August 31, 2014

As summer comes to a close and the sun drifts south for the winter, the porridge is not too hot or too cold.

********************

Coincident Index

The index of Leading Indicators came out last week, showing increased strength in the economy. Despite its name, this index has been notoriously poor as a predictor of economic activity. The Philadelphia branch of the Federal Reserve compiles an index of Coincident Activity in the 50 states, then combines that data into an index for the country.

This index is in the healthy zone and rising. When the year-over-year percent change in this index drops below 2.5%, the economy has historically been on the brink of recession. The index turns up near the end of the recession, and until the index climbs back above the 2.5% level, an investor should be watchful for any subsequent declines in the index.

As with any historical series, we are looking at revised data. When this index was published in mid-2011, the percent change in the index was -7% at the recession’s end in mid-2009. Notice that the percent drop in the current chart is a bit less than 5%. This may be due to revisions in the data or the methodology used to compile the index.

**************************

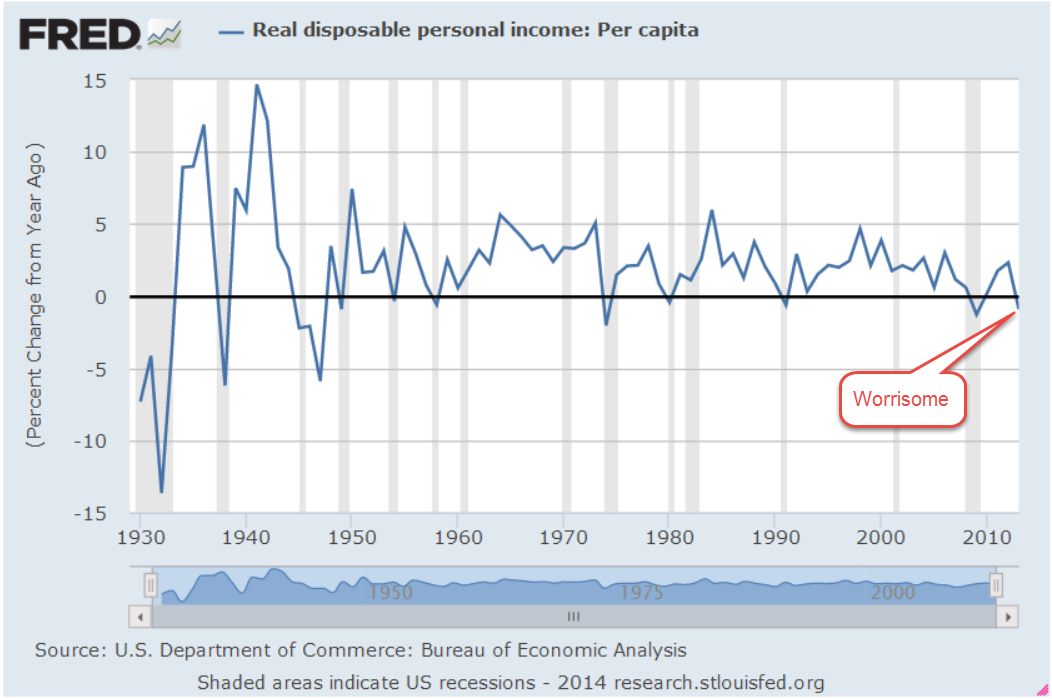

Disposable Income

The Bureau of Economic Analysis (BEA) produces a number of annual series, which it updates through the year as more complete data from the previous year is received. 2013 per capita real disposable income, or what is left after taxes, was revised upward by .2% at the end of July but still shows a negative drop in income for 2013. While all recessions are not accompanied by a negative change in disposable income, a negative change has coincided with ALL recessions since the series began at the start of the 1930s Depression.

Many positive economic indicators make it highly unlikely that we are either in or on the brink of recession. Clearly something has changed. Something that has routinely not been counted in disposable personal income is having some positive effect on the economy. In 2004, the BEA published a paper comparing the methodology they use to count personal income and a measure of income, called money income, that the Census Bureau uses. What both measures don’t count in their income measures are capital gains.

Unlike BEA’s measure of personal income, CPS money income excludes employer contributions to government employee retirement plans and to private health and pension funds, lumps-sum payments except those received as part of earnings, certain in-kind transfer payments—such as Medicare, Medicaid, and food stamps—and imputed income. Money income includes, but personal income excludes, personal contributions for social insurance, income from government employee retirement plans and from private pensions and annuities, and income from interpersonal transfers, such as child support. (Source)

Analysis (Excel file) of 2012 tax forms by the IRS shows $620 billion in capital gains that year, about 5% of the $12,384 billion in disposable personal income counted by the BEA. An acknowledged flaw in the counting of disposable income is that the total reflects the taxes that individuals pay on the capital gains (deducted from income) but not the capital gains that generated that taxable income. Although 2013 data is not yet available from the IRS, total personal income taxes collected rose 16%. We can suppose that the 30% rise in the stock market generated substantial capital gains income.

*************************

Interest

Every year the Federal Government collects taxes and spends money. Most years, the spending is more than the taxes collected – a deficit. The public debt is the accumulation of those annual deficits. It does not include money “borrowed” from the Social Security trust fund as well as other intra-governmental debt, which add another third to the public debt. (Treasury FAQ) This larger number is called the gross debt. At the end of 2012, the public debt was more than GDP for the first time.

The Federal Reserve owns about 15% of the public debt. But wait, you might say, isn’t the Federal Reserve just part of the government? Well, yes it is. Even the so-called public debt is not so public. How did the Federal Reserve buy that government debt? By magic – digital magic. There is a lot of deliberation, of course, but the actual buying of government debt is done with a few dozen keystrokes. Back in ye olden days, a government with a spending problem would have to melt down some of its gold reserves, add in some cheaper metal to the mix and make new coins. It is so much easier now for a government to go to war or to give out goodies to businesses and people.

Despite the high debt level, the percent of federal revenues to pay the interest on that debt is relatively low, slightly above the average percentage in the 1950s and 1960s but far below the nosebleed percentages of the 1980s and 1990s.

As the boomer generation continues to retire, the Federal Government is going to exchange intra-governmental debt, i.e. the money the government owes to the Social Security trust funds, for public debt. As long as 1) the world continues to buy this debt, and 2) interest rates stay low, the impact of the interest cost on the annual budget is reasonable. However, the higher the debt level, the more we depend on these conditions being true.

************************

Watch the Percentages

As the SP500 touched and crossed the 2000 mark this week, some investors wondered whether the herd is about to go over the cliff. The blue line in the chart below is the 10 month relative strength (RSI) of the SP500. The red line is the 10 month RSI of a Vanguard fund that invests in long term corporate and government bonds. Readings above 70 indicate a strong market for the security. A reading of 50 is neutral and 30 indicates a weak market for the security. The longer the RSI stays above 70, the greater the likelihood that the security is getting over-bought.

Long term bonds tend to move in the opposite direction of the stock market. While they may both muddle along in the zone between 30 and 70, it is unusual for both of them to be particularly strong or weak at the same time. We see a period in 1998 during the Asian financial crisis when they were both strong. They were both weak in the fall of 2008 when the global financial crisis hit. Long term bonds are again about to share the strong zone with the stock market.

Let’s zoom out even further to get a really long perspective. Since November 2013, the SP500 index has been more than 30% above its 4 year average – a relatively rare occurrence. It happened in 1954 – 1956 after the end of the Korean War, again in December of 1980, during the summer months of 1983, the beginning of 1986 to the October 1987 crash, and from the beginning of 1996 through September 2000.

In the summer of 2000, the fall from grace was rather severe and extended. In most cases, including the crash of 1987, losses were minimal a year after the index dropped back below the 30% threshold. When the market “gets ahead of itself” by this much, it indicates an optimism brought on by some distortion. It does not mean that an investor should panic but it is likely that returns will be rather flat over the following year.

The index rarely gets 30% below its 4 year average and each time these have proven to be excellent buying opportunities. The fall of 1974, the winter months of 2002 – 2003, and the big daddy of them all, March 2009, when the index fell almost 40% below its 4 year average.

************************

GDP

The Bureau of Economic Analysis (BEA) released the 2nd estimate of 2nd quarter GDP growth and surprised to the upside, revising the inital 4.0% annual growth rate to 4.2%. As I noted a month ago, the first estimate of 2nd quarter growth included a 1.7% upward kick because of a build up of inventory, which seemed a bit high. The BEA did revise inventory growth down to 1.4% but the decrease was more than offset primarily by increases in nonresidential investment. A version of GDP called Final Sales of Domestic Product does not include inventory changes. As we can see in the graph below, the year-over-year percent gain is in the Goldilocks zone – not strong, but not weak.

New orders for durable goods that exclude the more volatile transportation industries, airlines and automobiles, showed a healthy 6.5% y-o-y increase in July. Like the Final Sales figures above, this is sustainable growth.

***********************

Takeaways

Economic indicators are positive but market prices may have already anticipated most of the positive, leaving investors with little to gain over the following twelve months.