October 27th, 2013

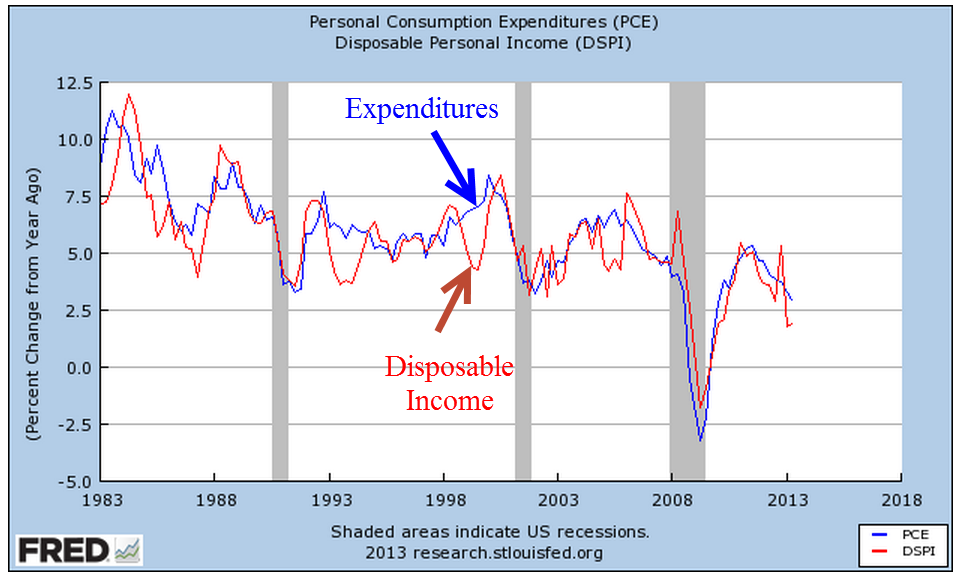

Before I take a short look at the delayed release of the employment report this week, let’s look at the growth in personal income and spending, which move in tandem. This is the y-o-y percent change in nominal after tax income and spending.

Income growth can be a bit more erratic than spending, bouncing around the more stable trend of spending.

The anemic growth in both income and spending has dampened hopes of a strong rebound of consumer spending. The ratio of an ETF composite of retail stocks versus the overall SP500 market index shows the recent doubt. Retail stocks have not participated in the larger market rebound.

A wholesale clothing sales rep I spoke with a week ago has noticed the caution in her buyers since mid-August. In September, some in the industry laid the blame at the prospect of a government showdown. For those of us in private business, the political shenanigans only muddy the water and make it difficult to read the consumer mood. Reports of sales at major retail centers – about 10% of retail sales – showed strength this week after a month of lackluster growth. Maybe it was the government shutdown.

However, the U. of Michigan Consumer Sentiment Index released this past Friday showed a sizeable drop in sentiment.

Was this decline in confidence due primarily to the shutdown or is this a forewarning of less than cheery holiday shopping season? The knuckleheads in Washington are like people who stand up at a concert, blocking the view of those seated behind them. The business community in general must plan around the politicians on both sides of the aisle in Washington who relentlessly pursue an anti-job agenda. Politicians can puff and posture on their principles – like so many in government service, they are not subject to the constraints and discipline of profit and loss. Sure, there are some whose intentions are good, who give their best effort but, unlike private business, their efforts and intentions are voluntary – a sense of personal virtue. Most will not lose their jobs because of a lack of performance. There are few incentives to improve efficiency. In fact, it is the reverse. The incentives are to promote more regulations, more layers of bureaucracy, as a program of job security and job growth in Washington at the expense of the rest of the country. Many of us in the private sector have the same sense of personal virtue but we also have that profit and loss whip.

Since the temporary resolution of the government shutdown and the raising of the debt ceiling, the market has shot up over 6% in twelve trading days. The late release of September’s labor report showed less than expected net job gains of 148,000, which dashed any further fears that the Fed might ease their bond buying program this year. The trends of employment growth have been fairly stable, with a few exceptions – health care, for one.

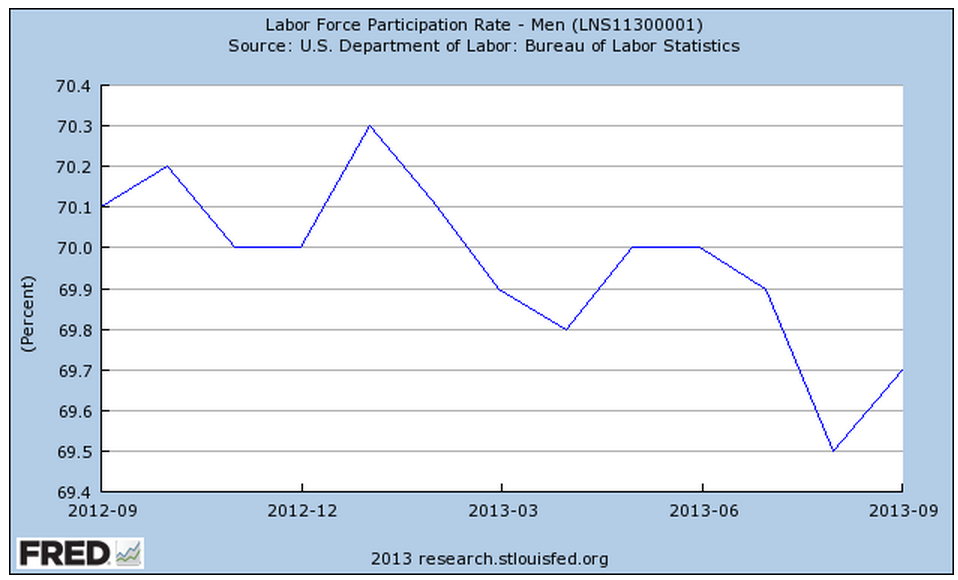

After six months of little growth, employment in construction rose by 20,000 this past month.

The rise in construction jobs helped the labor force participation rate for men, reversing a decline.

But the participation rate for the core labor force, those aged 25 – 54, shows no signs of reversing the decline of the past four years.

Demographic changes, combined with persistent job weakness among younger workers, is silently eroding the foundations of the Social Security system. The older half of the population, particularly the Woodstock generation, are growing faster than the younger population, as this table from the Census Bureau shows.

From the Census Bureau report: “the population aged 65 and over also grew at a faster rate (15.1 percent) than the population under age 45.” At the end of 2012, the Federal Government owed the Social Security trust fund $2.7 trillion (SSA Source)

The number of workers in the core labor force has declined by 5 – 6 million.

Let’s do some math. [5 million fewer workers paying into Social Security each year] x [$8000 guesstimated combined annual contribution] = $45 billion per year not collected. This is just the Social Security taxes, not including the income taxes, on a portion of the population that represents two thirds of the work force. That $45 billion represents the benefits paid to over 3 million people in 2012. (SSA Source) To put that figure in perspective, Congress is arguing over the medical device tax clause of Obamacare which is projected to raise just $29 billion over the next ten years.

It will take five to ten years for the crisis of funding to develop. In the meantime, the budget debates will grow more contentious, politicians will pontificate at their podiums with more frequency and the clouds of these dusty debates will make it more difficult for business people to plan ahead.