This past friday, the Bureau of Labor Statistics (BLS) released their monthly assessment of labor conditions in this country and the headline figure was a disappointment. The survey of businesses showed a seasonally adjusted 115,000 net jobs added in April, below the 150,000 expected by economists. The unemployment rate dropped to 8.1% as almost 350,000 people simply dropped out. Some of this was due no doubt to early retirees but the Federal Reserve estimates that retirees account for about 25% of the drop out rate.

As I have done in the past, I’ll take a deeper look at some numbers behind the headline numbers. The core work force of people aged 25 – 54 continues to show gains but the chart below shows the comparative weakness of this segment of the work force. This age demographic is the “middle”, when people accumulate both earning and buying power and form the primary demand of a consumer economy like the U.S.

The year over year job gains continue to climb upwards.

Late last summer, the larger work force of those aged 25 and older began showing year over year job gains several months before the core work force, revealing an underlying structural weakness of both the workforce and the recovery.

Some of the workforce is graying, moving from the core 25 – 54 age demographic into the older 55+ demographic, where workers are trying to save for retirement or taking jobs because their social security and retirement income is not adequate. With a natural propensity for saving, older workers do not create the needed demand for the economy to grow strongly. In the chart below is the year over year job gains for those aged 55+ and this is a key metric for it shows which age group have enjoyed the bulk of job gains in this recovery.

Throughout this recession and the massive loss of jobs, older workers have continued to show gains. Strengths in the labor force statistics have been in retail, business services and health care. Experienced older workers can be attractive to employers offering business services. In retail and health care, it may be that older workers have less family responsibility, show a greater reliability and are thus more attractive to employers who enjoy a “buyers” market. This past month was the first month that gains slowed while the gains of the core work force continued to climb.

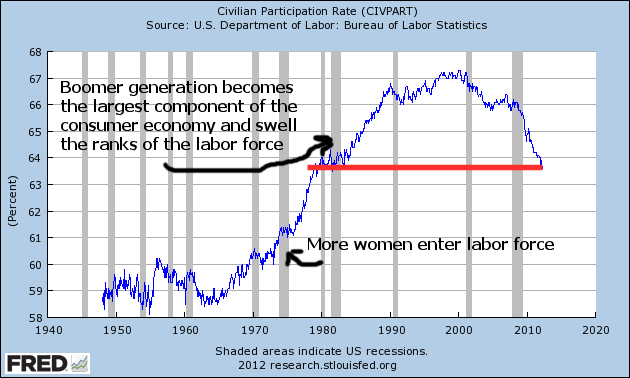

As I have noted before, the demographic bell curve of the past three decades is coming to a close. The participation rate, the number of workers as a percent of the working age population, has declined to 1981 levels, nearing the closing of an upswell brought on as the post WW2 boomer generation entered their prime working years.

The 1980 Census shows that, there were 25.5 million people 65 and older in 1980 (11.3% of the total population), an increase of 5 million from the 20.0 million count (12.3% of total) in 1970. While the numbers climbed, the percentage stayed stable in that 10 year period. Those aged 50 – 64 numbered 33.4 million, or 14.7% of the population. In 1970, it was 29.7 million or 14.6%. Again, the numbers were stable. The median age of the U.S. population was 30.

Fast forward to the 2010 census and the percentage of those aged 65+ is still relatively stable at 40.3 million or 13.0% of the population. Despite all the medical advances of the past 30 years and the trillions of Medicare dollars spent on the elderly, the percentage of older people is still about the same as it was in 1970 and 1980.

But the juggernaut of Boomers is waiting in the wings. The 2010 Census shows that those aged 50 – 64, the “meat” of the Boomer generation, numbered 58.8 million, or 19% of the total population. In thirty years, they have increased from 15% to 19% of the population. The median age of the population is now 37 years, an increase of seven years.

The 25 – 54 age group funds the social contract that provides health insurance and retirement income for older Americans. For this core work force, the increasing job gains of the past four months have been a welcome sign but, as the chart above shows, this core has suffered huge job losses in the past 3+ years and are climbing out of a deep hole. I hope that April is the beginning of new trend, where the job gains increasingly go to the core younger segment of the work force and not to older Americans. Only then will we see sustainable economic growth.