It’s the beginning of the year and I am cleaning up – not the house, but my notes – scribbles of factoids which I, and maybe you will as well, find interesting. Those of you who like graphs will be disappointed this week. 😦

In 2009, 55% of income in the S&P500 companies was generated overseas.

The Eurozone is set up very similar to the Senate in the U.S. Despite being 30% of the Euro economy, Germany only has one vote.

It will cost an estimated $175B for the payroll tax cut in 2012.

A rule of thumb that the Congressional Budget Office (CBO) uses – 1/10% of GDP growth over 10 years = $300B in revenues over 10 years to the Federal Government.

One of the problems with the federal mortgage agencies FHA, Freddie Mac and Fannie Mae is that they buy mortgages which originate in states where there is little or no regulation. If people want a government agency buying mortgages, why don’t the various states institute such agencies?

A CNN article about doctors going broke:

http://money.cnn.com/2012/01/05/smallbusiness/doctors_broke/index.htm?iid=Popular

This year, 2011, the USDA estimates that for the first time, this country will produce more corn for fuel than for food.

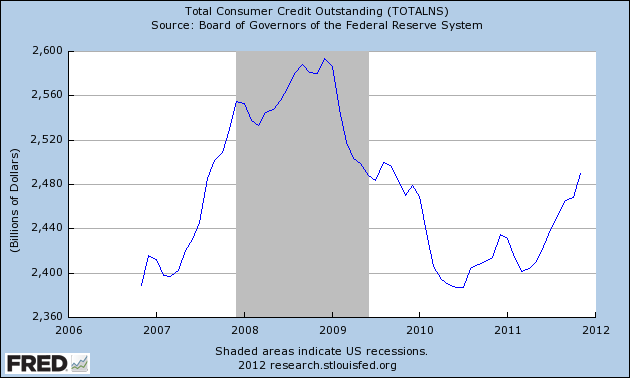

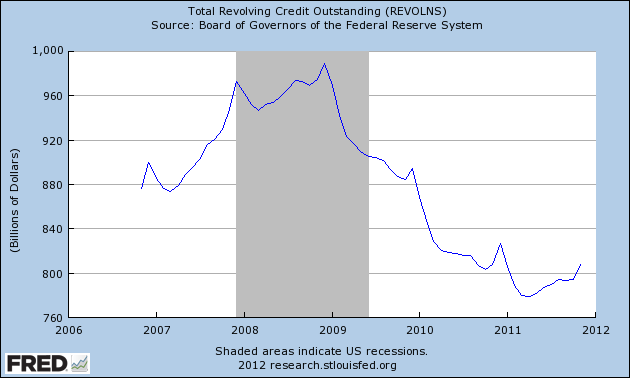

In 2009, total lending by U.S. banks fell 7.4%, the steepest drop since 1942. As of March 15, 2010, approximately half of Obama’s $787 billion stimulus program had been distributed but the flow of federal money into the economy could not keep up with the $700 billion that banks pulled out of the economy in the 6 months from mid-September 2008 to mid-March 2009.

Small companies, those with fewer than 100 employees, accounted for 45% of net jobs created from 1992 through the end of 2007, according to Labor Dept data.

In the U.S., diabetes costs about $174 billion annually in medical costs and lost production In the U.S., according to the American Heart Association. That is a little more than a 1% impact in a $15 trillion economy, or about 25% of the defense budget.

This past week, Standard and Poors downgraded the credit ratings of nine countries in the Eurozone. In assessing sovereign credit, Moody’s, another leading credit ratings firm, uses a metric called “debt reversibility margin.” This measures a government’s ability and willingness to get their debt level under control over the next five to seven years. Generally, it is the ratio of interest payments on a country’s debt to their revenues with a “benefit of the doubt” margin of 1 – 4% based on the resilience of the country’s economy, its politics and tax policies When this metric rises above 10%, Moody’s considers a downgrade to the country’s credit rating.

In 2008 New York spent $16K per student, top in the nation. It’s student-teacher ratio of 13.1 was the eighth lowest among the 50 states. From 2000 to 2009, the state added 15,000 teachers as student enrollment fell by 121,000 students.

Global warming is the latest in a series of hoaxes on the American people. Earlier scams include: smoking can kill you, lead in gasoline and paint is bad for children’s brains, chemical discharges in rivers and lakes are bad for your health, cholesterol is bad for your heart, smog is bad for your lungs, and acid rain is bad for trees and plants. In my lifetime, all of the above have been dismissed by critics at some point as scams on the American public.

In 2010, a USA Today analysis of data from the federal Office of Personnel Management showed that a federal worker makes 77% more than a private sector worker when benefits are included.

In 2010, the Boston Consulting Group issued its Global Wealth Report which found that the top 0.5% of households (those with $5 million or more) owned 21%, or $23 trillion, of global wealth, up from 19%.

A Goldman Sachs analysis of mortgage refinancing found that homeowners took out $358 billion in home equity loans in 2005, the most of any year.

J.P. Morgan Chase and two other banks now hold more than 33% of all U.S. deposits.

Based on 2007 data, the Energy Information Administration reported the various U.S. government subsidies per megawatt hour for the different sources for generating electric power. Coal got $.44, natural gas received $.25, nuclear enery $1.59 and the whoppers were solar at $24.34 and wind at $23.37 per MWH. Over the course of a year, at an average consumption of 10,000 KWH per year, a 100 homes will consume a MWH. In 2010, Google used the equivalent of 260 million homes of electricity.

When enacted in 1916, the income tax affected only the top 2% of incomes. With the popularity of beards and other creative facial hair statements among younger men, it might be time to resurrect an old Russian revenue raiser – a beard tax.

New York bills Medicaid about $2 million per year for each mentally disabled patient. The governor is reviewing the state’s billing procedures.

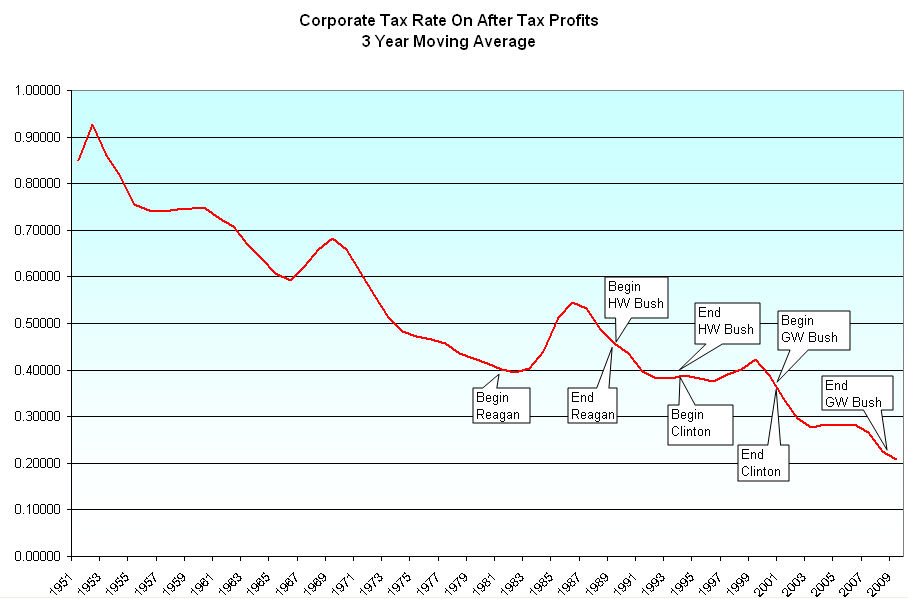

How much do all the tax breaks – or tax expenditures – cost the federal government? Health Insurance premiums not taxed – $659 billion, mortgage interest deduction – $484 billion, capital gains and dividends taxed at lower rates – $403 billion, pensions – $303 billion, earned income tax credit – $269 billion, charitable donations – $241 billion, state tax deductions – $237 billion, 401K plans – $212 billion, capital gains basis adjustment at death – $194 billion, social security benefits not taxed – $173 billion. The total is over $3 trillion, or almost the entire federal budget. If tax breaks were eliminated, the federal debt would be gone in 5 years.