November 28, 2021

by Stephen Stofka

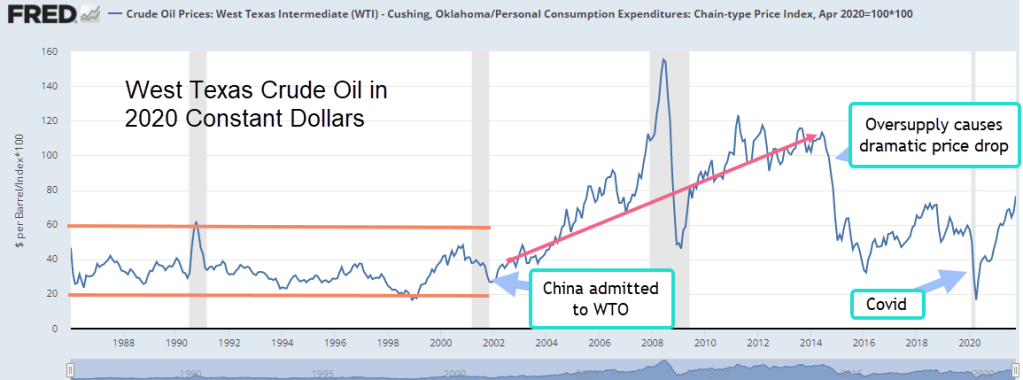

On Friday, fears of another wave of Covid lockdowns caused a sharp decline in equity and commodity prices worldwide. The decline was fueled by short-term traders who did not want to hold their positions over the holiday weekend and sold into a thin market. Crude oil prices fell 12% and closed the day below $70, and below the price of oil in the summer and early fall of 2018. Did we forget how high prices were just a few years ago? Rising oil prices helped fuel voter discontent that Democrats rode to take back control of the House that year.

Below is a graph of West Texas Intermediate, one of two oil benchmarks used domestically and shipped around the world. The price is adjusted to 2020 constant dollars.

As the price of oil broke out of its price channel in the early 2000s, companies began to develop more effective horizontal drilling techniques (Mead & Stiger, 2015, 4). In 2013, U.S. production reached a 24-year high and both political parties claimed credit. Oversupply led to a 50% price decline in 2014. Drivers liked the prices at the pump but states which had enjoyed the boom were hurt by the bust. Republican candidates promised better times in these red states if they were elected.

In a democracy, politicians must play a game of voter persuasion. They spend millions in opinion polls to test the temperature of voter passions, to discover the emotional buttons that will win votes. They rig Congressional districts to maximize the voter sentiment in one party’s favor. Like heralds marching into battle, candidates wave their principles and values for all to see. We have chosen this system, this political game, as the best alternative to armed conflict in the streets. Many of us were alarmed when the January 6th rioters championed a return to the violence that shook the foundations of civil society in France during the 19th century. Seventy years of successive revolts in that country left many bodies in the streets. We have far more sophisticated weapons and lots of them. Do we want that bloodbath?

As bread was a rallying cry in the French Revolution, the price of oil sparks political passions in the U.S. Higher prices impact rural folk more than urban residents, blue collar businesses more than white collar firms. When workers have to pay $100 – $200 to fill up a 40 gallon tank on a service truck, they complain. If their party is in power, it’s the fault of speculators and they will soon forget the pain when prices decline. Voters protest loudest at high oil prices when their party is not in power. Politicians promise that their policies will bring down oil prices. They know their promises are as real as unicorns but voters like unicorns and fairy tales.

///////////////////

Photo by David Thielen on Unsplash

Mead, D., & Stiger, P. (2015). The 2014 Plunge in Import Petroleum Prices: What Happened. BSL: Beyond The Numbers, 4(9), 1-8. Retrieved November 27, 2021, from https://www.bls.gov/opub/btn/volume-4/pdf/the-2014-plunge-in-import-petroleum-prices-what-happened.pdf