A few tidbits of info sitting around on my desk:

WSJ tidbit 12/31/09 – Families USA reports that Cobra family coverage averages 83% of the average unemployment insurance check, up from 61% in 2001. The stimulus bill provides a subsidy to unemployed individuals averaging $325 a month, $715 for families.

According to a Congressional Research report – after dropping dramatically from 1950 to 1980, death from diabetes has increased to above the levels of 1950, a 33% increase from mortality rates in 1980. Unintentional injuries, including automobile accidents, has dropped by half from 1950. Cancer rates are about the same as 1950. Death from heart disease are at 40% of 1950 levels. (pg 4)

Many of us do not like government interference and mandates, yet we see the results of several decades of seat belt and product safety laws.

Despite all the money invested in cancer research over the past fifty years, the rates have not improved. Of course, more people are living longer, naturally driving up the cancer incidence rate, which disproportionately afflicts older people.

Despite the dislike that some people have for “Big Pharma”, it is thanks to the pharmaceutical industry that heart disease has become a manageable problem for many older Americans.

While many like to blame the soft drink and fast food industry for the increase in diabetes, no one is forcing anyone to drink and eat sugar laden foods. Of course, it is easier to blame the big food companies than take personal responsibility for one’s food choices.

On Oct. 16, 2009, the Bureau of Labor Statistics reported that the median (not average) weekly earnings of the nation’s 100.1 million full-time wage and salary workers was $738 in the third quarter of 2009. This was 2.5 percent higher than a year earlier. The Consumer Price Index for All Urban Consumers (CPI-U) fell by 1.6 percent over the same period.

Social Security income accounts for about 40% of retirement income.

A retired person spends, on average, about 80% of what they spent before retirement.

WSJ tidbit 12/28/09 – The Institute for Justice cites that 50 years ago, 3% of American workers were regulated or licensed by government agencies. It is 35% today.

Food, energy, housing and health care consume the same share of American spending today (55%) that they did in 1960 (53%).

Revolving credit, primarily credit cards, declined at a steep 18.5% annual rate last year.

Smaller businesses are a dying breed in the U.S. Companies with less than 250 workers comprise 70% of the private-sector work force in the European Union, compared with 49% in the U.S., according to EU figures.

In 2009, 804 companies cut dividends, up sharply from 110 two years earlier and the highest level since S&P started to collect such data in 1955. Conversely, the number of dividend increases dropped 36.4% to a record low.

More than 6% of commercial-mortgage borrowers in the U.S. have fallen behind in their payments, a sign of potential troubles ahead as nearly $40 billion of commercial-mortgage-backed bonds come due this year. Moody’s reported a 4.9% actual delinquency rate. It is projected to go above 8% by the end of 2010.

The Mortgage Bankers Association reported that almost 6.2% of mortgages in Arizona and 9.4% of mortgages in Nevada were in foreclosure by the end of the third quarter of 2009. In California, 5.8% of mortgages are in foreclosure and personal bankruptcy filings rose almost 60% last year.

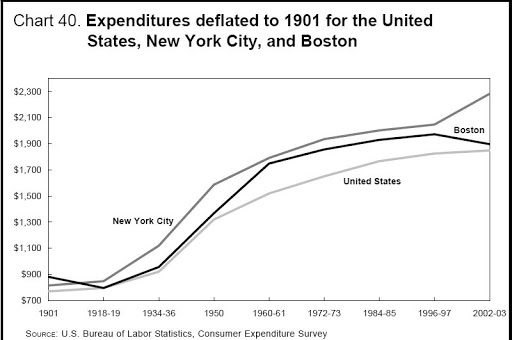

we can see the century long rise of consumer spending in real 1901 dollars despite the fact that food, clothing and housing expenses take up far less of our income today. What are we spending our money on? Chart 43 on (PDF) page 67 shows the share of income that the average household spends on non-necessities, from a low of less than 25% in 1900 to 50% today.

we can see the century long rise of consumer spending in real 1901 dollars despite the fact that food, clothing and housing expenses take up far less of our income today. What are we spending our money on? Chart 43 on (PDF) page 67 shows the share of income that the average household spends on non-necessities, from a low of less than 25% in 1900 to 50% today.

{kind=link}