington. “In March 2009, after receiving $170 billion in federal bailout money with another $30 billion pending, AIG announced a $165 million bonus payout to executives. Despite the bailout and the U.S. government having ownership control, AIG management thought it was prudent to pay executive bonuses in a financially struggling company. The U.S. government lacked the oversight to assure efficient use of taxpayer bailout funds.”

5. The sharp fall in October was the second sharpest decline since World War 2. The leader is the October 1987 crash, when the market lost 28% in four days. What about the dot-com bust? Over 2-1/2 years, the market lost half its value but there wasn’t a decline of more than 20% during that market fall. The strongest decline began in February 2001 and took 34 trading days to lose 18%.

6. An article from the Harvard Business Review in November 2009.

7. 50% market falls: The gas crisis of 1973-74, the dot-com bust of 2000 – 2003, and the mortgage and financial crisis of 2007-2009. Less severe falls came in 1966, 1969-70, 1977-78, 1982, 1987, 1990, and 2011. These were all more than 20% drops in market value.

/////////////////////////

Misc

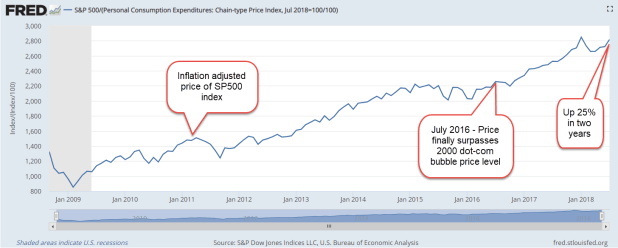

In mid-2016, the inflation-adjusted price of the SP500 index finally rose above its price at the start of the century. The price has risen 25% since then.