This week’s letter continues a look at taxes. This week the House passed a series of six spending bills that will avert a partial government shutdown. A majority of Republicans voted against the measure and Marjorie Taylor Greene, the bombastic representative from Georgia, filed a motion to remove Mike Johnson, the current House Speaker. It is unlikely to come to a vote because Republicans have only a one-member majority in the house after Mike Gallagher (R-WI) announced his early departure from Congress. A vote for a new speaker risks the chance that Democrat Hakeem Jeffries (D-NY), the current Minority Leader, might win the vote and become Speaker.

Most Republicans in the House and Senate have taken a “no-new-taxes” pledge called the Taxpayer Protection Pledge. The Americans for Tax Reform (ATR) database lists 191 members of the House and 42 members of the Senate who have taken the pledge. They have committed to not raising income tax rates. Additional tax revenues that arise from eliminating a tax deduction or loophole must be dedicated to lower taxes, according to the ATR’s FAQ page. Republican representatives implicitly committed themselves to increasing deficits but that is an unpopular political stance. They pledged to reduce spending but not military spending, the largest discretionary category in the budget. They pledged to reform entitlement programs like Social Security, Medicare and Medicaid, but rural Republican voters repeatedly rejected such reforms because they depend on those programs. Each time Republican members of Congress stepped away from the issue to save their political hide.

Many conservative members of Congress protest the social spending programs that crowd out other priorities. In 2010 defense spending was over 5% of GDP, more than twice the percentage of the state and federal spending on Medicaid. Defense spending has been reduced to 3.6% of GDP and Medicaid spending has grown to 3.2% of GDP. I will leave the series and chart links in the notes. As a share of GDP, Medicare has grown from 0.5% in 1967, two years after the program was enacted, to a current level of 3.6%.

The trustees are projecting a per capita growth rate of 5.4% and the program is now almost half funded by general tax revenues. Dedicated payroll taxes and cost sharing by Medicare recipients were supposed to fund the program entirely. Democrats want to raise taxes to shore up underfunded entitlement programs they instituted last century when they had filibuster proof majorities. Republicans view these higher taxes as a moral hazard, a reward for Democrats’ excessively optimistic promises and poor planning.

Voters in rural counties form a strong Republican base but depend on state spending and taxes from urban taxpayers to support the infrastructure central to their local economies. The growing of grains and vegetables, and the raising of animals requires natural resources that include land, water and food. Highways and utility lines in sparsely populated counties connect farmers and ranchers to their markets. Despite gains in efficiency, the farming and ranching industries are less efficient than industrial production. Crops and animals do not pay taxes. People do.

Elected officials must play a game with their constituents. Politicians in state legislatures could enact a head tax on dairy cows and beef cattle to cover the cost of those direct and indirect costs. Federal officials could enact a pollution tax on cattle and chickens whose concentrated effluent contaminates interstate waters. However, such taxes would raise the prices of milk and beef in grocery stores. Officials are hesitant to enact specific taxes like that because such taxes arouse voter anger and risk a politician’s career. Lawmakers prefer to fund such costs with general tax revenues. The costs appear as line items on a state or federal budget that is hundreds or thousands of pages long and disappear in the thicket of words.

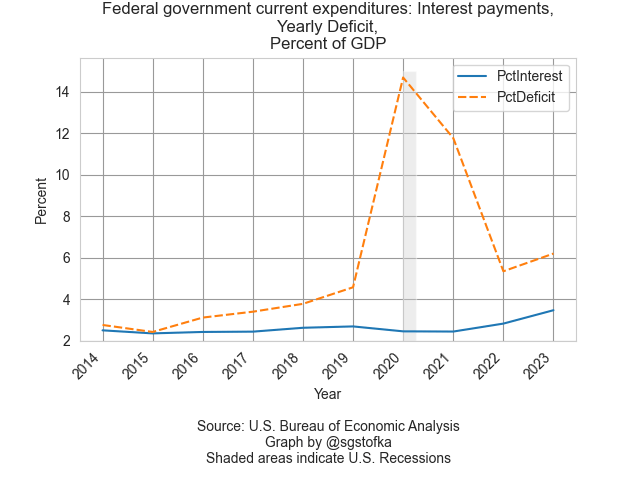

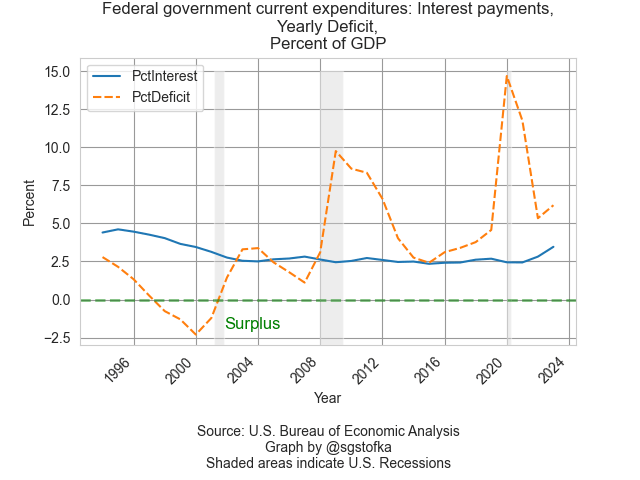

The private economy is not capable of supporting the current social and defense spending at this level of taxation. Neither political party wants to compromise on their priorities and the interest expense on the debt will grow, exacerbating the tensions between both political parties. That interest is now 3.5% of GDP, about the same as defense and Medicare spending. That interest is entirely funded by a deficit. We are borrowing to pay the interest on the debt we have accumulated.

The blue line will continue to rise, pushing the orange line upward as well. The political parties will stay entrenched in their ideological bunkers, creating a daily drama covered by mainstream and social media whose coverage incentivizes posturing rather than compromise. Just as Britain did in the inter-war period a century ago, we are steadily losing resilience, ready to falter at the next crisis.

Notes on social programs: Defense spending is series FDEFX at the FRED database. Medicaid is series W729RC1. Medicare is W824RC1. Each series link is a percentage of GDP.

This week’s letter continues my analysis of the many roles of the federal government, comparing spending, tax revenues and the federal debt that has accumulated since 9-11. Governments accumulate debt by spending more than they collect in tax revenues. Farmers, businesses and households appreciate the subsidies and support from government but resist paying the taxes to fund those programs. The private marketplace depends on government funding of nascent technologies that may take decades to commercialize. Examples include the internet, the development of semiconductors, lithium batteries and the funding of pharmaceutical research. Investment in military readiness has spurred advancements in aerospace and satellite technology, the GPS that connects our phones and the Kevlar clothing that protects our soldiers and police officers. Critics may ridicule a government investment in solar manufacturer Solyndra, but it was also heavy government funding that provided the cash flow for SpaceX and Tesla.

In last week’s letter I showed that private investment and government spending and investment both averaged about 18% of GDP over the past three decades. A closer look at those two series shows how they complement and compete with each other. In the graph below, private investment dipped from 19% of GDP in 2006 to below 14% in 2009. As a percent of GDP, government spending and investment took up some of the slack.

As many people lost their jobs, they became eligible for Medicaid or food stamps. Both of these programs are included in government spending because the programs directly or indirectly provide people with goods or services. The graph above does not include increased unemployment insurance payments during the recession. These are included in government transfers since this is money, not services, transferred from the government to individuals. Policymakers refer to this combination of support programs as automatic stabilizers, providing assistance to households during hard economic times.

A recent analysis by the Congressional Budget Office (CBO) found that these automatic stabilizers were not “key drivers of debt over the long-term.” The federal debt was growing because government spending was increasing at a faster pace than revenues. The chart below shows spending and revenues for the past thirty years in a natural log form to portray the trends of change more clearly.

For most of the past three decades, revenue growth, the orange dashed line in the graph above, lagged government spending, the blue line. Note that this revenue series (FRED Series FYFR) does not include Social Security taxes. The growth in government spending showed some moderation only during Obama’s term and that was the worst time to slow the growth of government spending and investment. The Great Recession of 2007-2009 was the worst economic downturn since the 1930s Depression, surpassing the pain of the back-to-back recessions of the early 1980s.

Biden was vice-President during that recovery and was determined not to repeat that mistake in the aftermath of the Covid-19 pandemic. Although the Democratic majorities in the House and Senate were slim, unified government helped the effort to pass the Inflation Reduction Act and the CHIPS Act. Both pieces of legislation committed government funds to support investment in clean energy development and semiconductor manufacturing. Such commitment spurred private investment in the energy industry. In 2023 field production of crude oil surpassed 2019 levels, according to the Energy Information Administration (EIA). They report that natural gas output was up 2% in the first year of Biden’s term, then accelerated to 5% growth in 2022 and 2023 following Russia’s attack on Ukraine.

Despite big increases in the deficit after 9-11, and an accumulated debt of $22 trillion held by the public, the interest share of GDP has remained below the levels of the 1990s. In 2001, China was admitted into the World Trade Organization. As imports from China increased, we paid for them with U.S. Treasury debt, helping to keep interest rates low for most of the past two decades.

Unlike individuals and corporations, governments can buy their own debt. Unless a majority of that debt is sold in the private marketplace, there is no independent evaluation of the creditworthiness of that debt. At the end of last year, 65% of the total Federal debt was privately held, the highest percentage since 1997 (see notes). Including the Treasuries held by independent Federal Reserve banks, the percentage is close to 80%. A recent report from the Center for Strategic and International Studies (CSIS) calculates the percentage of debt held by two of our largest trading partners, China and Japan, at 5.8%. The wide ownership of U.S. debt validates it as a low-risk financial instrument.

The global financial system depends on tradeable sound securities. When the financial crisis undermined confidence in mortgage securities, private investment declined sharply, and it would do so again if investors doubted the soundness of Treasury securities. The recent CBO report points out a weakness in public policy that the Congress must resolve or risk damaging the credit of U.S. securities. 1997 was the last year when Congress submitted a budget by the deadline, according to the Congressional Research Service. When is the moment when the private debt market loses hope that Congress can match its spending and revenues? No one can forecast a stampede to safety but in hindsight many will claim to have seen the exit signs.

Keywords: investment, debt, interest, Treasuries, government spending, taxes, automatic stabilizers

According the March 2024 Treasury bulletin, total Federal debt was $34 trillion. $21.7 trillion was privately held – about 65%. See Table OFS-2 of the March bulletin. Privately held debt plus $5.2 trillion of Treasuries held by independent Federal Reserve banks constitute Federal Debt Held by the Public (FRED Series FYGFDPUN) and is close to 80% of total federal debt. For a thirty-year series of the public’s portion of total debt, see https://fred.stlouisfed.org/graph/?g=1hYFV. Until the 2008 financial crisis Federal Reserve banks held less than 10% of total debt. During the pandemic, that share rose to 21%. At the end of 2023, the share was 15.4%.

This week’s letter is about the debt ceiling. It has been ten days since Janet Yellen, Secretary of the Treasury, began using “extraordinary measures” to pay federal obligations as the nation waits for Congress to raise the debt ceiling. The U.S. is the only country in the world that requires legislative authorization of its debt after the legislature has already authorized the spending, then appropriated the money for that expense.

Each year, the federal government and each of the states conducts an annual appropriations process that allocates money to each state or federal department or agency. By law, states must balance their budgets – in a pro forma manner, at least. They sometimes employ accounting mechanisms to defer expenses to a later year or accelerate revenues into a current fiscal year to achieve that balance. The federal government does not have a balanced budget constraint but Congress does occasionally play a dangerous game of budget “chicken” when it wants to send a message to the other party.

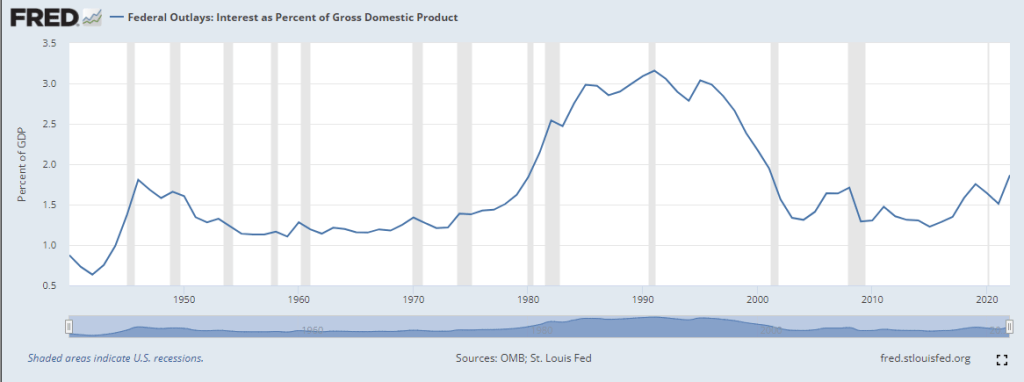

Political parties are ever conscious of their branding and each claims to be a good financial steward of the public’s taxes. Each claims that the other party is irresponsible. Paying the interest on the debt takes funding from other programs without doing anything. While this may be true and the interest on the debt is rising, it is less than 2% of GDP, far below the 2.5% – 3% of GDP during the 1980s and 1990s.

The press, politicians and public argue over who is responsible and whether to cut programs or increase revenues. When Republicans are out of power, as they are now, they call for spending cuts. Democrats call for revenue increases, particularly higher taxes on the rich. When Republicans were in power from 2017-2019, they increased the deficit each year, ending 2019 with a deficit of almost $1 trillion. In 2020, the deficit was $3.1 trillion. A month after the 2020 election was over, Congress added another $920 billion for Covid relief. The Trump administration added $6.5 trillion to the debt, or 21% of today’s total debt of $31 trillion.

Shortly after Mr. Biden took office in January 2021, Congress passed the American Rescue Act which provided another $1.9 trillion in relief. The two relief packages before and after the start of Biden’s term added up to $2.8 trillion and was responsible for the entirety of the 2021 deficit of $2.775 trillion. The Republican House will pin the blame for the debt on the Biden administration and programs like Social Security and Medicare. When a party is out of power, they can indulge in what is called position-taking. The firebrand rhetoric is popular with the Republican base and, since there is no possibility that those programs will be cut, politicians can claim to be prudent or for small government. When a party is actually in power, politicians have to be careful with political blustering. Their constituents are more likely to think that such cuts are possible and will vote them out of office.

For forty years, the Republican party has run on a theoretical assumption that tax cuts will spur enough economic activity that the increased tax revenue will more than pay for the cuts. There is no evidence supporting that claim but claims do not need evidence to be effective at raising funds and winning votes. For almost sixty years, Democrats have touted federal social programs as a path to greater equality and equitability.

In any game of chicken, the danger is that neither side gives in. Relying on estimates of income tax revenue in the next few months, some economists project that Secretary Yellen can continue to take ever more extraordinary measures until June. At the last big debt limit showdown in 2011, people argued over the constitutionality of the Treasury printing a $1 trillion coin and handing it over to the Federal Reserve to cover any expenses, including interest payments and bond redemption. This year, the idea is again a popular debating point on social media.

Like the filibuster, the debacle of the debt limit debate continues because each party wants to have power yet check the other party’s power, a dilemma that neither can escape. They are two horses harnessed together pulling the wagon of state. With reins in hand, the public is under the impression that it is driving the wagon but it is not. The parties pay attention only to the harness that binds each to the other.

Two quick asides before I get into this week’s topic. A cricket perched on the top of a 7′ fence. It drew up to the edge of the top rail, learned forward, raised its rear legs as though to jump, then settled back. It did this twice more before jumping 8′ out then down into a soft landing on some ground cover. How far can crickets see, how often do they injure a leg if they land incorrectly and do they get afraid?

The bulk of the personal savings in this country is held by the top 20% of incomes, and it is this income group that received the lion’s share of the 2017 tax cuts. It’s OK to bash the rich but that top 20% probably includes our doctor and dentist. Before you start drilling or cutting me, I want to make it perfectly clear that I was not criticizing you, Doc.

In 2016, the top quintile – the top 20% – earned 2/3rds of the interest and dividend income (Note #1). Due to falling interest rates over the past three decades, real interest and dividend income has not changed. Real capital has doubled and yes, much of it went to those at the top, but the income from that capital has not changed. That is a huge cost – a hidden tax that gets little press. The real value of the public debt of the Federal Government has quadrupled since 1990, but it pays only 20% more in real interest than it did in 1990 (Note #2). Here’s a graph of personal interest and dividend income adjusted to constant 2012 dollars. Thirty years of flat.

Ok, now on to a story. Economists build mathematical models of an economy. I wanted to construct a story that builds an economy that gradually grows in complexity and maybe it would help clarify the relationships of money, institutions and people.

Let’s imagine a group of people who move into an isolated mining town abandoned several years earlier. The houses and infrastructure need some repairs but are serviceable and the community will be self-sufficient for now. The homeowners form an association to coordinate common needs.

The association needs to hire lawn, maintenance and bookkeeping services, and security guards to police the area and keep the owners safe. How does the association pay for the services? They assess each homeowner a monthly fee based on the size of the home. How do the homeowners pay the monthly fee? Each homeowner does some of the services needed. Some clean out the gutters, others fix the plumbing, some keep the books and some patrol the area at night. They work off the monthly fee.

How do they keep track of how much each homeowner has worked? The association keeps a ledger that records each owner’s fee and the amount worked off. The residents sometimes trade among themselves, but it is rare because barter requires a coincidence of wants, as economists call it. Mary, an owner, needs some wood for a project and Jack has some extra wood. They could trade but Mary doesn’t have anything that Jack wants. He tells Mary to go down to the association office and take some of her time worked off her ledger and credit it to Jack’s monthly fee. Mary does this and they are both happy (Note #3).

As other owners learn of this idea and start trading work credits, the association realizes it needs a new system. It prints little pieces of paper as a substitute for work credits and hands them out to owners who perform services for the association. These pieces of paper are called Money (Note #4).

The

money represents the association’s accounts receivable, the fees owed and

accruing to the association, and the pay that the association owes the owners

for the work they have done. Then the association notices that there are some

owners who are not doing as well as others. It assesses an extra fee each month

from those with larger homes and gives that money to needy homeowners. These are called transfers because the owners

who receive the money do not trade any real goods or services to the association.

In this case the association acts as a broker between two people. Let’s call

these passive transfers. We can lump these transfers together with exchanges of

goods and services.

Then

some people from outside the area start stealing stuff from the homeowners. The

association needs to hire more security guards, but homeowners don’t want to

pay a special one-time assessment to pay for the extra guards.

Instead

of printing more Money, the association prints pieces of paper called Debt.

Homeowners who have saved some of their money can trade it in for Debt and the

association will pay them interest. Homeowners like that idea because Money

earns no interest and Debt does. The association uses the Money to pay for the

extra security guards.

But

there are not enough people who want to trade in their Money for Debt, so the

association prints more Money to pay the extra security guards.

Let’s pause our story here to reflect on what the words inflation and deflation mean. Inflation is an increase in overall prices in an economy; deflation is a decrease (Note #5). Inflation occurs when the supply of money fuels a demand for goods and services that is greater than the supply of goods and services. Ok, back to our story.

So

far so good. All the Money that the association has printed equals a trade or a

passive transfer. Let’s say that the association needs more security guards and

no one else wants to work as a security guard because they can make more Money

doing jobs for other homeowners. The association makes a rule called a Draft.

Homeowners of a certain age and sex who do not want to work as security guards

will be locked up in the storage room of the community center.

Now

there’s a problem. Because the association has taken some homeowners out of the

customary work force, those people are not available for doing jobs for other

homeowners, who must pay more to contract services. This is one of several

paths that leads to inflation. To combat that, the association sets price

controls and limits the goods that homeowners can purchase. After a while, the

outsiders are driven off and the size of the security force returns to its

former levels.

Now all the extra Money that the association printed to pay for the security force has to be destroyed. As homeowners pay their dues, the association retires some of the money and shrinks the Money supply. However, there is a time lag, and prices rise sharply (Note #6).

Over

the ensuing decades, there are other emergencies – flooding after several days

of rain, a sinkhole that formed under one of the roadways, and a sewer system

that needed to be dug up and replaced. The association printed more Debt to cover

some of the costs, but it had to print more Money to pay for the balance of

repairs. Because the rise in the supply of Money was a trade for goods and

services, inflation remained tame.

There

didn’t seem to be any negatives to printing more Money, so the homeowners

passed a resolution requiring that the association print and pay Money to

homeowners who were down on their luck. These were active transfers – payments

to homeowners without a trade in goods and services and without some offsetting

payment by the other homeowners.

So

far in our story we have several elements that correspond with the real world: currency,

taxes, social insurance, the creation of money and debt and the need to pay for

defense and catastrophic events. Let’s continue the story.

With

the newly printed Money, those poorer homeowners could now buy more goods and

services. The increased demand caused prices to rise and all the homeowners

began to complain. Realizing their mistake, they voted on an austerity program

of higher homeowner fees and lower active transfers to poorer homeowners.

Because

homeowners had to pay higher fees, they didn’t have enough extra Money to hire

other services. Some residents approached the association and offered to repair

fences and other maintenance jobs, but the association said no; it was on an

austerity program and cutting expenses. Some residents simply couldn’t pay

their fees and the problem grew. The association now found that it received

less Money than before the higher fees and Austerity program. It cut expenses

even more, but this only aggravated the problem.

Finally,

the association ended their Austerity program. They printed more Money and hired

homeowners to make repairs. Several homeowners came up with a different idea.

There is another housing development called the Forners a few miles away. They

are poorer and produce some goods for a lower price. The homeowners can buy

stuff from the Forners and save money. There are three advantages to this

program:

Things bought from the Forners are

cheaper.

Because the homeowners will not be

using local resources, there will be less upward pressure on prices.

The homeowners will pay the

association for the goods bought from the Forners and the association will pay

the Forners community with Debt, not Money. Since it is the creation of Money that

led to higher prices, this arrangement will help keep inflation stable.

As

the homeowners buy more and more stuff from the Forners, the money supply

remains stable or decreases. After several years, homeowners are buying too

much stuff from the Forners and there is less work available in the community.

As homeowners cannot find work, they again fall behind in paying their monthly

fees.

Several

of those in the association realize that they don’t have enough Money to go

around in the community. There is a lot to do, and the homeowners draw up a

wish list: repairs to the roads and helping older homeowners with shopping or

repairs around their home are suggested first. A person who is out of work

offers to lead tours and explain the biology of trees for schoolchildren. The

common lot near the clubhouse could use some flowers, another homeowner

suggests. I could use a babysitter more often, one suggests, and everyone nods

in agreement. I could teach a personal finance class, a homeowner offers.

Another offers to read to homeowners with bad eyesight and be a walking

companion to those who want to get more exercise.

Everyone who contributes to the welfare of the community gets paid with Money that is created by the association. What should we call the program? One person suggests “The Paid Volunteer Program,” and some people like that. Another suggests, “The Job Guarantee Program” and everyone likes that name so that’s what they called it (Note #7).

So

far in this story we have two key elements of an organized society:

Money – a paper currency created by the

homeowner association.

Debt – the amount the association owes

to homeowners (domestic) and the Forners (international).

Next

week I hope to continue this story with a transition to a digital currency, banks

and loans.

//////////////////////

Notes:

In 2016, the top 20% of incomes with more than $200K in income, earned more than 2/3rds of the total interest and dividends. IRS data, Table 1.4

In 2018 dollars, the publicly held debt of the Federal government was $4 trillion in 1990, and $16 trillion now. In 2018 dollars, interest expense was $500B in 1990, and is $600B now.

In David Graeber’s Debt: The First 5000 Years, there is no record of any early societies that had a barter system. They had a ledger or money system from the start.

In the Wealth of Nations, Adam Smith – the “father” of economics – defined money as that which has no other value than to be exchanged for a good. This essential characteristic makes money unique and differentiates paper money from other mediums of exchange like gold and silver.

An easy memory trick to distinguish inflation from deflation. INflation = Increase in prices. DEflation = DEcrease.

The account of the increased force of security guards – and its effect on prices and regulations – is the simple story of money and inflation during WW2 and the years immediately following. The process of rebalancing the money supply by the central bank is difficult. Monetary policy during the 1950s was a chief contributor to four recessions in less than 15 years following the war.

A Job Guarantee program is a key aspect of Modern Monetary Theory.

Until the financial crisis, I thought that other people’s debt was their problem. In 2008, debt became a nation’s problem and a national conversation with two aspects – the moral and the practical. Moral conversations are not confined to church; they drive our politics and policy. Many laws contain some language to contain moral hazard, which is the danger that language loopholes in a law or policy promote the opposite of the intended effect of the law. This is particularly true of many entitlement policies. Let’s leave the moral conversation for another day and turn to the practical aspects of current policy.

Bankers learned their lesson during the financial crisis, didn’t they? Maybe not. A decade of absurdly low interest rates has starved those who depend on the income earned by owning debt. Even a savings account is money loaned to a bank, a debt that the bank must pay to the account holder. In their hunger for income, investors have turned to less prudent debt products. So long as the economy remains strong, no worries.

A fifth of conventional mortgages are going to people whose total debt load, including the mortgage, is more than 45% of their pre-tax income. By comparison, at the market’s exuberant peak in late 2007, 35% of conventional mortgages were going to such households, who were especially vulnerable when monthly job gains turned negative in early 2008.

The real estate analytics firm Core Logic also reports that Fannie Mae has started backing mortgages to those with total debt loads up to 50%. FICA, federal, state and local income taxes can amount to 25% of a paycheck (Princeton Study). Add in 45% of that gross pay for mortgage and debt payments, and there is only 30% left for food, gas, home repairs and utilities, child care, etc.

I’ll convert these percentages to dollars to illustrate the point. A couple grossing $80,000 might have a take home pay of $60,000. The couple has $36,000 in mortgage and other debt payments (45% of $80,000). They have $24,000, or $2000 a month for everything else. This couple is vulnerable to a change in their circumstances: a layoff or a cut back in hours, some unexpected expense or injury.

For those who get a conventional loan despite their heavy debt load, where is the money coming from? Banks suffered huge losses during the financial crisis. The Federal Reserve tightened capital requirements for banks’ loan portfolios, forcing them to improve the overall quality of their debt. As a result, banks turned away from their most lucrative customers – subprime borrowers and those with heavy debt loads who must pay higher interest on their loans. Profits in the financial industry fell dramatically. A broad composite of financial stocks (XLF) has still not regained the price levels of 2007.

The banking industry employs some very smart people. What solution did they create? The big banks now loan money to non-financial companies who loan the money to subprime borrowers. After bundling the consumer loans into securities, the non-financial companies use the proceeds to pay the big banks back. In seven years this kind of borrowing has expanded seven times to $350 billion. Doesn’t this look like the kind of behavior that almost took down the financial system in 2008? The banks say that this system isolates them from exposure to subprime borrowers. If large scale job losses cause a lot of loan defaults, it is the investors who will bear the pain, not the banks. Same song, different lyrics.

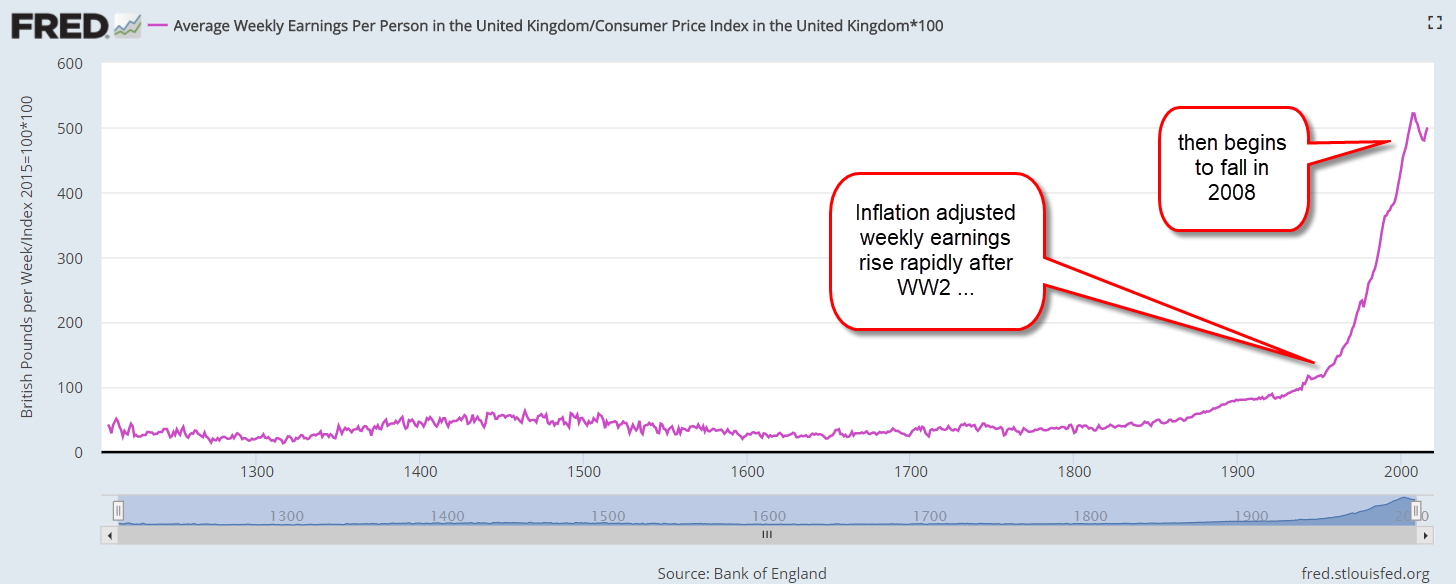

The 2008 financial crisis is best summed up with a chart from the Federal Reserve. In the post WW2 economy, the weekly earnings of British workers rose steadily. The growth is especially strong when compared to the earlier decades of the 19th and 20th centuries. In 2008, earnings peaked.

Developed countries depend on the steady growth of tax receipts generated by weekly earnings. An assumption of 3% real GDP growth underlies the health and continuation of post-war social welfare policies. For more than a decade, the U.S. and U.K. have had less than 2% GDP growth. Both governments have had to borrow heavily to fund their social support programs. How long can they increase their debt at such a rapid pace?

I am reminded of a time more than 40 years ago when New York City held a regularly scheduled auction to sell bonds to fund their already swollen debt load. None of the banks showed up to bid for the bonds. The city is the financial center of the world. The lack of interest stunned city officials. To avoid a messy bankruptcy, the city turned to the Federal government for a loan (NY Times).

The Federal government is not a city or state, of course. It has extraordinary legal and monetary power, and its bonds are a safe haven around the world. But there could come a time when investors demand higher interest for those bonds and the rising annual interest on the debt squeezes spending on other domestic programs.

Debt causes stress. Stress causes anxiety. Anxiety weakens confidence in the future and causes investment to shrink. Falling investment leads to slower job growth. That causes profits and weekly earnings to fall which reduces tax receipts to the government. That increases debt further, and the cycle continues. Other people’s debt is everyone’s problem after all.

Republicans used to care about yearly budget deficits when Obama was President. Since Obama left office, the budget deficit is up 20%. As a percentage of GDP, 2017’s deficit was above the forty-year average of deficits (Treasury Dept press release). At the end of the Obama term, the gross federal debt was 77% of GDP. In ten years, the Congressional Budget Office estimates that percentage will be over 90%. (Spreadsheet ) That estimate does not include the lower revenues from the tax cuts passed in December.

During the two Bush terms, Republican deficit hawks, genuinely concerned about budget deficits, were overruled by a majority of Republicans who paid only political lip service to common sense budgeting.

The Federal Government’s fiscal year runs from October to September. At the end of February, the fiscal year was five months old. According to the Treasury’s monthly budget statement, this fiscal year’s deficit has gone up 10%. Because of the tax cut passed in December, payroll tax collections are down. Because of higher interest rates, the government paid an extra $40 billion on the federal debt in the first five months of this fiscal year, which began October 2017. $40 billion is half of the food stamp program. Debt matters. The government is going into more debt to pay the interest on the existing debt.

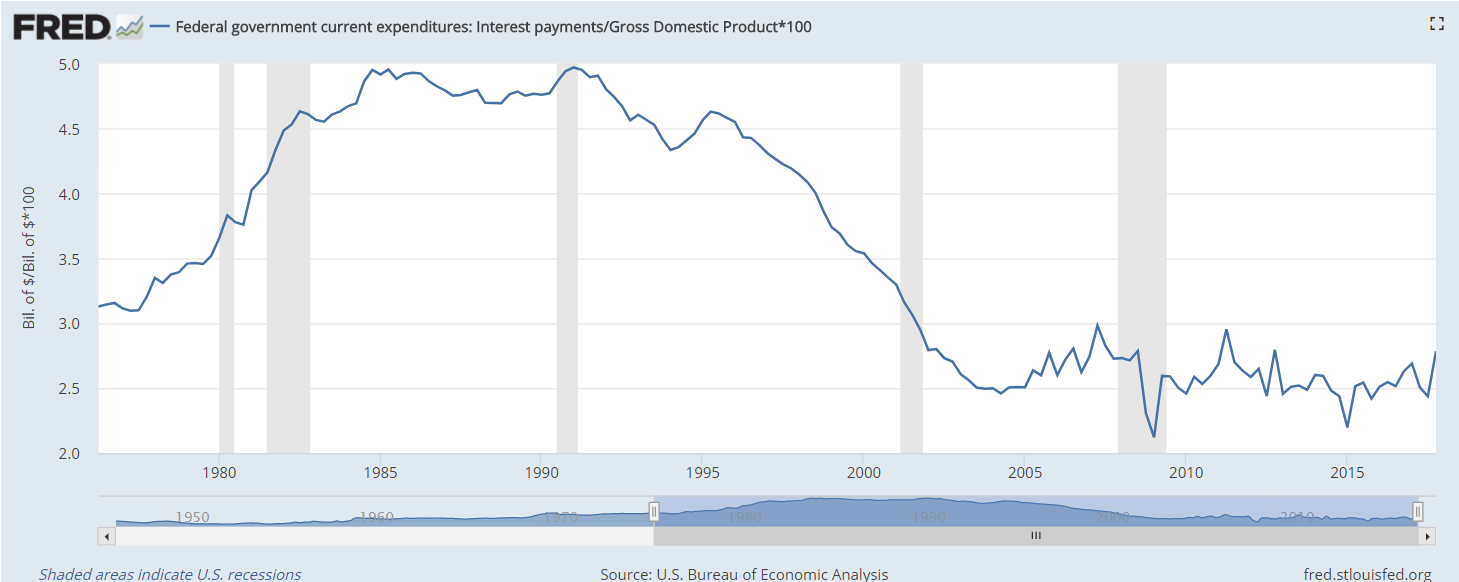

The government paid $550 billion in interest last year and is estimated to pay over $600 billion this year. That is just a $100 billion less than the defense budget. Because interest rates are historically low, the interest as a percent of GDP is low. We cannot expect that they will remain low.

Interest rates were low in the 1950s. By 1970, they were over 7% and had climbed to 14% by 1980. Since the financial crisis ten years ago, central banks in China, Europe and the U.S. have been buying government debt. Central banks don’t demand higher interest. As their role diminishes, price-sensitive buyers like pension funds and households will demand higher interest rates (Bloomberg article). Recent Treasury debt auctions have been lightly subscribed, and the Fed is having to step in as a buyer to artificially make a market. Remember, the Fed is just another pants pocket of the Federal Government. In essence, the Federal Government is buying its own debt. What can’t continue forever, won’t.

///////////////////

Housing

Have you gotten the impression that the housing market is going gangbusters? As a percent of GDP, housing investment is double what it was at the lows of the recession. The bad news is that current levels are near the historic lows of the post WW2 economy.

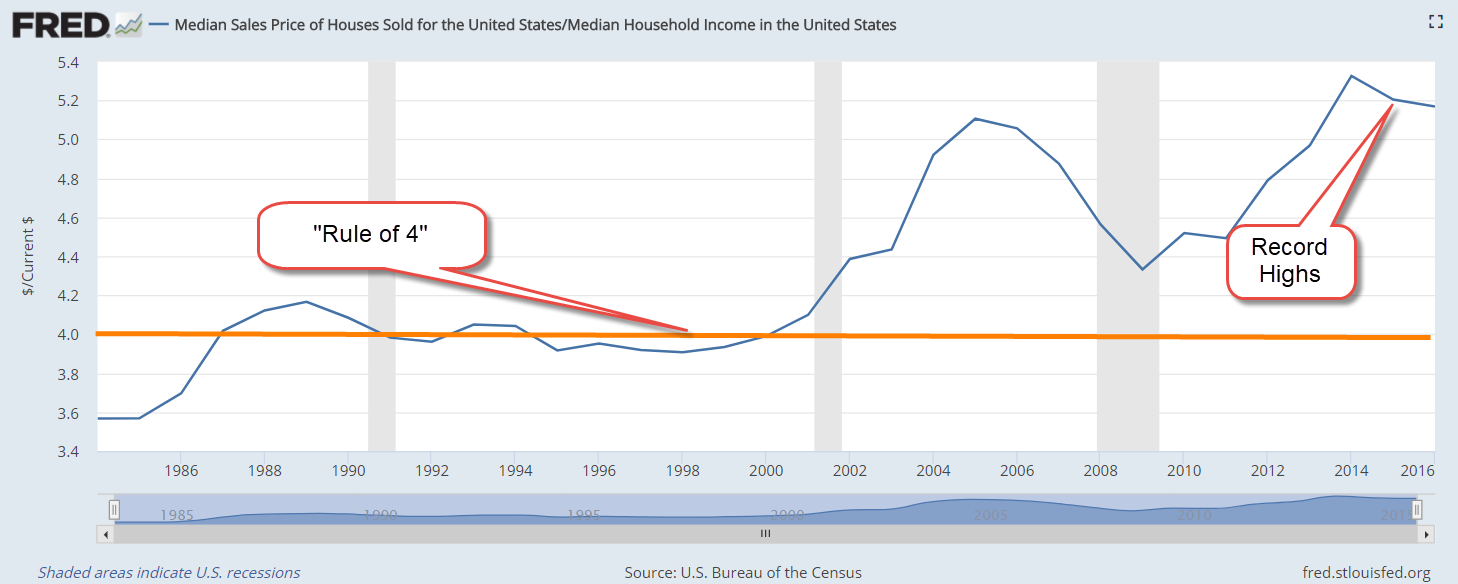

On the other hand, housing affordability has hit all time lows. A prudent rule of thumb is that a person or family should not spend more than 25% of their income on housing. A corollary of that rule is that a household should not buy a home that is more than 4 times their annual income. At 5.2, the current ratio is far above a prudent rule of thumb.

Government debt levels make the government, and us, vulnerable to any loss of confidence. Low housing investment makes the economy less resilient. High housing costs make it more difficult for families to save. In a downturn, more families must turn to government for benefits. Saddled with high debt levels and interest payments, government is less able and willing to extend benefits. The cycle turns vicious.

As summer comes to a close and the sun drifts south for the winter, the porridge is not too hot or too cold.

********************

Coincident Index

The index of Leading Indicators came out last week, showing increased strength in the economy. Despite its name, this index has been notoriously poor as a predictor of economic activity. The Philadelphia branch of the Federal Reserve compiles an index of Coincident Activity in the 50 states, then combines that data into an index for the country.

This index is in the healthy zone and rising. When the year-over-year percent change in this index drops below 2.5%, the economy has historically been on the brink of recession. The index turns up near the end of the recession, and until the index climbs back above the 2.5% level, an investor should be watchful for any subsequent declines in the index.

As with any historical series, we are looking at revised data. When this index was published in mid-2011, the percent change in the index was -7% at the recession’s end in mid-2009. Notice that the percent drop in the current chart is a bit less than 5%. This may be due to revisions in the data or the methodology used to compile the index.

**************************

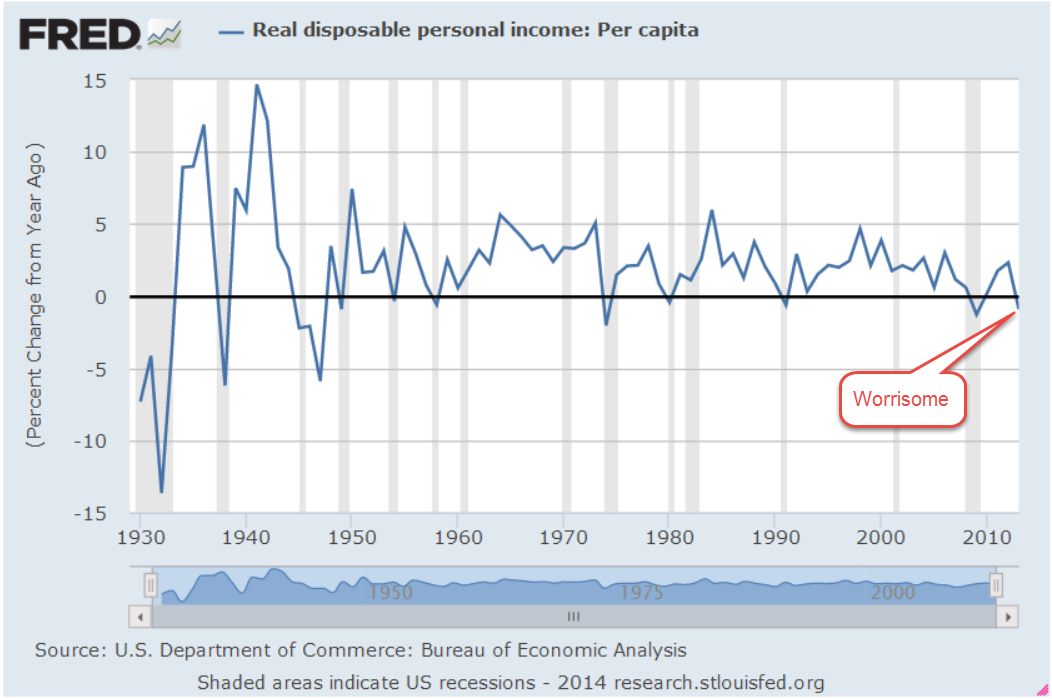

Disposable Income The Bureau of Economic Analysis (BEA) produces a number of annual series, which it updates through the year as more complete data from the previous year is received. 2013 per capita real disposable income, or what is left after taxes, was revised upward by .2% at the end of July but still shows a negative drop in income for 2013. While all recessions are not accompanied by a negative change in disposable income, a negative change has coincided with ALL recessions since the series began at the start of the 1930s Depression.

Many positive economic indicators make it highly unlikely that we are either in or on the brink of recession. Clearly something has changed. Something that has routinely not been counted in disposable personal income is having some positive effect on the economy. In 2004, the BEA published a paper comparing the methodology they use to count personal income and a measure of income, called money income, that the Census Bureau uses. What both measures don’t count in their income measures are capital gains.

Unlike BEA’s measure of personal income, CPS money income excludes employer contributions to government employee retirement plans and to private health and pension funds, lumps-sum payments except those received as part of earnings, certain in-kind transfer payments—such as Medicare, Medicaid, and food stamps—and imputed income. Money income includes, but personal income excludes, personal contributions for social insurance, income from government employee retirement plans and from private pensions and annuities, and income from interpersonal transfers, such as child support. (Source)

Analysis (Excel file) of 2012 tax forms by the IRS shows $620 billion in capital gains that year, about 5% of the $12,384 billion in disposable personal income counted by the BEA. An acknowledged flaw in the counting of disposable income is that the total reflects the taxes that individuals pay on the capital gains (deducted from income) but not the capital gains that generated that taxable income. Although 2013 data is not yet available from the IRS, total personal income taxes collected rose 16%. We can suppose that the 30% rise in the stock market generated substantial capital gains income.

*************************

Interest Every year the Federal Government collects taxes and spends money. Most years, the spending is more than the taxes collected – a deficit. The public debt is the accumulation of those annual deficits. It does not include money “borrowed” from the Social Security trust fund as well as other intra-governmental debt, which add another third to the public debt. (Treasury FAQ) This larger number is called the gross debt. At the end of 2012, the public debt was more than GDP for the first time.

The Federal Reserve owns about 15% of the public debt. But wait, you might say, isn’t the Federal Reserve just part of the government? Well, yes it is. Even the so-called public debt is not so public. How did the Federal Reserve buy that government debt? By magic – digital magic. There is a lot of deliberation, of course, but the actual buying of government debt is done with a few dozen keystrokes. Back in ye olden days, a government with a spending problem would have to melt down some of its gold reserves, add in some cheaper metal to the mix and make new coins. It is so much easier now for a government to go to war or to give out goodies to businesses and people.

Despite the high debt level, the percent of federal revenues to pay the interest on that debt is relatively low, slightly above the average percentage in the 1950s and 1960s but far below the nosebleed percentages of the 1980s and 1990s.

As the boomer generation continues to retire, the Federal Government is going to exchange intra-governmental debt, i.e. the money the government owes to the Social Security trust funds, for public debt. As long as 1) the world continues to buy this debt, and 2) interest rates stay low, the impact of the interest cost on the annual budget is reasonable. However, the higher the debt level, the more we depend on these conditions being true.

************************

Watch the Percentages As the SP500 touched and crossed the 2000 mark this week, some investors wondered whether the herd is about to go over the cliff. The blue line in the chart below is the 10 month relative strength (RSI) of the SP500. The red line is the 10 month RSI of a Vanguard fund that invests in long term corporate and government bonds. Readings above 70 indicate a strong market for the security. A reading of 50 is neutral and 30 indicates a weak market for the security. The longer the RSI stays above 70, the greater the likelihood that the security is getting over-bought.

Long term bonds tend to move in the opposite direction of the stock market. While they may both muddle along in the zone between 30 and 70, it is unusual for both of them to be particularly strong or weak at the same time. We see a period in 1998 during the Asian financial crisis when they were both strong. They were both weak in the fall of 2008 when the global financial crisis hit. Long term bonds are again about to share the strong zone with the stock market.

Let’s zoom out even further to get a really long perspective. Since November 2013, the SP500 index has been more than 30% above its 4 year average – a relatively rare occurrence. It happened in 1954 – 1956 after the end of the Korean War, again in December of 1980, during the summer months of 1983, the beginning of 1986 to the October 1987 crash, and from the beginning of 1996 through September 2000.

In the summer of 2000, the fall from grace was rather severe and extended. In most cases, including the crash of 1987, losses were minimal a year after the index dropped back below the 30% threshold. When the market “gets ahead of itself” by this much, it indicates an optimism brought on by some distortion. It does not mean that an investor should panic but it is likely that returns will be rather flat over the following year.

The index rarely gets 30% below its 4 year average and each time these have proven to be excellent buying opportunities. The fall of 1974, the winter months of 2002 – 2003, and the big daddy of them all, March 2009, when the index fell almost 40% below its 4 year average.

************************

GDP The Bureau of Economic Analysis (BEA) released the 2nd estimate of 2nd quarter GDP growth and surprised to the upside, revising the inital 4.0% annual growth rate to 4.2%. As I noted a month ago, the first estimate of 2nd quarter growth included a 1.7% upward kick because of a build up of inventory, which seemed a bit high. The BEA did revise inventory growth down to 1.4% but the decrease was more than offset primarily by increases in nonresidential investment. A version of GDP called Final Sales of Domestic Product does not include inventory changes. As we can see in the graph below, the year-over-year percent gain is in the Goldilocks zone – not strong, but not weak.

New orders for durable goods that exclude the more volatile transportation industries, airlines and automobiles, showed a healthy 6.5% y-o-y increase in July. Like the Final Sales figures above, this is sustainable growth.

***********************

Takeaways Economic indicators are positive but market prices may have already anticipated most of the positive, leaving investors with little to gain over the following twelve months.