In this week’s downturn, prices of the SP500 almost touched the 26 week, or half year, average of $203.90. Since August 2012, when the 50 day average crossed above the 200 day average, these price dips have been good buying opportunities as the market has resumed its upwards climb after each downturn.

***********************

Manufacturing and Durable Goods

Preliminary readings of March’s Purchasing Managers’ Index (PMI) showed an uptick back into strong growth. Survey respondents were concerned about weak export sales as the dollar’s strength makes American products more expensive overseas. The full report will be released this coming Wednesday.

This past Wednesday’s report that Durable Goods had dropped 1.4% in February caused an already negative market to fall another 1.5% for the day and this marked the close of the week’s activity as well. New orders for non-transportation durable goods have steadily declined since the fall. Although the year-over-year comparisons are consistent with GDP growth, about 2.3%, the downward trend is concerning.

***********************

Housing

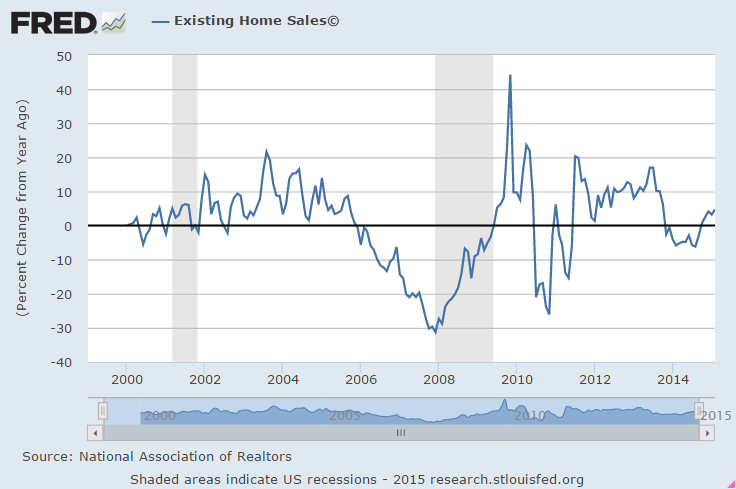

Existing home sales in February rose almost 5% in a year over year comparison, the best in a year and a half but still below the 5 million annual mark. The positive y-o-y gains during the past six months has prompted some optimism that sales may climb back above the 5 million mark in the spring and summer season.

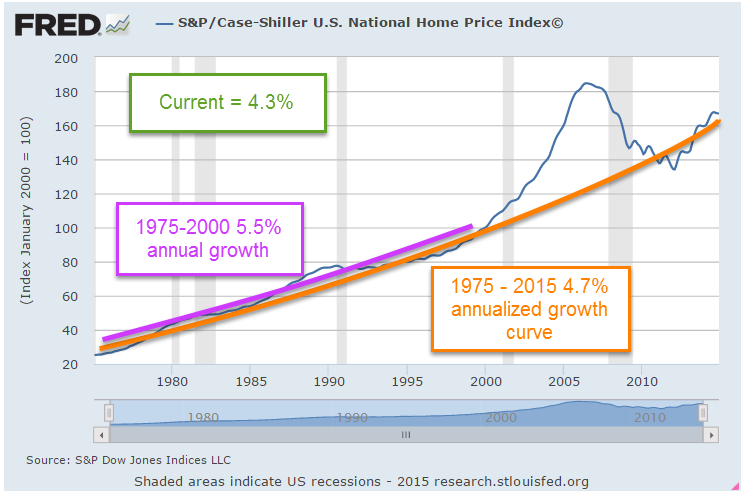

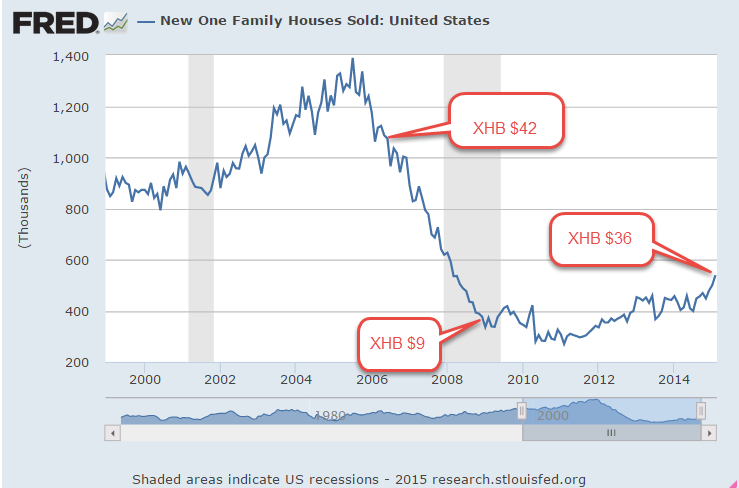

New home sales in February surged back above a half million. In a more healthy market, sales of new homes are 6% – 7% of existing homes. In 2006, that ratio started climbing above the normal range, getting increasingly sicker until it reached almost 18% in May 2010. February’s ratio was 9%. If the ratio were in the normal range, existing home sales would be over 8 million, far above the current 4.9 million units actually sold.

In a 2014 report the National Assn of Realtors noted that boomers tend to buy new or newer homes to avoid maintenance headaches while younger buyers buy older homes because they are less expensive (page 3). 38% of all home buyers are first timers but the percentage is double for those younger than 33 (Exhibit 1-9 in the report). As the supply of existing homes is inadequate to meet the demand, prices climb and suppress the demand, forcing first timers to either buy a smaller new home or continue renting.

Sales of new homes and the fortunes of home builders are based on the churn of existing homes. Since October, the stocks of home builders (XHB) have climbed 20% in anticipation of growing sales, but weak existing home sales may prove to be a choke point for growth.

The larger publicly traded homebuilders also build multi-family units. Real investment in this sector has tripled from the lows of early 2010 but are still below pre-crisis levels.

The housing market in this country is still wounded. 63% of the population are white Europeans (Census Bureau) but are 86% of home buyers (Exhibit 1-6). While few will admit to racial prejudice in the current housing market, the numbers are the footprints of this nation’s long history of racial discrimination and socio-economic disparity. Mortgage companies that made – let’s call them imprudent – credit decisions that helped precipitate the housing crisis are especially cautious, making it more difficult for younger buyers to purchase their first home, despite the historically low mortgage rates. This market will not heal until mortgage companies relax their lending criteria just a bit and that won’t happen while rates are so low.

**************************

Income

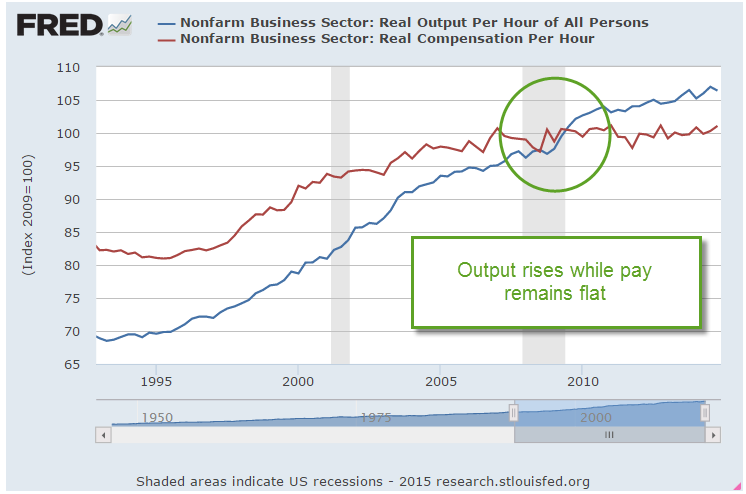

The Bee Gees might have sung “Words are all I have to take your heart away” because they were singing about love, not economics and finance. Graphs often tell the story much better than words. A milestone was passed a few years back. For the first time since World War 2, the growth in income crossed below the growth in output.

This past week, the Bureau of Labor Statistics released a revision to their initial estimate of multi-factorial productivity in 2013. There is a lot of data to gather for this series. An often quoted productivity growth rate calculates the GDP of the nation divided by an estimate of the number of hours worked, a statistic that is accessible through payroll reports submitted monthly and quarterly. The contribution of capital to GDP is much more difficult to assess and is largely disregarded by those like Robert Reich, former Secretary of Labor under President Clinton, who have a political axe to grind. Truth is on a path too meandering for politics.

Total output in the years 2007 – 2013 was just plain bad, growing at an annual rate of only 1%, a third of the 2.9% growth rate from the longer period 1987 – 2013. In the BLS assessment, the growth rates of both labor and capital inputs were poor by historical norms but capital input accounted for all of the meager gains in non-farm business productivity. People’s work is simply not contributing as much to growth as before. That reality means that income growth will be meager, which will prompt louder political rhetoric to make some kind of change, any kind of change, because voters like to believe that politicians have magic wands.