January 29, 2023

by Stephen Stofka

This week’s letter is about the debt ceiling. It has been ten days since Janet Yellen, Secretary of the Treasury, began using “extraordinary measures” to pay federal obligations as the nation waits for Congress to raise the debt ceiling. The U.S. is the only country in the world that requires legislative authorization of its debt after the legislature has already authorized the spending, then appropriated the money for that expense.

Each year, the federal government and each of the states conducts an annual appropriations process that allocates money to each state or federal department or agency. By law, states must balance their budgets – in a pro forma manner, at least. They sometimes employ accounting mechanisms to defer expenses to a later year or accelerate revenues into a current fiscal year to achieve that balance. The federal government does not have a balanced budget constraint but Congress does occasionally play a dangerous game of budget “chicken” when it wants to send a message to the other party.

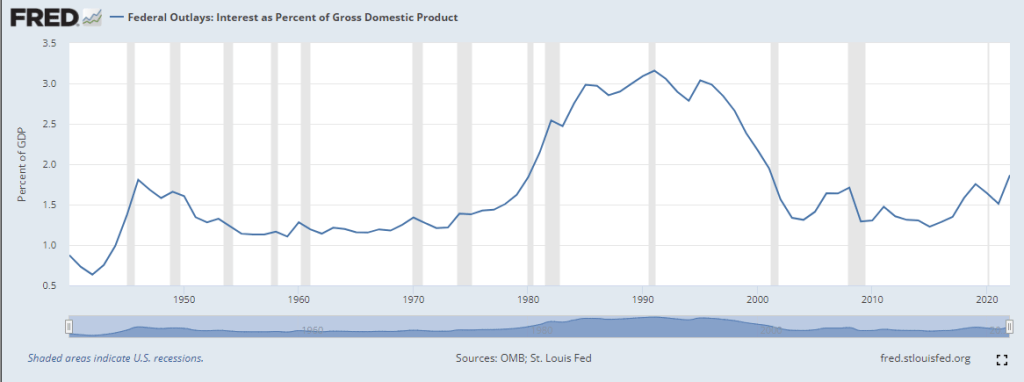

Political parties are ever conscious of their branding and each claims to be a good financial steward of the public’s taxes. Each claims that the other party is irresponsible. Paying the interest on the debt takes funding from other programs without doing anything. While this may be true and the interest on the debt is rising, it is less than 2% of GDP, far below the 2.5% – 3% of GDP during the 1980s and 1990s.

The press, politicians and public argue over who is responsible and whether to cut programs or increase revenues. When Republicans are out of power, as they are now, they call for spending cuts. Democrats call for revenue increases, particularly higher taxes on the rich. When Republicans were in power from 2017-2019, they increased the deficit each year, ending 2019 with a deficit of almost $1 trillion. In 2020, the deficit was $3.1 trillion. A month after the 2020 election was over, Congress added another $920 billion for Covid relief. The Trump administration added $6.5 trillion to the debt, or 21% of today’s total debt of $31 trillion.

Shortly after Mr. Biden took office in January 2021, Congress passed the American Rescue Act which provided another $1.9 trillion in relief. The two relief packages before and after the start of Biden’s term added up to $2.8 trillion and was responsible for the entirety of the 2021 deficit of $2.775 trillion. The Republican House will pin the blame for the debt on the Biden administration and programs like Social Security and Medicare. When a party is out of power, they can indulge in what is called position-taking. The firebrand rhetoric is popular with the Republican base and, since there is no possibility that those programs will be cut, politicians can claim to be prudent or for small government. When a party is actually in power, politicians have to be careful with political blustering. Their constituents are more likely to think that such cuts are possible and will vote them out of office.

For forty years, the Republican party has run on a theoretical assumption that tax cuts will spur enough economic activity that the increased tax revenue will more than pay for the cuts. There is no evidence supporting that claim but claims do not need evidence to be effective at raising funds and winning votes. For almost sixty years, Democrats have touted federal social programs as a path to greater equality and equitability.

In any game of chicken, the danger is that neither side gives in. Relying on estimates of income tax revenue in the next few months, some economists project that Secretary Yellen can continue to take ever more extraordinary measures until June. At the last big debt limit showdown in 2011, people argued over the constitutionality of the Treasury printing a $1 trillion coin and handing it over to the Federal Reserve to cover any expenses, including interest payments and bond redemption. This year, the idea is again a popular debating point on social media.

Like the filibuster, the debacle of the debt limit debate continues because each party wants to have power yet check the other party’s power, a dilemma that neither can escape. They are two horses harnessed together pulling the wagon of state. With reins in hand, the public is under the impression that it is driving the wagon but it is not. The parties pay attention only to the harness that binds each to the other.

/////////////////////

Photo by Jacek Ulinski on Unsplash