September 24, 2017

Republicans in Congress hope that they can enact comprehensive tax reform that will lower taxes for individuals and corporations. The Congressional Budget Office estimates that, under current law and before any tax reform, the current $20 trillion deficit will grow to $30 trillion by 2026. They recommend a combination of decreased spending and increased revenue that would amount to $620 billion (in current dollars) annually, about 15% of current Federal spending of $4.2 trillion. CBO’s goal is to achieve a level of public debt to GDP that is about 40%, the 50-year average.

Lawmakers struggle to cut even 5% of spending but let’s assume that they could accomplish that and reduce spending by $210 billion. That might be the easier task. The Federal government is currently collecting 18.5% of GDP in taxes, a few tenths more than the 18.2% collected during the Reagan years. The CBO says that the dollars collected is not adequate to meet the Federal government’s current level of spending and obligations and they project that annual deficits will increase over the next decade. The 70-year average of federal revenues is 17.5% of GDP.

Raising an additional $410 billion, or 10% extra in revenue, will require raising taxes or increasing GDP. Republican lawmakers and some economists hold fast to a theory that reducing tax rates will increase economic growth. To raise an additional $410 billion for a total of $4 trillion dollars, and collect the 50-year average of 17.9% of GDP in tax revenue, GDP next year would need to be almost $23 trillion, a whopping 20% increase from the 2016 level of $19 trillion. No amount of tax decrease will spur that much growth. A Republican Congress will not pass a tax increase.

In a recent Senate budget committee hearing, I was surprised to learn that half of the cost of corporate taxes is borne by the workers, as estimated by the Tax Foundation. The OECD finds that corporate income taxes are most injurious to people’s incomes and is why most developed countries have lower corporate tax rates than the U.S. These countries augment their revenues with a consumption tax, most often a VAT, or value added tax. Another surprise: consumption taxes are less of a burden to a worker than higher corporate taxes.

The founding of this country was instigated by a protest over a tea tax. In the Framer’s Coup, Michael Klarman relates the bitter debates over slavery and taxes at the 1787 Constitutional Convention. 230 years later, the debate over slavery may have ended but the debates over taxes are just as ferocious.

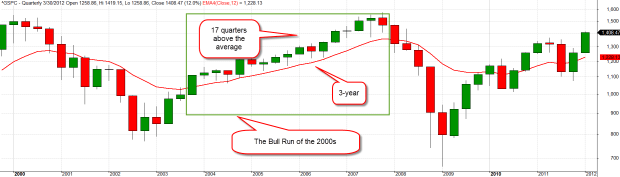

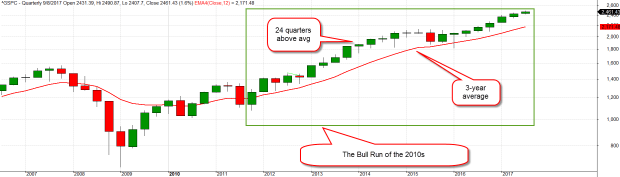

Since last November, the stock market has priced in the probable passage of tax reform by the end of this year or early next year. Republican lawmakers have been unable to repeal Obamacare and I think they will have an equal amount of difficulty passing tax reform.

CBO budget projections restrain the freedom of lawmakers to enact their favorite theories. Lawmakers are highly motivated to answer the whoops and hollers of their voters, many of whom may not be interested in the achingly dull but necessary procedures of budget craft. The parliaments of European governments can enact sweeping legislative changes that are difficult under our federalist system. The U.S. chose a different path of checks and balances embedded in a Constitution hammered out by compromise and a suspicion of human beings given legislative power. Time and time again we are reminded that those suspicions were well founded. Voters and lawmakers may become frustrated with the procedural obstacles of crafting legislation but the U.S. Constitution is the longest living Constitution because of those obstacles.

History lesson done. Stock investing lesson: don’t count your tax reform before it hatches.