December 2, 2018

by Steve Stofka

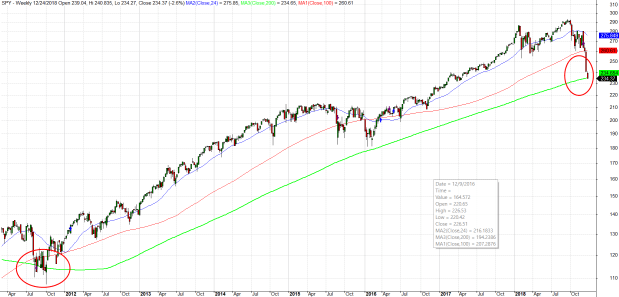

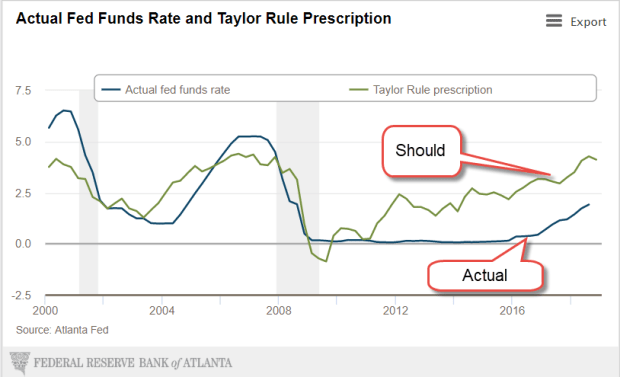

Each time the Federal Reserve raises interest rates, the President tweets out his disapproval. This week Fed Chair Jerome Powell indicated that interest rates increases might be slowing and the Dow Jones average jumped up more than 2% in a few hours (Note #1). Presidents don’t like rising interest rates because they contribute to a slump in housing and car sales, two relatively small pieces of the economy that create ripples throughout a community’s economy. Trump’s strategy relies on strong growth.

The passage of the tax law last December reduced Federal tax revenues, which contributed to a rising deficit. The gamble was that the repatriation of corporate profits plus a reduced corporate tax rate would spur higher GDP growth which would offset the falling revenues. It hasn’t so far.

Let’s get away from dollars and use percentages. Economists track the annual budget deficit as a percent of GDP. I’ll call it DGDP. Let’s say a family made $50,000 last year and had to borrow $1000 because they spent more than they made, their DGDP would be $-1,000/$50,000 or -2%. In a growing economy, the DGDP rises, or gets less negative. It falls, or gets more negative, as the economy nears a recession.

A DGDP below the 60-year average of -2.5% indicates an unhealthy economy and, by this measure, the economy has not been healthy since 2007. The DGDP was the same in the last year of Bush’s presidency as it was in the last year of the Obama presidency. By 2014, it had risen above -3% and rose slightly again in 2015 but fell again the following year.

In 2016, the last year of the Obama presidency, the DGDP was -3.13%. In the first year of the Trump presidency it fell slightly to -3.4%. As I said earlier, the administration and Congressional Republicans hoped the tax law passed at the end of 2017 would spur enough GDP growth to offset declining corporate revenues. So far, that has not happened. The 2018 budget year just ended in September. Preliminary figures indicate that the deficit will be 3.9% of GDP this year (Note #2). Some economists project a DGDP near -5% in 2019.

Japan’s economy for the past two decades strongly suggests that an aging population weakens GDP growth. The U.S. economy must flourish against that demographic headwind. By December this year, Social Security (SS) benefits will surpass the $1 trillion mark, equal to or surpassing SS taxes collected (Note #3). For years, the excess in SS tax collections has lessened the amount that the Federal government had to borrow from the public. Each year, the government has left an I.O.U. in the SS trust fund. The total of those IOUs is almost $3 trillion.

Now the Federal government faces two challenges: interest on the ever-growing Federal debt and the government’s need to borrow more from the public to “pay back” those IOUs. The interest on the debt will soon overtake defense spending. Politicians could reduce cost of living increases in SS benefits by indexing benefits to the chained price index, a flexible measure of inflation that assumes that human beings alter their consumption in response to changing prices. Benefits are currently indexed to the Consumer Price Index (CPI) whose fixed basket of goods never changes. The CPI overstates inflation, but seniors are sure to lobby against any changes that would reduce cost of living increases. Politicians are reluctant to face angry seniors who might boot some of them out of office at the next election.

Trump has a better alternative than strategically lowering benefit increases for the swelling ranks of retiring Boomers – increase SS tax collections. The only way to do that is jobs, jobs, jobs. Jobs that are “on the books,” that take out SS taxes with each paycheck; not the jobs of the underground economy that flourish in immigrant communities. More jobs to draw in the half million discouraged workers who are sitting on the sidelines of the job market (Note #4).

Jobs, jobs and more jobs take care of a lot of budget problems. Campaign strategist James Carville stressed that point to Bill Clinton during the 1992 Presidential campaign. Higher interest rates hurt the construction, auto and retail industries, and blue collar small business service industries. All of these are more likely to reach out and hire marginal workers.

The headwinds are more than demographic. The economy has been stuck in low for a decade. In the eleven years since the 3rd quarter of 2007, just before the 2007-2009 recession, real GDP has averaged only 1.6% annual growth (Note #5). That is barely above population growth. Sectors that were strong, housing and auto sales, have slowed. Housing sales have declined for six months. Auto sales have declined for 18 months. Fed interest rate policy has been very supportive but that is slowly being withdrawn.

The DGDP is one more indicator that we should already be in a recession or approaching one. A recession will add to the demographic headwinds, increase the annual budget deficit and swell the accumulated federal debt. Job growth must counter job loss due to automation. Good policies are those likely to add jobs. Bad policies are those that thwart job growth. It doesn’t matter how well intentioned the policies are. Good or bad for job growth is all that matters in the next decade.

Here’s why. Another credit crisis is building. Low interest rates transferred billions of dollars in interest from the savings accounts of older people to businesses and government, who were able to go on a borrowing binge. Defaults and delinquency on business loans will probably be the source of our next crisis. After that is the coming pension crisis in several cities and states. Let’s hope those two don’t hit simultaneously.

////////////////////

Notes:

- Within a day, interest rate futures that had priced in a 1/2% increase in the Fed Funds Rate during 2019 fell to just .3% for next year.

- Estimates of 2018 Fed deficit and GDP

- Social Security trustees’ summary report for fiscal year 2017.

- BLS series LNU05026645 discouraged workers. After ten long years, there are now as many discouraged workers as October 2008, just as the financial crisis sent the economy into shock. Within two years after the onset of the crisis, the number of discouraged workers had exploded 250%, reaching 1.25 million in October 2010.

- Real GDP: 3rd quarter 2007 – $15,667B. 3rd quarter 2018 – $18,672B. Constant 2012 dollars.