As this past quarter began in July, Greece’s debt was a concern but the countries of the EU were in negotiations to work it out. QE2, the Federal Reserve’s program of bond buying, had just ended, prompting some to worry about a negative effect on the economy as that stimulus. Early second quarter earnings reports in mid July were strong and the balance sheets of major companies showed that they had accumulated ample reserves of cash to weather any small downturns. Manufacturing was slumping a bit but that was attributed to supply chain disruptions from the March Japanese tsunami and was expected to grow again in the third quarter. The moribund housing sector and stubbornly high unemployment remained a concern but the stock market is a pricing of future company earnings. The companies in the S&P500 which have any foreign earnings receive the majority of their earnings from countries other than the U.S. This global sales and revenue base makes these large U.S. companies less vulnerable to economic weakness in any one country.

Japan’s recovery in GDP in the second quarter surprised many, testifying to the resilience and industry of the Japanese people and Japanese industry. China, Indonesia, India and Brazil were showing strong growth, perhaps a bit too much growth, as inflation in those countries and regions was prompting central banks to take steps to cool that growth. Growth in the EU countries was a concern but German manufacturing was holding steady.

Toward the end of July, the EU reached an agreement to provide financing to Greece and, in the U.S., President Obama and House Speaker Boehner supposedly reached an agreement – dubbed the “grand bargain – for debt reduction. On July 22nd, the S&P500 closed near 1350. At the end of September, the S&P500 stood at 1130, a drop of 17%. What happened?

The weekend after the “grand bargain” came news that there was no bargain. During August, the American people stared in befuddlement at a dark comedy in which lawmakers and the President brought the country to the brink of default, prompting one rating agency to downgrade U.S. government debt.

Computing the Gross Domestic Product (GDP) of an entire nation is a complex affair, one that requires an early estimate and two revisions. In the late days of July, the Bureau of Economic Analysis (BEA) revised the GDP growth for the 1st quarter of 2011 (ending in March) from a weak 1.9% to an almost recessionary .4%. This was a large revision and shook the markets, swiftly dropping the S&P500 index to about 1100.

Germany reported strong manufacturing data for July but China showed a stalled growth in their manufacturing, adding to worries about a global slowdown. Since early August, the market has behaved like a small boat in the Mid Atlantic, rising and falling dramatically with both news and worries about Greece’s debt as well as the debt of Italy, Spain, Ireland and Portugal. Investors have fled from the stocks of banks holding the debt of those countries as well as larger banks which might have indirect exposure to that debt. An index of large banks has fallen 28% since April of this year. Many developed countries are wallowing in debt. A slowdown in growth leads to less tax revenue to pay down that debt. Worries of a global recession or a severe slowing of growth provoke fear of bank defaults, government defaults, and growing pressure on small and medium sized businesses, who are least able to withstand downturns in an economy.

Fractious meetings among EU member countries, among the various branches of the U.S. government leads many to regard politicians on both sides of Atlantic as dysfunctional, unable to resolve their ideological differences to make any functional policy decisions. Investors worry about the viability and future of the euro currency, fleeing the Euro and parking their money in U.S. Treasuries, causing the price of Treasuries to rise and the yield (interest) on those bonds to fall to historically low levels.

In September, an HSBC index of small and medium Chinese manufacturers reported a slight contraction. German manufacturing declined from strong numbers in July to a neutral stall speed in September, confirming fears of a global slowdown.

In the U.S. and Eurozone, governments at all levels have instituted austerity measures to cope with declining tax revenues. Government employee layoffs increase the demand for social support programs, prompt civilians to curb their spending, resulting in less tax revenues for government, prompting more government cuts, ad nauseum. Cautious companies hoard what cash they have, reduce their investments in anticipation of further slowdowns in consumer demand.

Weighing on the economies of the U.S, Japan and Europe are a decades long accumulation of debt. Below is a chart of OECD data on the total debt of developed countries. Debt in the U.S. doesn’t look bad compared to some of these other countries. (Click to enlarge in separate tab)

For the past thirty years, all of us in the U.S. have been running up debt. People, companies and governments at the Federal, State and local levels have borrowed…and borrowed…and borrowed some more.

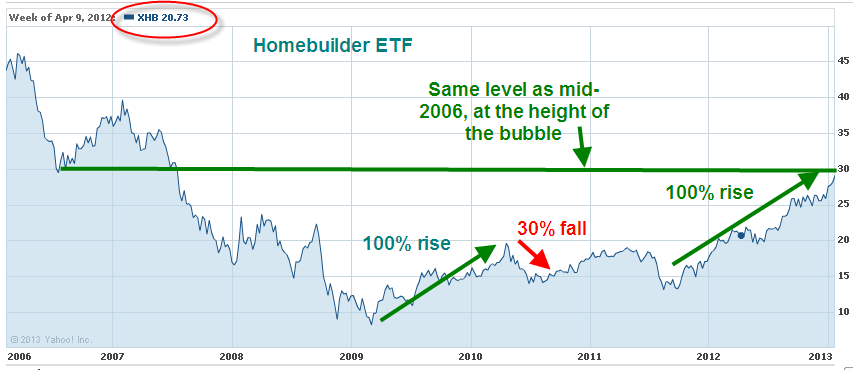

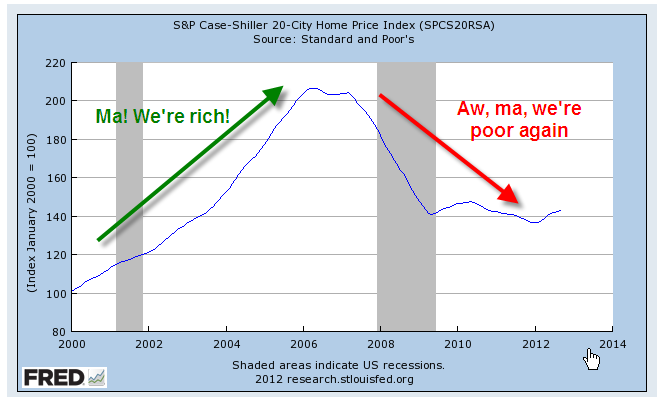

The severely slumping U.S. housing market is a strong headwind to any GDP growth. Lower valuations lead to less property taxes for local governments and schools, reduced government services, houses that are difficult for homeowners to sell without bringing cash to the sale. A recent report by the Commerce Dept. showed that housing has contributed an average of 4.7% to GDP for the past half century. Last year, housing contributed only 2.2% to GDP. If the health of the housing sector was just average, GDP growth in this country would be 2.5% higher. Some in the industry anticipate that it will be another five years for housing to recover from the excesses of the past decade.