On Dec. 1st, the bipartisan National Commission on Fiscal Responsibility and Reform (Debt Commission) will hold its sixth meeting to hammer out a series of proposals to reduce both the deficit and debt of this country. Deficit refers to the current year’s budget imbalance, while debt is the sum of each year’s deficit. You can watch previous meetings here.

Earlier in November the two co-chairs presented a draft proposal which distributes the pain of both budget cuts and higher taxes in an equitable fashion. Of course, any constituency who suffers from the cuts or has to pay the higher taxes will not like a particular proposal – a NIMBY syndrome that has infected this country.

Why bother planning for the future? Why not just wait till things get really bad and we have a Treasury Bond crisis, where other countries start selling their holdings of this country’s debt and the government has to pay high interest rates just to get anyone to buy the debt? Ireland and Greece have tried that method and it has gotten ugly as each of those governments has had to make severe reductions in social security pensions and other benefits. By planning ahead, we can make more gradual reductions but regardless of what we do, we will be reducing benefits and raising taxes. Elected politicians of both parties have been making promises, and “bringing home the bacon” to their constituents for several decades. They have done this by spending the social security taxes – essentially making it a flat tax for the general fund – that the large numbers of “boomers” have been paying in. The boomers are nearing retirement age.

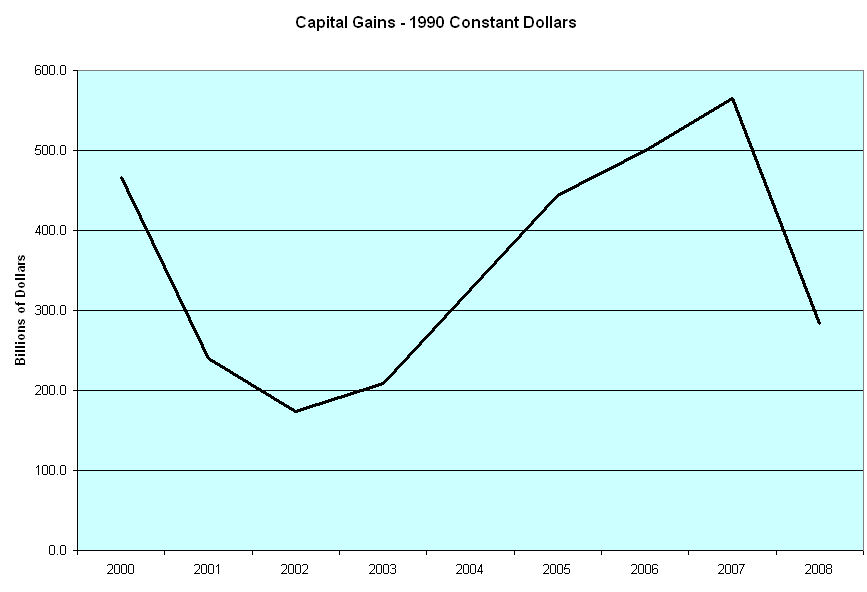

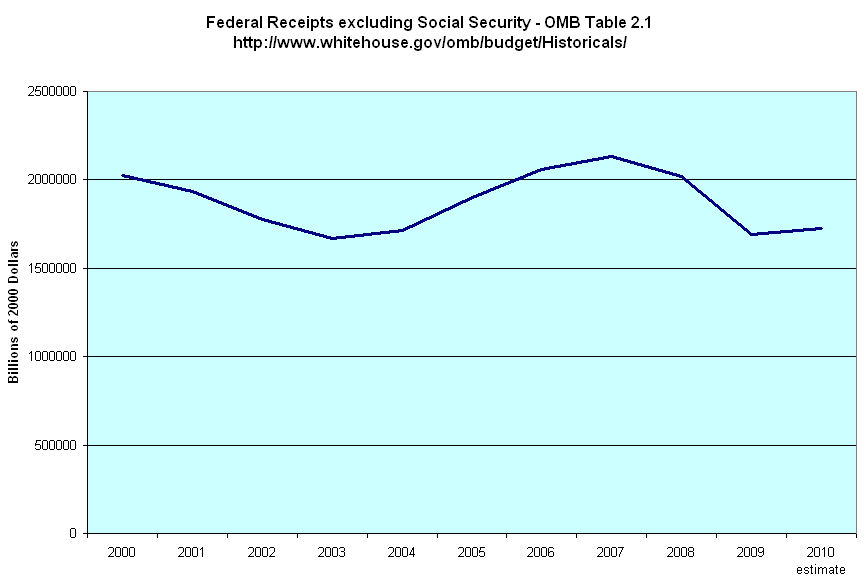

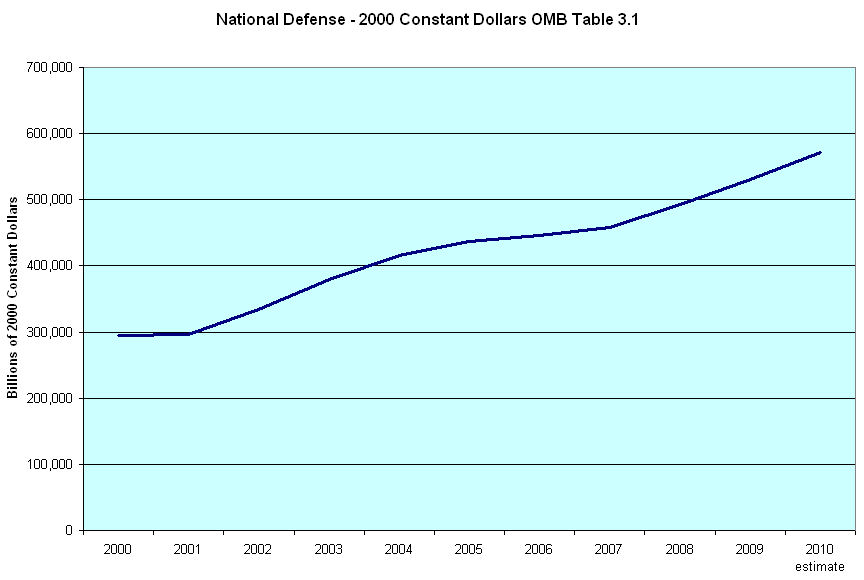

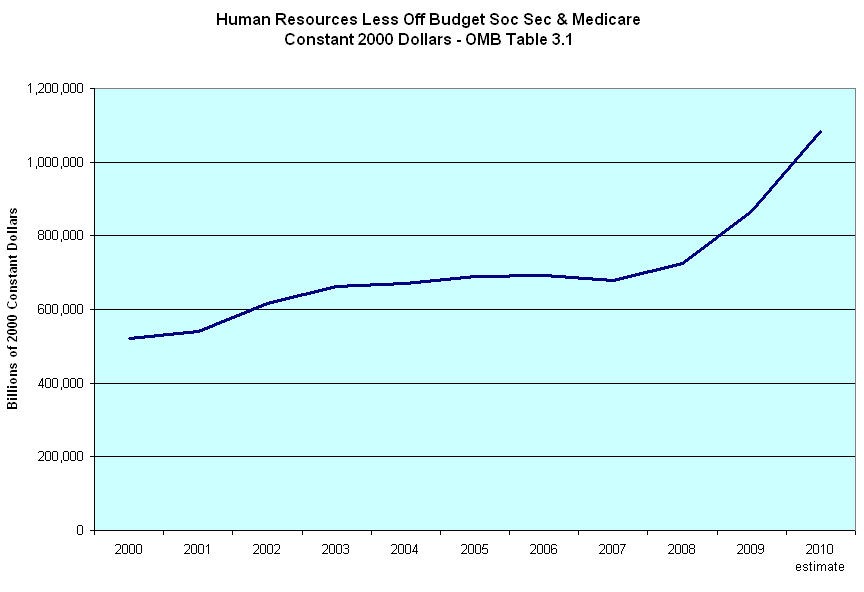

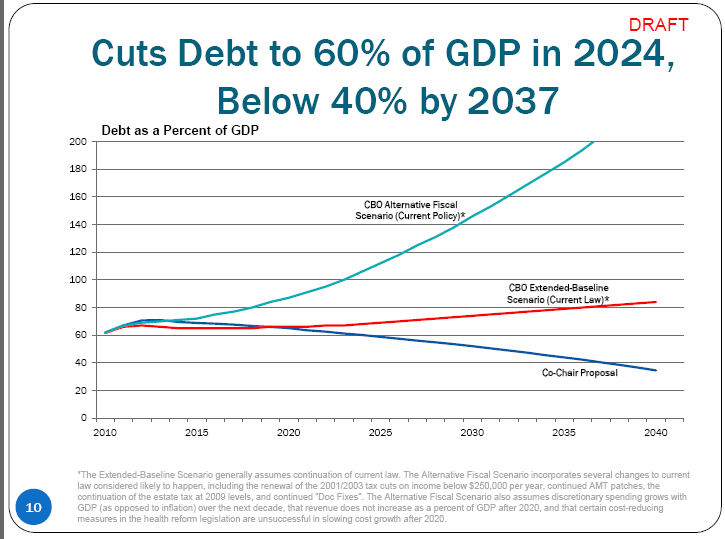

Here is the Congressional Budget Office (CBO) projection of this country’s debt and the effect of the Debt Commission’s proposals on the debt. (Click to enlarge in separate tab)

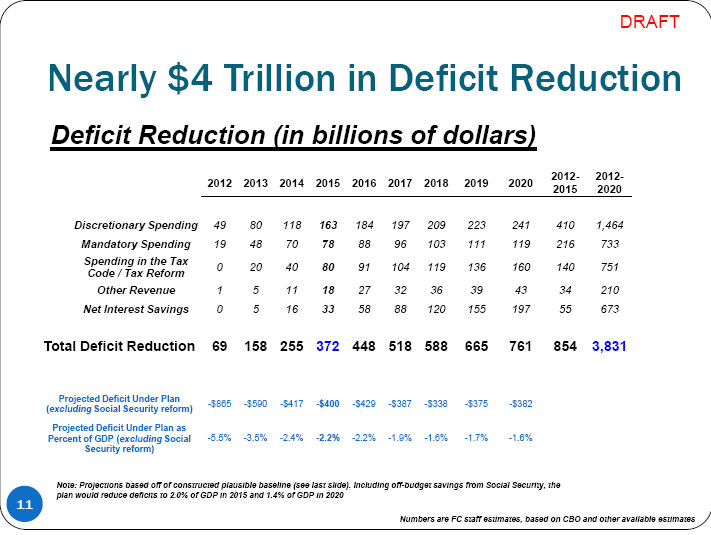

Here is a summary of the proposals, excluding any Social Security reforms.

As people are living longer, it makes sense to consider raising the full retirement age. But this recent report by the Government Accountability Office (GAO) shows that such a seemingly simple solution has consequences that I had not considered. They found that a quarter of the pre-retirement aged population had some work limiting condition and that two thirds of them work a physically demanding job. The GAO thus anticipates a rise in disability, unemployment, food stamp, Medicaid and other benefit claims as this older population is unable to find work that they can reasonably perform. The percentage of work restricted workers would only grow as we raise the retirement age. The more sensible and fair solution is to reduce benefits and eliminate the early retirement option introduced in the 1960s.

When the Social Security system was enacted in the mid thirties, life expectancy for a 60 year old worker was 72. (Bureau of Labor Statistics Monthly Labor Review, pg. 4) In 2006, the Census Bureau estimated life expectancy for a 60 year old at 82, an additional ten years of life – and retirement benefits.

It is going to take character for many politicians to take on Social Security reform but it must be done if we are to get our financial house in order. The last time the system was reformed was in 1983, when Democrats held a sizeable majority in the House and Republicans controlled the Senate. The full retirement age was raised to 67 on a sliding scale and the payroll tax was increased. Since then we have seen that increasing the payroll tax is but a flat tax, an excuse for our elected representatives to spend ever more money that they don’t have. Any increase in payroll taxes would have to be accompanied by a complete divorce of the Social Security trust fund and the general revenue fund of this country.

To hide the cost of the Vietnam war, President Johnson in the late sixties instituted the “unified budget” so the Federal government could take in payroll tax revenues, put them in the general fund, issue paper IOUs and spend the money on the war without arousing public anger. Ever since, politicians have been hiding the size of real budget deficits. Even when this country last had a “surplus” in the Clinton years, it was only a surplus because of the huge Social Security surplus. The real budget ran a deficit.

Will we grow up, wake up and take some responsibility or will we continue to keep thrusting our hands into the Federal pot of money, trying to get as much as we can? For too many years we have behaved as shoppers did last Friday morning at a Wal-Mart in Honolulu, pushing and shoving to get the best deal, then trying to take deals away from other people when there were no more to be had.