April 27, 2025

By Stephen Stofka

This is part of a series on persistent problems. The conversations are voiced by Abel, a Wilsonian with a faith that government can ameliorate social and economic injustices to improve society’s welfare, and Cain, who believes that individual autonomy, the free market and the price system promote the greatest good.

Abel said, “After last week’s conversation on the homeless problem, I wondered about the strategies cities have devised to tackle the problem. I thought Denver and Aurora provided a good contrast. Here are two cities in the metro Denver area that have adopted policies with a different emphasis. They share a common border so imagine you’re standing on one side of a border street. Homeless people on that side of the street get treated one way. Homeless on the other side of the street get dealt with under a different policy.”

Cain smiled, “Well, you had a more productive week than I did. I spent Monday worrying about the consequences if Trump tried to fire Powell, the head of the Federal Reserve. On Tuesday, Trump said the media made too big a deal out of things he said.”

Abel asked, “What did Trump say?”

Cain replied, “That he wanted to fire Powell. Trump’s exact words were ‘his termination cannot come fast enough’ (Source).”

Abel smirked. “Naturally, it’s the media’s fault for broadcasting what Trump says. Anyway, to get back to the homeless problem. Yeah, the mayor of Denver, his name’s Mike Johnston, ran on a campaign of reducing homelessness and took office in July 2023. He immediately announced his administration’s ‘All In Mile High’ program. By the end of that year, the city had bought a hotel and turned it into a shelter for 205 families. Tamarac Shelter it’s called (Source).”

Cain whistled. “A government that got something done in six months. Good for them.”

Abel continued, “By the end of last year, the city had moved 2500 homeless people into housing of some sort (Source). The cost was about $155 million in the 17 months ending in December 2024 (Source). Much of the expense was startup costs, funded by federal grants for the purchase and repair of buildings to house homeless people (Source). The city expects to spend almost $58 million in fiscal year 2025 as ongoing costs to provide housing and support programs for 2000 homeless.”

Cain asked, “How many homeless people does Denver have?”

Abel replied, “A few years ago, they estimated 9000 (Source). That’s less than the 11,000 estimated homeless in 2012 (Source).”

Cain frowned. “So, the city hopes to resolve the problem in the next two years?”

Abel sighed. “Resolve? No. Reduce? Yeah. They estimate that people will spend six to twelve months in the program so I suppose the goal is to show a strong response in the hopes that the problem will ease.”

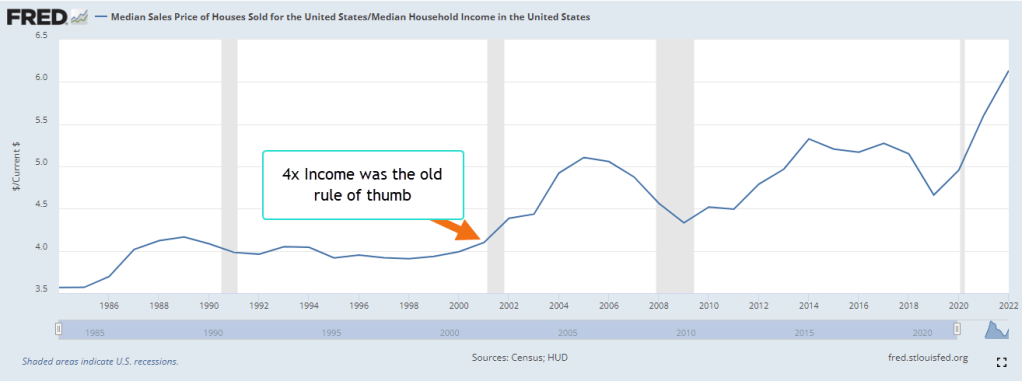

Cain raised his eyebrows. “Housing is not getting cheaper. That’s going to put some pressure on poorer families who are just one or two paychecks from homelessness. How many of the homeless are these immigrants that got bused up from Texas?”

Abel shook his head. “I don’t know but migrants were the main component of the surge in homelessness in 2022 and 2023.”

Cain nodded. “You said the city estimated a cost of $58 million a year to provide shelter and support services for 2000 homeless people. Napkin math tells me that’s about $30,000 per person. That’s the same amount the federal government spends to house someone in a standard federal prison (Source). That says something about our priorities and values. In essence, we pay people not to work, whether they commit a federal crime or become homeless.

Abel scoffed. “Well, that’s not exactly giving them money.”

Cain argued, “It’s giving someone money. One man’s expense is another man’s income. That’s the underlying problem. The prison industrial complex naturally promotes more prison time as a solution to crime.”

Abel showed surprise. “You would support more rehab services instead of prison?”

Cain shrugged. “Depends on what the crime is. I don’t think rehab works well with violent people. They have seen violence as a solution to their problems for a long time.”

Abel asked, “That’s not true. Given an opportunity and the right emotional circumstances, an abused wife might kill her husband. Maybe there was not an immediate threat when she killed him, so a jury doesn’t buy her plea of self-defense. She killed him to avoid the likely chance of mortal injury because of her past experiences with her husband.”

Cain nodded. “Maybe you’re right. There’s not a cut and dried rule. Given that each individual’s circumstances are a bit different, I wonder if AI could be used to guide sentencing? An AI could scan through a gazillion histories of court cases involving violent crime, look for patterns that promise a greater chance of success with rehab.”

Abel wiped his mouth with his napkin. “I like that. A more individualistic approach.”

Cain continued, “These damn politicians just don’t think of the long-term consequences of their spending policies. They adopt a ‘tough on crime’ political posture to get re-elected. They support privatization of prisons because private corporations don’t have to be as accountable to the public. Core Civic runs 61 prisons (Source). The GEO Group has 50 facilities in the U.S. that house prisoners and detained migrants for ICE (Source). These are big businesses that are listed on the New York Stock Exchange. GEO had a drop in profit last year because they spent money to build additional capacity for detained migrants.”

Abel’s eyes widened. “Border crossings are at historic lows (Source). GEO can’t be happy about that.”

Cain nodded. “Sure. They’ve invested money. They want to fill those detention facilities. You can bet their lobbyists are bending ears in the White House and Congress. I’m just afraid that cities like Denver are going to promote a similar constituency of companies that provide services for the homeless. Those companies do not want a reduction in homelessness. OK, so what’s Aurora’s approach? You said it was different.”

Abel nodded. “Denver emphasizes a stable home as a priority. Aurora takes a “tough-love” approach that emphasizes work. They have three tiers of assistance. At Tier 1, which is an emergency level, the homeless have shelter but no privacy. They need to work at improving their lives through rehab, volunteer and paid work to earn a spot in Tier 2 housing, which is semi-private, and Tier 3, which is private (Source).

Cain replied, “Yeah, I like that. A program with incentives. In fact, I’d like to see an incentive program for prisoners. They would get basic gruel, a crude bed and a minimum of yard time when they first got into the facility. They would have to prove themselves to get better food, board and time outside their cell.”

Abel frowned. “The prison would need to segregate prisoners by level of accomplishment. The prison kitchen would need to cook separate meals. Housing facilities would need to be segregated. I’ll bet a lot of prisons just don’t have the resources for that. Raise taxes? There would be a lot of pushback from voters for an ‘incentive’ program like that.”

Cain shook his head. “Goes to prove my point. The prison industrial complex wants high recidivism rates. Most of the guys in prison need to have goals set for them. They are there in prison because they wanted something they didn’t deserve. They need to be broken of that habit.”

Abel scoffed. “Robbery, I get your point. Murder? How is that taking something you don’t deserve?”

Cain replied, “Murder is the quintessential example of taking something you don’t deserve. Someone else’s life.”

Abel argued, “That’s an overly simplistic perspective. The abused wife example I gave earlier. What does that have to do with how they are treated in prison?”

Cain put his coffee cup down. “The prison gives them something they haven’t worked to deserve. Food and shelter. That just reinforces the behavior they developed outside of the pen. They are treated better than some prisoners of war who have to build roads or bust rocks for their keep. So, these guys go to war against their society and society rewards them for it by giving them free room and board. No wonder there is such a high rate of recidivism.”

Abel cocked his head. “I don’t see people lining up to get into prison.”

Cain nodded. “Most people don’t like to be caged up like animals in a zoo.”

Abel raised his eyebrows. “The Romans let slaves work their way to freedom (Source). Is that part of your program?”

Cain shook his head. “I think a lot of states have policies that reduce prison time for good behavior. This could be an adjunct to those programs, I suppose.”

Abel asked, “No, I mean could a prisoner work to have their conviction wiped clean? It would help people looking for a job.”

Cain looked puzzled. “That’s an interesting proposal, but maybe too much of a change? Could a child sex offender get his conviction erased? Would society want that? I don’t know.”

Abel said, “Let’s get back to the homeless. I favor getting them settled into housing first, forming a daily routine, developing a sense of safety before they try various steps to rehabilitation.”

Cain replied, “I like the work first model that Aurora has adopted. Step 13, now called Step Denver, has been using that model with addicts since the early 1980s (Source). They have been dependent on government services for many years. Step provides group housing, but the emphasis is on sobriety and getting a full-time job to break that cycle of dependence (Source). Some of these people have not had a regular job for years. They need to relearn the routines of daily life. Get a paycheck, budget money, go shopping, pay bills.”

Abel argued, “But that program was designed for men only. Women, especially those with kids, need a stable home life. If they have pre-school children, getting a job is a second priority after taking care of their kids. A decade ago, the Colorado Coalition for the Homeless estimated that women made up 45% of the homeless population (Source). You like simple rules, principles that you can apply in all circumstances. That approach doesn’t work in the real world.”

Cain shook his head. “Maybe not but it’s a starting place. In a country with 350 million people, we can’t apply the law based on individual circumstances. The Trump administration is trying a simpler approach in order to expedite immigration policy. Inevitably, the liberal media finds an instance where the application of the law seems unjust because of an individual’s circumstances. Hey, I have a heart. I feel bad for some of those individuals. But student visas and green cards come with restrictions. Sure, those restrictions have often been ignored, but they are there.”

Abel frowned. “There was a dad from Indonesia with a student visa and a pending green card application who was deported because he was convicted of a misdemeanor for spraying graffiti on a semi-truck trailer (Source). The Trump people are treating people like computer programs. They probably search a bunch of databases for immigrants and visa holders who have broken any rule, no matter how slight. A programmer can write a rule and feed that rule into a computer.”

Cain admitted, “Yeah, it’s not perfect, I’ll admit. The DOGE team used a similar methodology. They fired recent hires who have fewer job protections. It didn’t matter what those people did or how critical their jobs were. No matter what method people use to streamline government or any large organization, there are going to be mistakes and injustices.”

Abel asked, “So what are our choices? On the one hand, we can have an incompetent government that can’t get anything done because it tiptoes through a lot of hurdles put up by advocacy groups. On the other hand, we can have a government willing to make some casualties as it enacts policy and hope that we don’t become the victims.”

Cain argued, “You said I was too simplistic. I’d say your alternatives are too simplistic. Look, we invented this complex system of government about a hundred years ago. Each decade, we bolted on policies and procedures until government has become a series of Rube Goldberg machines that are way too complex for the task they must accomplish. Trump is trying to undo some of those machines. It’s not pretty.”

Abel shook his head. “His administration keeps taking things apart before they studied how they were put together. When mistakes come to light, they blame it on ‘politics’ or ‘improper classification of employees.’ Like Trump, DOGE never makes a mistake. It’s always someone else’s fault.”

Cain sighed. “We started out talking about policy solutions for the homeless and now we are discussing problems with redesigning federal government practices. What’s the point?”

Abel’s tone was exasperated. “Governments can’t conduct policy using simple rules because many of the problems that government handles are complex.”

Cain interrupted, “The private marketplace handles complex problems as well. Remember Milton Friedman’s video ‘I, Pencil’(Source)? The manufacturing of a simple pencil uses materials sourced from all over the world. The price system helps coordinate the work of thousands of people and a lot of capital to produce a simple pencil.”

Abel resumed, “That is a good example of a complex problem involving an exchange of goods and services. The buyer of the pencil has one problem to solve. Writing. Government handles problem bundles, where one problem is a container of many, call them sub-problems. What if the pencil had to be used as the rod in a Tinkertoy set as well? The pencil design would have to be more complicated. The lead tip of the pencil would be good for writing but weak for making a connection in a Tinkertoy structure.”

Cain smiled. “I like that.”

Abel continued, “Each problem in the bundle interacts and interferes with other problems in the bundle. It’s like a whack-a-mole game. Solving one problem makes another problem worse. It’s like walking with a bowl full of water. We fall forward to walk. That interferes with keeping the water level in the bowl, so it doesn’t spill. Which is more important? Getting the bowl across the room or spilling as little water as possible? Choosing a priority is a policy decision.”

Cain interrupted, “Ok, I get it. So, Aurora has chosen to get the bowl across the room, to get the homeless working in a productive job, even if that strains the homeless person’s mental or character resources. Denver’s priority is to spill as little water as possible, to keep the homeless person’s personal life stable and level. A go slow approach.”

Abel laughed. “I hadn’t made the connection but OK. It’s like I enjoy the shade tree in my front yard because it blocks the sun during the summer and keeps the house cooler. But it’s messy in the spring when it spreads its seeds and in the fall when it sheds its leaves. The tree’s solution to my need for shade creates other problems. My priority is shade. A lot of government problems are like that, only ten times more complex. That’s why we hand these problems to politicians.”

Cain sighed. “Unfortunately, people vote for politicians who say they have a magic wand that can fix these problems.”

Abel smirked. “Like Trump. He promised to bring prices down, to resolve the war in Ukraine and Gaza. People who don’t pay a lot of attention to politics voted for that illusion. Prices are up and the wars continue. The chaos grows.”

Cain nodded. “We secretly long for simple rules. They help us navigate our personal lives. Why can’t they work for society’s problems?”

Abel looked up. “Jesus thought two rules were sufficient. He was a preacher, not a politician.”

Cain placed his napkin on the table and stood. “A preacher who was put to death by politicians. That’s depressing. Hey, I’ll see you next week.”

Abel smiled. “First week of May. Flower planting time. See you next week.”

//////////////////

Image by ChatGPT in response to the prompt “draw an image of a whack-a-mole box.”