Thanks to Lydia who sent a link to a Toronto Globe and Mail interview by Heather Scoffield with Laurence A. Tisch, professor of history at Harvard University, and author of The Ascent of Money, A Financial History of the World. Some notable comments:

“This is a very unfair crisis. Here is the world’s biggest economy, which gave us subprime mortgages, rampant securitization, the collateralized debt obligation, Lehmann Brothers, Merrill Lynch. The epicentre is the United States, but the rest of the world, and particularly America’s trading partners, will get hit harder than the U.S. … because the U.S. retains the safe-haven status.” Safe haven is when, in a crisis, the rest of the world buys U.S. Treasury notes and bonds.

“Property ownership is something that our societies, particularly English-speaking societies, seem to be drawn towards. The notion that the majority of people should own their own homes dated from the 30s. It didn’t really become a reality until the 50s. We’ve sort of pushed the home ownership rate up to what seems to be its maximum, and beyond. It will clearly come down. The lesson of the subprime crisis is that you shouldn’t give mortgages to people who can’t afford them.”

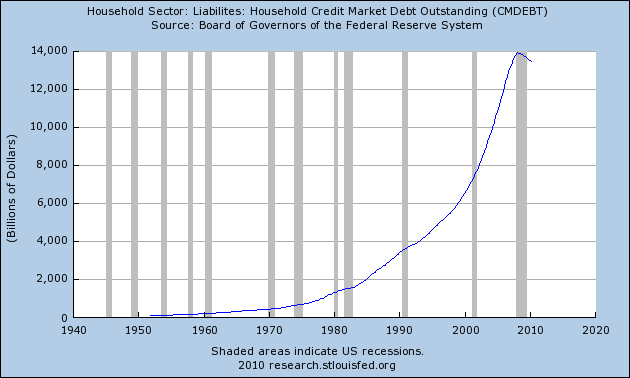

“It’s a crisis of excessive debt, the deleveraging process has barely begun, the U.S. consumers are not going to suddenly bounce back and hit the shopping malls just because they get a tax cut. The savings rate is going to continue to rise. These processes have tremendous momentum that quite clearly differentiates them from anything that we’ve seen, including the early 80s, including 73, 74, 75. Those big crises, the ones that we have lived through, were bad. But seems certain to be deeper, and more protracted. “

“August, 2007 was when this crisis began. And if you were really watching the markets carefully, April is when it began, when the various hedge funds started to hemorrhage. The stock markets carried on until October of that year. And in many ways, consumer behaviour in the U.S. did not change until the third quarter of 2008.”

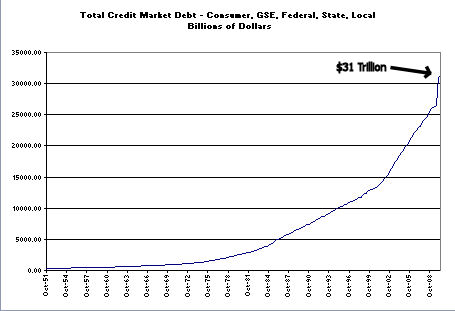

“$2-trillion worth of debt is going to hit the market this year, maybe more. Supply is exploding just when demand is contracting.” “There is still this inertia that prevents the dollar from falling off a cliff, that keeps the Treasury market from falling off a cliff.” “If I were in the market to buy distressed assets, I would wait, I would wait a bit longer until they’re really desperate. And it might even be better to wait until they’re bankrupt.”

“From John Law in 1719 to Alan Greenspan in the late 90s, there’s always a banker, there’s always a central banker making credit too readily available. The second thing is, though, that regulation may not prevent that.”

“Monetary policy evolved in a peculiar way in the 1990s towards de facto or de jure targeting of inflation, an increasingly narrow concept of inflation – core CPI.” “When the central bankers got together at Jackson Hole, the view that emerged from the debate in the late 90s was, we shouldn’t really pay attention to asset prices in the setting of monetary policy.”

“European banks are far more leveraged than American banks.”

“But one of the things that I find troubling about the administration is the degree to which is has ceded power to Congress. It’s almost like it’s a parliamentary system.”

“If you subtract mortgage equity withdrawal from the Bush years, the real underlying rate of growth of the U.S. economy was 1 per cent.”

“If you have a more equitable redistribution through the tax system, which Obama is committed to, it might actually be no discernible downside for middle America and lower-class Americans. So many of the benefits of the boom went to the elites.”