November 3rd, 2013

In this week’s title is the new government top level domain name: gum for gummint or gummed up. But before I get into that, a few side notes on the economy.

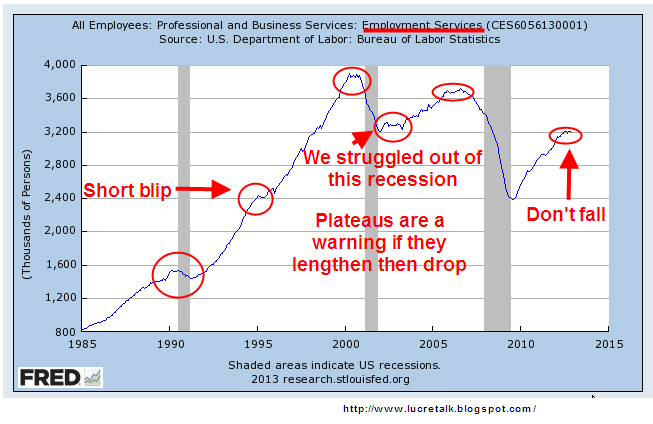

On Friday, the Institute for Supply Mgmt released October’s ISM manufacturing report, which again showed that the manufacturing sector of the economy is humming along. The monthly report on Factory Orders will be released this coming Monday, followed by the non-manufacturing ISM report on Tuesday. The non-manufacturing sector has slowed from robust growth readings during the summer but are expected to still be a strong 54 to 56. I’ll update the CWI that I have been charting since the spring.

On Wednesday, the payroll firm ADP released their estimate of job growth in the private sector during October. The 130,000 net job gains came in under expectations and ADP noted a downward revision of about 12% for the previous months employment gains. Normally, the BLS releases their monthly employment report on the first Friday of each month but because of the government shutdown that report will not be released till this coming Friday. The disappointing growth in the private sector shown in ADP’s report and fallout from the government shutdown in October has diminished expectations of job growth in the coming BLS report. Previous estimates of 160-180,000 job gains have shrunk to 120-140,000. The economy has been expanding yet employment gains have been moderate, a puzzlement to a lot of economic models. The stagflation of the 1970s contradicted several prominent economic models at that time and the current persistent weakness in employment growth has got to be causing some head scratching by labor economists.

The continuing computer dysfunctions at healthcare.gov have commanded the spotlight these past two weeks. There are about 15 million people, or 5% of the population, who purchase individual health insurance plans. About 50% of individual plans are not renewed each year, either by choice of the insurance company or the insured. In the industry, this is referred to as the “churn rate.”

The Affordable Health Care Act, a/k/a Obamacare, enacted minimum standards for health insurance plans. Existing plans were grandfathered in with a few caveats, one of them being that there was no change in rates since the act was signed into law in 2010. Of course, most plans have annual rate revisions, voiding any grandfathering provisions. Some estimate that as many as half of all individual policy holders have received cancellation notices from their insurance carriers.

Only 18 states have set up their own health care exchanges and these have functioned fairly well over the past month. The “hub” portion of healthcare.gov acts in the background to connect these state exchanges to data from various government agencies. A majority of states, including all states dominated by Republican legislatures, opted not to set up their own exchanges but to use the federal health care exchange at healthcare.gov. This much more visible portion of the health care IT infrastructure has been a disaster since it opened on October 1st. Many individual plan policy holders in states without an exchange must access this web site to shop for insurance policies and apply for federal insurance subsidies. For many the web site has been inaccessible or there were long delays in creating accounts on the site or they were constantly dropped off the site.

There was little to no support for Obamacare among Republicans and this dysfunctional web marketplace underscores a lack of faith in the big government that Democrats extol. Note to Democrats: a crippled web site is not the way to win friends and influence people.

In control of the House, Republicans control the agendas of the various committees and subcommittees. Note to Democrats: don’t screw up when the other party has control. In congressional hearings, Republican reps presented numerous examples of constituents angry over the largely non-functioning federal health care site. Democrats were angry as well – less so at agency officials appointed by a Democratic President and more so at Republicans, arguing for everyone to come together to solve these problems.

After failing to make their point by shutting down the government for a few weeks, House Republicans have taken a more moderate stance of letting the Democratic health care insurance apparatus implode. Had the Republicans – and Democrats – not been posturing at their podiums during the shutdown, Republicans might have paid more attention to the healthcare.gov site problems during the first week of the government shutdown and adopted this more moderate stance sooner. Note to Republicans: get out of the way when your opponent is falling on his sword.

In the political wrangling over the passage of the Affordable Care Act, President Obama famously repeated, “If you like your insurance, you can keep it.” What he should have said was “Nothing in the new health care act will force you to change plans,” but that indicates some nuance. Nuance is the first soldier to fall in political campaigns. Words are daggers; as kids we learn that lesson well. To pass the Politician Exam, candidates learn three things about the use of words: how to conceal, cajole and cut with them. In Politician School they learn “Keep It Simple, Stupid” and think that the Stupid are the voters. In sales, the quip is aimed at the salesperson, a “memo to self” reminder that the more one becomes practiced in the art of selling a particular good or service, the more complicated and less effective one’s presentation can become.

Politicians tend to talk to voters at the level of the least intelligent among them, so it comes as no surprise that President Obama kept it beguilingly simple, to the point of an almost falsehood. Yes, if an insurance company kept a policy exactly as it was three years ago, then it was grandfathered in. An insurance carrier has little incentive to keep a person or family in the same risk pool when the carrier can cancel the policy, issue them a new policy at higher rates justified by the fact that the person or family is now in an unrated risk pool. President Obama might have thought that the subject of risk pools was just too complicated for simple minded voters. Several years ago, politicians in Colorado found that voters were very interested in and could comprehend risk pools when it involved changes to auto insurance. In response to legislative changes, I have had at least two policy cancellations and reissues by my auto insurance carrier. Because the market for auto insurance is very competitive, rate changes were small. Not so in the market for individual health insurance.

My state, Colorado, has set up its own exchange. In Estes Park, a husband and wife with a family of four kids will save almost $600 a month with a health insurance plan they purchased on the exchange. Their deductible will drop from $12,500 a year to zero.

For each anecdote illustrating the benefits of Obamacare, there will be at least one example of financial hurt. For 14 years as a self-employed person I carried an individual health policy, so I am well aware of the benefits and problems of these policies. To get an initial policy, I answered a lot of questions about myself, my habits, my family’s medical history, and my family’s parent’s medical history. I peed in a cup and had blood taken to get a policy renewal. Applications are an average of 23 pages according to testimony in recent hearings. Contrast that length with the typical two page application for an employer-sponsored health care plan. In short, there were and are a lot of very big and persistent problems in the individual health insurance market.

Many individual plans are sold to small business owners or self-employed professionals, an independent lot who do like being able to pick and choose an affordable plan that meets their needs. Despite the negatives, individual plans did not suffer the onerous burden of government regulation. Media attention to the problems in individual plans has been scant because almost 90% of people with health insurance get their insurance through an employer or through Medicare or Medicaid.

A week ago, a Congressional oversight committee questioned CGI, the general contractor for the healthcare.gov web site, and OSSI, a contractor for the backbone of the system. This past week, another Congressional committee questioned Marilyn Tavenner, the head administrator for CMS, the government agency that administers Medicare and Medicaid, and Katherine Sebelius, the Secretary of HHS. Both have apologized for the fiasco and have promised a tireless effort to get it right, bringing in teams of experts from private industry, including Google and Facebook, to work on the problems.

Ms. Tavenner worked for 25 years in the big hospital chain HCA, then a four year stint in Virginia’s HHS, before becoming a Deputy Administrator, then the head Administrator at CMS. Congresspeople on both sides of the aisle gave her a lot of respect. During the hearing with Ms. Tavenner, there were several points raised. While I took notes, I did not fact check the claims.

CMS projects an enrollment of 7 million by March 2014. Of these 7 million, approximately 2.3 million need to be younger to make the policies actuarially sound.

Before the web site launch on October 1st, the CMS conducted small scale tests of the site for two weeks in September that showed no major problems. In testimony the week before, both CGI and OSSI said that a project this size requires several months of testing before launch.

CMS made the decision not to release initial application or enrollment numbers on healthcare.gov till mid-November, claiming that the numbers were unreliable. Republican members of the committee claimed that this was a delaying tactic to hide the fact that the numbers of enrollees so far is very low.

Ms. Tavenner insisted that their goal was to have the site running smoothly by the end of November, giving those who have had policies cancelled effective on Jan. 1st ample time to sign up for new plans.

If a person is not concerned about the availability of subsidies, they do not have to sign up, i.e. create an account on the web site, simply to find out what plans are available and at what rates.

Health care costs and coverage over the next twenty-five years are the primary concerns of small businesses. (Side note: for most of the 2000s, premiums in the Colorado small business market were increasing by 9 – 15% each year.)

In August, CMS decided to delay the “Shop and Browse” rollout of insurance plans for small businesses on healhcare.gov till later in the year. They also decided to delay the Spanish version of the web site as well as the capability of Medicare and Medicaid transfers. Even with the delayed implementation of some of these components of the web site, the site has been dysfunctional.

On October 24th, Mother Jones reported that it was possible that social security numbers could be hacked on the healthcare.gov web site.

Charley Rangel, a Democratic Congressman from New York, stressed the need for health care access for children, reminding Republicans that they need a stock of healthy children to fight their wars. An example of the verbal tennis match that ensues at some Congressional hearings.

Under the medical loss ratio clause of Obamacare, $3.4 billion has been returned to policyholders by insurance carriers.

17 million children with pre-existing conditions can no longer be denied coverage.

Medicare patients have saved $8.3 billion by the closing of the “donut hole” in Part D prescription drug coverage.

Lloyd Doggett, a Democratic rep from Texas (Texas has everything, including Democrats), continues to ask for Navigator progress reports. Navigators are licensed by CMS to help people sign up for Obamacare and it was not clear how much supervision CMS has over these Navigators.

Ms. Tavenner denied reports that Navigators are not required to undergo criminal background checks.

Current Medicare claims are 18% below CBO projections from a few years ago. There has been a slowing of medical costs for the past few years. If someone leans to the left, they attribute that to the enactment of the ACA. If someone leans to the right, they attribute the reduction to the recession.

I noticed a pattern during the hearings and the distinction has been confirmed in some polling. Democratic voters and their representatives focus on health care access, while Republicans focus on health care costs. This difference in focus helps explain why each side often talked past the other during the hearings.

The longer that the web site is not functioning properly, the more that voters will punish Democratic reps in the 2014 elections. Many districts are rigged – er, engineered – to be no contest for one party or the other. Democratic reps in contested districts are hoping that the current problems are fixed asap and praying that no more problems emerge before the election.

And finally, a side note on food stamps. The House reduced food stamp benefits by 5% this week. Lest you think that Republicans are all about smaller government, think again. Yahoo reported that Republicans want to impose restrictions on what foods and drinks a person can buy with food stamps. Whatever became of the Party of Personal Responsibility? Although President Obama has said he would veto the plan, it indicates that Republicans as well as Democrats are parties of Big Gummint. Put your money in the gumball machine and hope your flavor comes out.