Every Christmas, the President and his faithful scribe journey to Camp David near Thurmont, MD. There on the top of the mountain they wait for God to give them the 10 year economic forecast, including the projected GDP and unemployment rate for the nation. In February, or January if the President is leaving office, he presents the tablets of wisdom to Congress in the annual budget. The Congressional Budget Office then uses these projections to score various spending bills and programs, divining their future impact on the budget of the nation.

Actually, the economic forecast is painstakenly crafted each January by the President’s economic advisors, who are locked in a dungeon on the 4th sublevel under the White House, where they tear at each other limbs until the victor emerges from the dungeon gloom with his forecast, which he presents to the President.

In January 2001, just as President Clinton was leaving office, he presented what is called the “Legacy” budget to Congress. It included a robust growth of 5.4% in GDP during the early part of the 2000s, tapering to a 5.1% growth at the end of the decade. This rosy projection was far above the 3% that the nation had experienced during the past thirty years. After 9-11, President Bush’s administration revised growth projections to a more reasonable 2.2% growth for 2002, then forecast a slightly more subdued GDP growth than Clinton had envisioned but never below 5%. So how did these prognostications match up with reality? Below is a chart of projections (Source – last table on the page) and the official GDP numbers as determined by the BEA. (Click to enlarge in a separate tab)

Actual GDP numbers were a bit above Bush’s post 9-11 forecast – until 2009 and 2010. Projected 2009 GDP of $15 trillion was almost a trillion more than what we actually produced. 2010’s performance was more than a trillion below Bush’s forecast 8 years earlier. Federal revenues average about 18% of GDP so each trillion below GDP projections represents $180 billion in revenue that is not going to come into the Treasury as planned. Those plans assume unemployment at less than 6%. As it has climbed to above 9%, the shortage of revenue is even more pronounced.

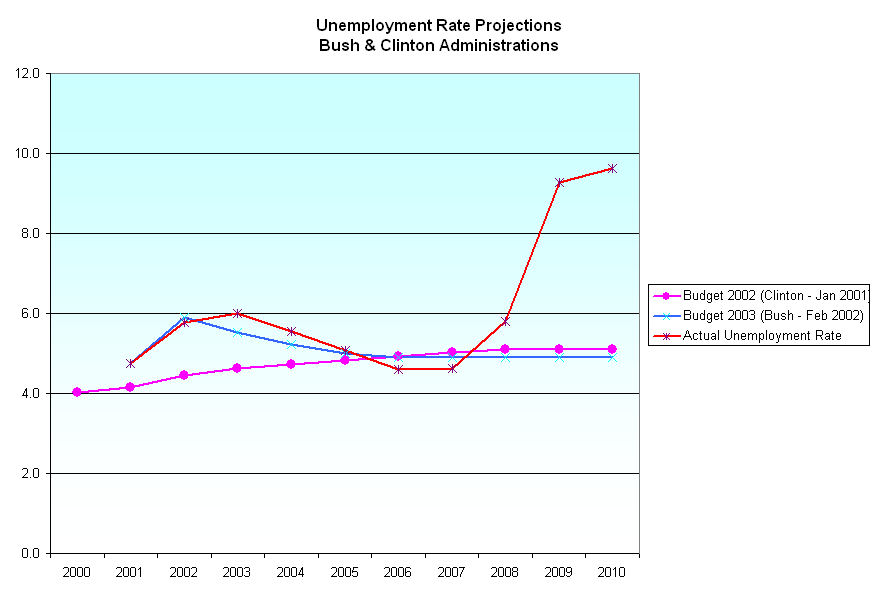

Below is a chart of projected unemployment rates for the past decade and the actual average unemployment rate for each of the past eight years. Clinton’s projections, occurring before 9-11, were rosy. Bush’s post 9-11 projects were fairly accurate. His economic team anticipated a faster rebound after the recession of 2002 but the unemployment rate actually dropped below projections during the heated years when the housing market rose dramatically.

What neither projection could envision was the severe recessionary unemployment of 2008 – 2010. What becomes obvious is that Presidential budget forecasts have not included recessions unless they were ongoing at the time of the forecast. Since recessions occur fairly regularly in an average seven year cycle, it appears that these forecasts are unrealistically optimistic. Since they help determine economic policy, spending on social and defense programs, they should include such a likelihood or we are doomed to be “surprised” at the onset of every recession. Each “surprise” results in a deficit, adding to the total debt of the nation.

Under the current budget process, there is no upside for a President’s economic team to project recessions since it means a projection of less revenues for the government, and thus, less funding for their programs. A more realistic budget process would include at least a mild recession every 7 years. If a President is elected and there has not been a recession in 3 years, then his forecast assumptions should include a recession 4 years in the future. Unrealistic optimism only hurts both the finances and the spirit of our people when recessions occur, revenues fall and programs have to be curtailed or cut.