July 29, 2018

by Steve Stofka

“Banking was conceived in inequity and born in sin” – Josiah Stamp

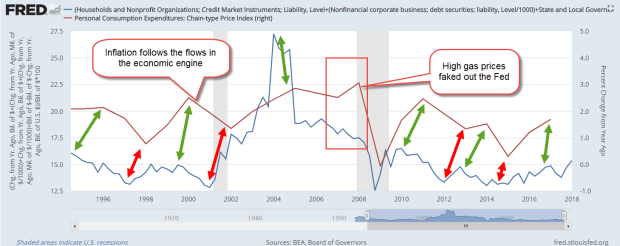

In the past two weeks, I’ve looked at the inputs and drains to the economic engine. This week I’ll look at the flow between bank credit, the largest input, and loan payments, the largest drain. Because bankers want to make a profit on the money they pump into the economy, they do a better job of managing the economy than government officials. Banks manage access to the credit system better than governments and achieve less economic inequality. Whenever governments wrest control of credit creation away from the banks to promote greater equality, the country’s economy suffers.

Let’s begin with the first point; banks must protect their loan portfolios. To do that, they monitor the health of the economy. The Conference Board uses ten data series to construct its index of leading economic indicators to estimate the probability of recession. ECRI uses 50 data series to chart its weekly leading index. These indicators are sensitive and may give a false signal, indicating a coming recession which doesn’t occur. Watching these data series are the banks who form an emergent Artificial Intelligence machine that varies the amount of credit they input into the economic engine.

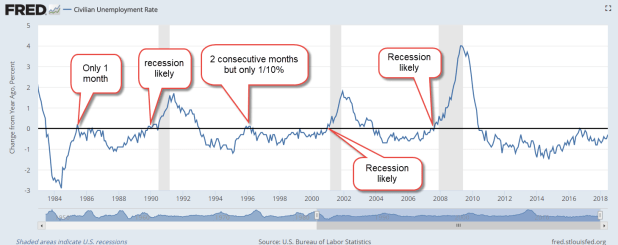

Let’s piggy back on the efforts and watchfulness of the banks. We can look for a change in the ratio of household credit, an input to the engine, to the unemployment rate, or the ability to drain the input. One quarter’s decline of 2% or greater in this ratio, or two quarters of a smaller decline has been a reliable indicator that a recession is approaching. Below is a graph of the Household Debt-Unemployment ratio during the past thirty years but this signal has been reliable since World War 2.

Bank behavior has accurately predicted the start of every recession since WW2. Is this the holy grail for mid to long-term trading decisions? Not quite. The Federal Reserve does not release the total amount of household debt for each quarter until the end of the following quarter (see #1 at end). However, every month, the BLS releases the unemployment rate, the divisor in the Debt-Unemployment ratio. If the rate is lower than a year ago, no worries. If the year-over-year change in the rate is higher in two consecutive months, worry.

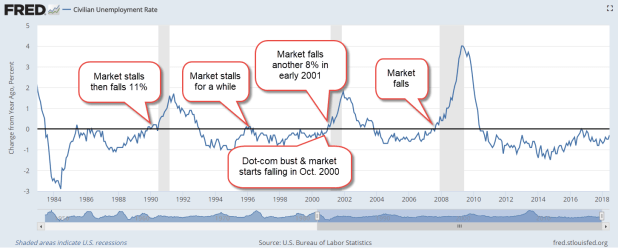

Here’s the same chart with the stock market’s reaction when the year-over-year change has been above zero for two months in a row. Insiders and market movers have lightened their exposure to equities.

Loans add money to the engine. Loan payments drain money from the engine. As unemployment rises, people reduce their loan payments. In managing their risk, the banks react to signs of economic weakness by reducing the amount of credit they issue. Because they are more responsive to evolving conditions than central banks and elected officials, banks manage the economy better than the government.

Access to credit is the key to understanding the disparity in fortunes among Americans. Let’s look at the flow of credit creation in a system where a bank can loan out ten times its deposits. Let’s say I borrow $10,000 from Bank A for a bath remodel. The contractor might have a gross profit of $2500 which he deposits in Bank B, who leverages that into a $25,000 loan to another customer, who remodels her basement. Her contractor’s gross profit of $5000 is deposited in Bank C, which leverages that into a $50,000 loan to another customer for a complete kitchen remodel. Only those people with good credit – the haves – can access this money machine. The machine is closed to the have-nots.

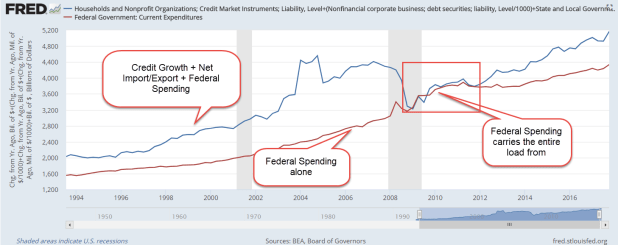

Governments have attempted to fix this inequality. The government borrows from the banks, acting as a substitute for the people who cannot borrow. The government then inputs the money into the economy, but this does not make the engine run because there is not enough being drained out in loan payments and taxes. The engine runs on flow – inputs and drains. One without the other damages the engine and makes the country vulnerable to a triggering event which causes collapse and the economic engine blows up. Yugoslavia (1994), Argentina (2000), Zimbabwe (2008) and Venezuela (2017) are the most recent examples.

Quoting an unnamed source, Winston Churchill said, “Democracy is the worst form of Government except for all those other forms that have been tried from time to time.” Private bank management of credit creation is a terrible system, but far better than the other systems that have been tried.

///////////////////

Notes:

1. With a month delay, the Fed releases a monthly estimate of household debt that excludes mortgages and HELOCs.

Ten years after the recession, the amount of household debt per employee is still above trend. A ratio of debt to disposable income is below trend.

According to the credit reporting agency Experian “Transactors” are 29% of card holders and pay off their balance each month. 43% carry a balance. The rest are dormant accounts. Experian ranks states by the average credit rating of its residents.

Fannie Mae reports that, as of the end of 2017, 37% of the mortgages modified during the housing crisis had defaulted again.

Bank of America clients with High Net Worth reported that their allocations were 55% stocks, 21% bonds, 15% cash, 10% other.

In May, consumer credit increased at a seasonally adjusted annual rate of 7-1/2 percent. Revolving credit increased at an annual rate of 11-1/2 percent, while nonrevolving credit increased at an annual rate of 6-1/4 percent (Federal Reserve)