April 28, 2019

by Steve Stofka

When former President Obama took the oath of office, the economy was in the worst shape since the Great Depression 75 years earlier. Tax receipts plunged and benefit claims soared. Millions of homes and thousands of businesses fell into the black hole created by the Financial Crisis. In sixteen years of the Bush and Obama presidencies, the country added $16 trillion to the public federal debt, more than tripling the sum at the time Clinton left office in early 2001.

Although growth has remained slow since the financial crisis (see my blog last week), the economy has not gone into recession. Despite the fears of some, a recession in the next year does not look likely. The chart below charts the annual percent change in real GDP (green) against a ratio called the M1 money multiplier, the red line (Note #1). Notice that when the change in GDP dips below the money multiplier for two quarters we have been in recession.

The money multiplier seems to act like a growth boundary. While some economy watchers have warned of an impending recession, GDP growth has been above 2.5% for more than a year and is rising. In 2018, real disposable personal income grew nearly 3%. This is not the weak economic growth of 2011 or the winter of 2015/16 when concerns of recession were well founded.

The number of people voluntarily quitting their job is near the 1999 and 2006 highs. Employees are either transferring to other jobs or they feel confident that they can quickly get another job. An even more important sign is that this metric has shown no decline since the low point in August 2009.

In 2013, the Social Security disability fund was in crisis and predicted to run out of money within a decade. As the economy has improved, disability claims have plunged to all-time lows and the Social Security administration recently extended the life of the fund until 2052 (Note #2).

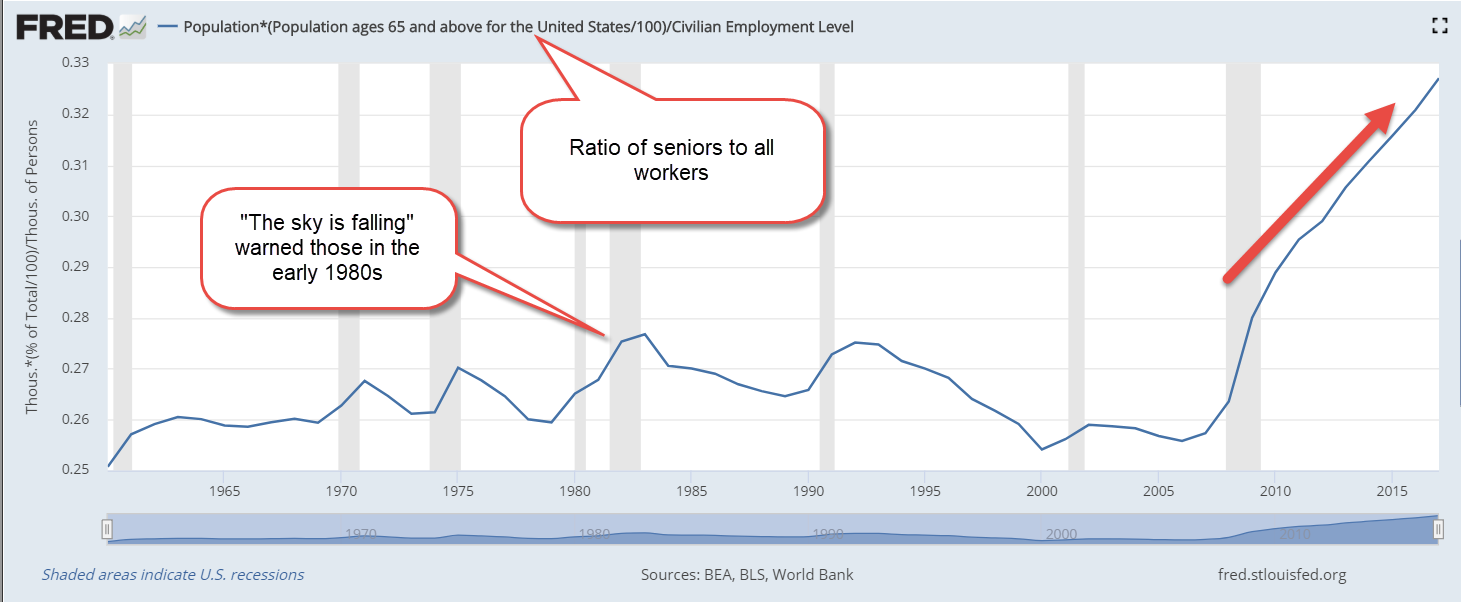

Approximately 1 in 6 (62 million) Americans receive Social Security benefits and that number is expected to grow to 78 million in a decade. However, the ratio of workers to the entire population is near all time highs. The number of Millennials (1982-1996) has surpassed the number of Boomers. This year the population of iGen, those born after 1996, will surpass the Millennial generation (Note #3). Just as a lot of seniors are leaving the work force, a lot of younger workers are entering. The ratio of worker to non-worker may reach 1 to 1. 45 years ago, one worker supported two non-workers.

As the presidential cycle gets into gear, we will hear claims that there are not enough workers to pay promised benefits. Those claims are based on the Civilian Employment Participation Rate, which is the ratio of workers to adults. While the number of seniors is growing, the number of children has been declining. To grasp the total public burden on each worker, we want to look at the ratio of workers to the total population. As I noted before, that is at an all time high and that is a positive.

Raising a child is expensive. The average cost of public education per child is almost $12K (Note #4). Public costs for housing, food and medical care can push average per child public cost to over $20K annually.

Let’s compare to public costs for seniors. The average person on Social Security receives $15,600 in benefits (Note #5). In 2018, the Medicare program cost an average of $10,000 per retiree (Note #6). The public cost for seniors is not a great deal more than those for children.

As a society, we can do this.

/////////////////

Notes:

- The M1 money multiplier is the ratio of cash and checking accounts to the amount of reserves held at the Federal Reserve.

- SSDI solvency now extended to 2052. Here’s a highlight presentation of the trustee’s report.

- Generation Z will surpass the numbers of Millennials in 2019. Report

- Public education costs per pupil

- Social Security costs

- Medicare program cost $583 billion. There are approximately 60 million on the program. CMS