March 25, 2018

by Steve Stofka

What a week it was. A glance at the headlines would lead someone to believe that it was all about tariffs and an impending trade war between the U.S. and China. On Thursday and Friday, the Dow Jones Industrial Average lost more than 1000 points, or almost 5%. Was that all about tariffs? Hardly.

As expected, the Federal Reserve raised interest rates ¼% on Wednesday. This put the Fed rate at 1.5% – 1.75%. Half of the members of the interest setting committee (FOMC) indicated that it might be necessary to raise interest rates four times this year. The market has been pricing in three interest rate increases for 2018. Until Thursday, a fourth increase had not been fully priced in.

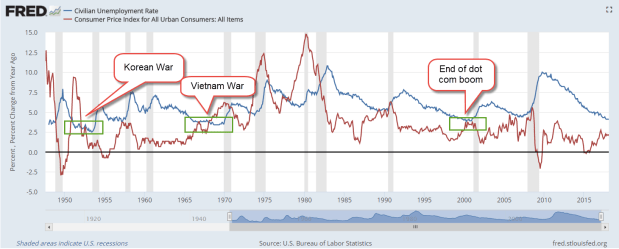

Further, the Fed is projecting an unemployment rate below 4% by late 2018 and early 2019. The current rate is 4.1%. Many industries are already struggling to find qualified workers. Rarely does the unemployment rate dip below 4%, and each time, inflation has risen and the stock market has fallen – sometimes substantially.

The downturn following the Korean War was short and shallow, but the other two periods of low unemployment were followed by steep corrections in the market.

On Thursday night, the White House tweety bird announced another change in the roster. Out with the old National Security Adviser, General H. R. McMaster. In with the new adviser, John Bolton, an old school war hawk who avoided military service in Vietnam by joining the National Guard. Bolton’s first instinct is war and regime change as a solution to global disputes. In choosing Mike Pompeo as his new Secretary of State and John Bolton as his new National Security Advisor, Trump has assembled a war cabinet. The market has still not priced in the heightened chances of conflict with North Korea or Iran. Nor has it recognized a greater likelihood of armed conflict with China in the South China Sea. That might come in the next few weeks.

On Thursday, Trump enacted tariffs on imported steel and aluminum from China as promised. Stronger action against China’s trade policies are overdue, as it has long violated the spirit, if not the letter, of the WTO global agreements. Car manufacturers wanting to set up a plant in China must have a Chinese business partner with a 25% stake and – surprise – access to industrial trade secrets. The national government heavily subsidizes key industries so that they can support their own industries and workers. They avoid labor and environmental regulations, and when caught, pledge to do better. They issue a national change in regulation, but the change is only published and enforced in a few local areas.

The theft of intellectual property is a hallmark of most developing nations like China. In the 18th and 19th century, the U.S. was notorious for copying products made by companies in England and France. Article 1, Section 8 of the Constitution added some promise of patent and copyright protection, but the laws instituted protected only U.S. citizens. A half century later, Charles Dickens was “one of the chief victims of American literary piracy” (Source). A foreign inventor had to establish citizenship or residency in the U.S. for two years to gain any patent protection. In 1887, the U.S. joined a 19th century version of the WTO called the Paris Convention. As China does today, the U.S. skirted international agreements for at least a decade (Patent history).

Older Chinese citizens may have watched patrolling U.S. naval ships from the shores of the Yangtze River. The nation remembers the century of U.S. gunboat diplomacy (Wikipedia article). Despite American free market rhetoric, Chinese leaders understand that mercantilism still retains a strong political influence in the trading policies of many developed countries, including the U.S.

When NAFTA was signed in the early 1990s, subsidies of American corn farmers enabled them to sell cheap corn to Mexico. Unable to compete, many farmers in northern Mexico went out of business. As farming jobs decreased in Mexico, many laborers journeyed north to the U.S. to pick crops so that they could support their families. The U.S. is partially responsible for creating the very environment that led to so much illegal immigration from Mexico.

Around the world, developed countries cry foul when another country subsidizes goods that are exported at a lower cost into their countries. Since 1963, the U.S. has imposed a protectionist tariff of 25% on imported light duty trucks, the so called “chicken tax”. Protected for over fifty years by this tariff, domestic truck manufacturers like Ford and Chevy had made few substantial changes to their work vans in the past few decades. In 2015, Ford finally made a substantial change to its F-150 pickup. Notice those Mercedes tall work vans on the road? They are built in Germany, disassembled to avoid the tariff, shipped to the U.S. and reassembled by U.S. workers. Ford uses the same process with its Transit Connect van.

Boeing imports parts from all over the world to build its Dreamliners. Chinese companies use southeast Asia as a manufacturing supply, then assemble and ship thousands of products to the U.S. and around the world. In the truly global manufacturing economy, a trade war is a threat to the profits of many large businesses. They have tuned their operations to the contradictory rules of international trade.

Business leaders understand the political strut of free trade. Each business wants free trade when it wants to compete in someone else’s market. Each business lobbies for more regulations, tariffs and barriers to protect its competitive position within its own market. Yes, it’s all lies, so it’s important that the rules underlying this game not change too much. Trade wars change the rules and that’s bad for business.