October 28, 2018

by Steve Stofka

In ten years, the number of households that own their homes has grown by only 2-1/2%. Renting households have grown by 20%.

Should you buy a home? Home prices are sky high in some cities. Mortgage rates are rising. Is 2018 a repeat of 2006? Many bought homes at high prices only to see the price fall by a third or half over the following years.

Time to discover your inner owner investor who is going to buy the house. You are going to rent the home from your owner investor. Let’s compare the annual Net Operating Income (NOI) to the purchase price of the home. To keep the math simple, let’s say the owner investor can charge the renter $2000 a month in rent for the home. Let’s say that you, the renter, are going to bear the monthly cost of utilities. You, the investor, must pay $2000 in property taxes and other city charges like garbage collection. Your annual net income from the property is $2000 x 12 = $24,000 – $2000 taxes and costs = $22,000. Let’s say that the all-in cost of the home is $360,000. $22,000/$360,000 = 6.1%. That is the cap rate of the property.

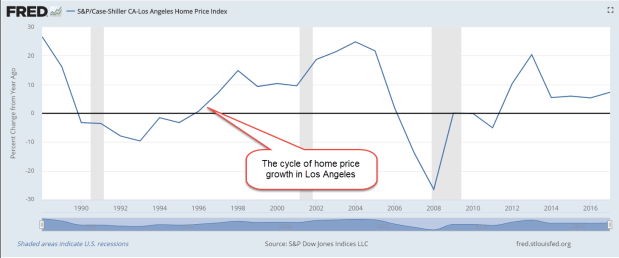

Home pricing, like many assets, behaves in a cyclic manner, as the graph below shows. In the past thirty years, the average annual growth of the Case-Shiller home price index in Los Angeles is 5.6%. The rate of the past three years is slightly above that thirty-year average, meaning that prices in the L.A. area have stabilized relative to the long-term growth average.

Rents have risen almost 5% so the two growth rates are fairly close. Let’s subtract an inflation rate of 2.6% from that to get a real capital gains rate of 3%. Add the two rates together to get a combined rate of 9.1%. For an average home in the L.A. area, this is a pretty good total rate of return.

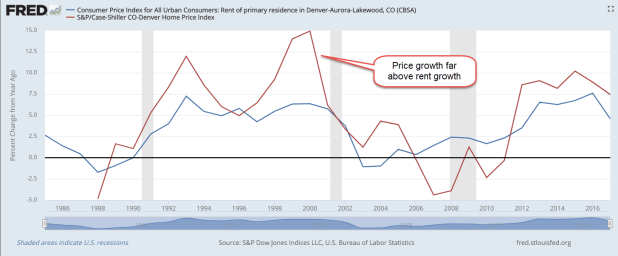

Let’s look at another area: Denver. The thirty-year average of annual growth in home prices is 4.9%. During the past five years, population growth in the Denver area has been robust. Home prices have risen more than 7.5% during each of the past five years, topping 10% in 2015. In 2017, rents rose an average of 5.33%, not enough to keep pace with the growth in prices. An investor would be buying at an above average price.

In a hot market like Denver, a family might think “I am saving 8% a year by buying now.” They assume that above average price growth will continue. The law of averages indicates the opposite – that price growth is more likely to fall below average, and even turn negative.

In making a decision, understand where current prices are in the cycle (Note #1). Understand where current rental growth is in the cycle and compare the two (Note #2). Here is a graph comparing the two series in Denver. Note the large divergence between home prices and rents in the late 1980s, 1990s and again in the 2000s. Rental prices were much more stable.

Imagine that the home purchase is a cash investment and estimate a total return on that investment, as I showed above. Some familes pick a home in a price range based on the leverage of their income and down payment. A real estate agent may present home buying choices based on the amount of house a family can qualify for. But – is the house a good deal? These rates of return are an important factor to consider in making a wise decision.

////////////////////////////////

Notes:

- You can search for “FRED home prices [large city name here]” to get the Case-Shiller Home Price Index for that city. Click Edit Graph button in upper right and change the units to “Percent Change From Year Ago”. To get an average, click the Download button above the Edit Graph button to download an Excel spreadsheet.

- You can search for “FRED cpi rent residence [large city name here]” to get the index of rental prices for that city. As above, click Edit Graph button and change units to “Percent Change From Year Ago

/////////////////////////////////

Stocks

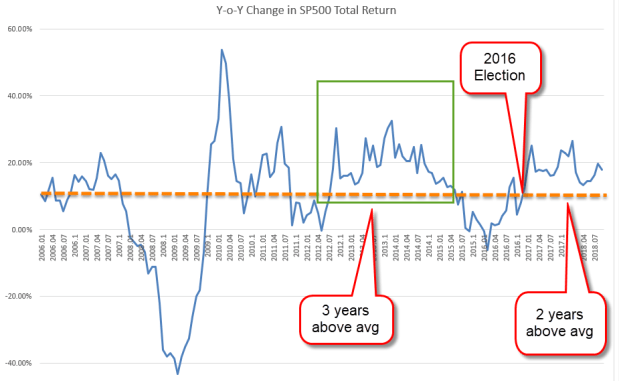

The recent downturn in the market was overdue. Since the election almost two years ago, the year over year total return of the SP500 has been above the 10% historical average.

The longest above average streak under Obama’s Presidency was almost three years. In the dot-com boom under Clinton, the market had above average returns for almost 3-1/2 years. After a two-month stumble in 1998 due to the Asian Financial Crisis, the streak continued for another twenty months. Such a long period of exuberance was sure to fall hard. During the following three years, the market lost half its value. Reagan and Eisenhower enjoyed the next longest streaks of almost 2-1/2 years. The 1987 crash ended the streak under Reagan.