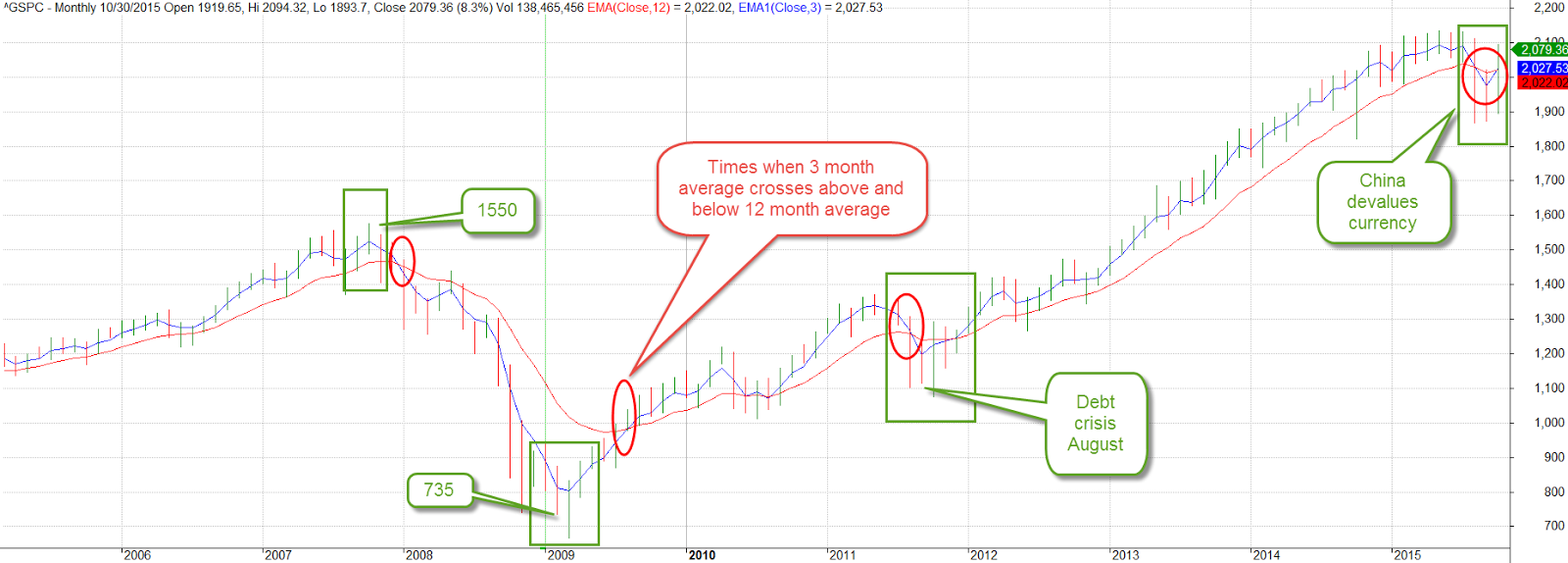

November 29, 2015

Obamacare

United Healthcare (UNH), the largest health insurance carrier in the U.S., announced that they may drop out of the state health care exchanges at the end of 2016. The CEO indicated that it would review costs again in mid-2016 but was concerned that continuing losses on the state exchange plans would simply make it uneconomical for UNH to continue to offer these plans.

UNH says it has evidence of many individuals gaming the system by coming into and out of the health insurance system when they need medical services. {Bloomberg and Market Watch} It is not clear how patients would do this since the health care exchanges have enrollment rules similar to Medicare. These restrictions are designed to make it difficult for individuals to game the system. Are those rules being implemented consistently on the state level? If the policy rules are in place, have the screening algorithms been reviewed? Poor implementation and oversight have plagued some exchanges.

At the heart of Obamacare is the projection that costs for the newly insured stabilize after approximately two years, a metric derived from long experience with Medicare patients. Individuals who have not had regular medical care often have chronic unattended conditions which need to be stabilized. Medicare costs typically rise during this initial stage before leveling off.

Obamacare will certainly be an issue in the upcoming Presidential election. The debate will intensify if other insurers express doubts about the economic feasibility of the system,

************************

Productivity and Policy

Economists and policy makers continue to debate the causes, and solutions, for the slowdown in labor productivity that has occurred over the past several decades. Larry Summers served as Treasury Secretary under President Clinton, Director of the National Economic Council under President Obama, and Chief Economist at the World Bank. In other words, the guy’s got some chops.

In a recent speech Summers noted several trends:

1) Dis-employment of unskilled workers. The participation rate of those aged 25 – 54 has declined from 95% in 1965 to 85% now. (p. 3) While this is often attributed to technical improvements, Mr. Summers makes the case that labor productivity should go up, not down, due to technical change. That is not the case. Summers says he doesn’t have the answer either but the contradiction between theory and data indicates that economists still don’t understand the underlying processes. (p. 4)

2) Mismeasurement. Productivity measures are based on the calculation of real GDP which is dependent on the measure of inflation. Summers asks whether differences in quality, or what are called hedonic measures, are captured in CPI data. He asks “Which would you rather have for you and your family, 1980 healthcare at 1980 prices or 2015 healthcare at 2015 prices? How many people would prefer 2015 healthcare at 2015 prices?” If people prefer the 2015 variety at 2015 prices then inflation has been negative in healthcare. As a percent of GDP, healthcare spending has increased. Mismeasuring inflation in healthcare may negate all or most of this increase. (p. 5)

3) As we have transitioned to an economy dominated by services, mismeasurement of inflation has probably increased. A leading technocat in Democratic administrations, Summers casts doubts on a staple of liberal rhetoric – that median family income has not changed since 1973. This idea is a central tenet of Bernie Sanders presidential campaign. What if the measurement of median family income is flawed? This doubt is more often raised by conservative economists and policy makers. Summers’ remarks crossed the ideological and political divide and surely raised a few eyebrows. (p. 6)

4) Developing the theme of measurement as it pertains to different types of economies, Summers refers to several statistical terms like “unit root” stationarity that may challenge casual readers.

When a time series (data observations over time like GDP) has a unit root it exhibits more deterministic behavior; it is more likely to adopt an altered path or trendline when shocked off its previous path.

Series without a unit root are more likely to exhibit stochastic behavior when subjected to some shock; that is, they will tend to return to their former path or trendline, not form a new trendline.

At mid-century, when our economy was much more reliant on manufacturing, it behaved in a stochastic way when subjected to economic shocks. It rebounded to a previous trendline. Our economy is now overwhelmingly service oriented, about 88%. Summers makes the case (p. 9) that unbalanced economies like ours behave differently than a more balanced economy. The growth path of GDP changes permanently in response to an economic shock like the financial crisis of 2008. If that is the case, policy changes will be ineffective in returning GDP and employment back to the former trendline. (For more info on testing the deterministic and stochastic components of time series processes, see this).

Summers adds to the number of voices calling for a more accurate – but also objective – measurement of inflation. Poor measurement leads to imprecise data leads to inaccurate conclusions leads to ineffective policy leads to more problems leads to…

Policy debates often involve complicated issues of identification, measurement, and methods of analysis that are not readily explainable in a campaign speech. On our way home from work, a complicated system of algorithms based on traffic data determines whether the traffic lights continue to trip green as we maintain a constant speed. Much of this is hidden from us and incomprehensible to most of us. All of that complexity is boiled down to a simple heuristic: we go when it’s green, stop when it’s red.

Voters like simple. The job of a politician is to convince voters and donors that if they are elected, they will implement the right policies, the correct algorithms that will move traffic, i.e. the economic fortunes of the families of America, faster.