January 27th, 2013

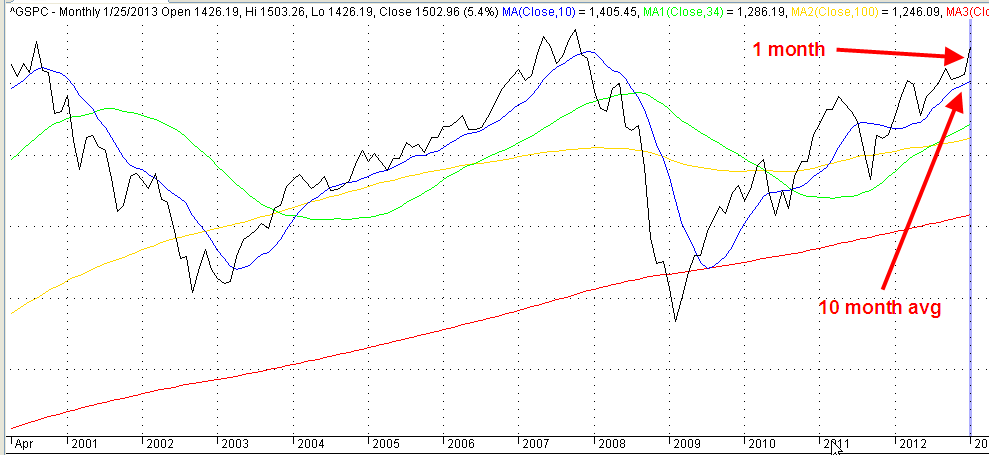

This past week, Republicans in the House passed a bill to delay the raising of the debt ceiling till May. The S&P500 crossed 1500, nearing the high of 1550 it set in October 2007. This past week, money flowing into equity mutual funds finally surpassed the flows into bond funds (Lipper Source)

As the saying goes, “The trend is your friend.” When the current month of the SP500 index is above the ten month average, it’s a good idea to stay in the market.

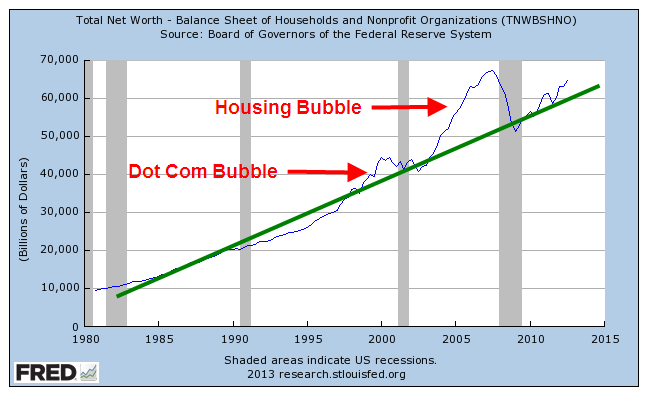

So, happy days are here again! Well, not quite. Household net worth is still climbing but has not reached the 2007 peak.

But when we step back and look at the past thirty years, household net worth is better than trend.

Asset bubbles overly inflate and deflate net worth, which includes the valuation of assets like stocks and homes. An asset bubble is like a Ponzi scheme in that those who get in toward the end, before the bubble bursts, often suffer the worst.

CredAbility, a non-profit credit counseling service, produces a Consumer Distress score that evaluates five categories that have a significant effect on a consumer’s financial stability: employment, housing, credit, the household budget and Net Worth. It has only just broken out of the unstable range into the bottom of the frail range.

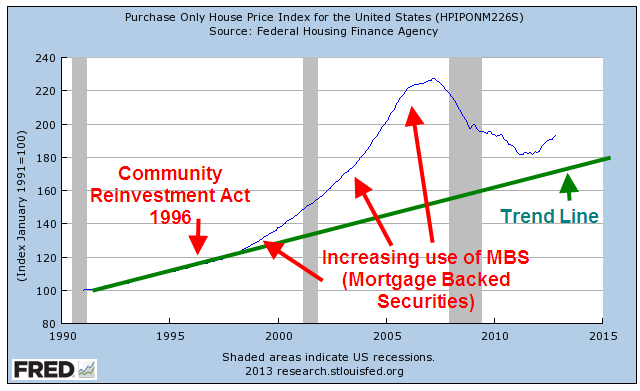

The Federal Housing Finance Administration (FHFA) released their House Price index a few days ago. This price gauge is indexed so that 1991 prices equal $100. The index, which does not include refinancing, came in at $193, or just about 3% per year. Although housing prices are still depressed from the heights of the housing bubble they are still above the CPI inflation index since 1991. Housing prices generally rise about 3% – 4% per year, depending on what part of the country you live.

When we look back twenty years, we can see that housing prices are, in fact, above a sustainable trend line established before the Community Reinvestment Act and the advent of mortgage securitization, both of which undermined rational underwriting standards.

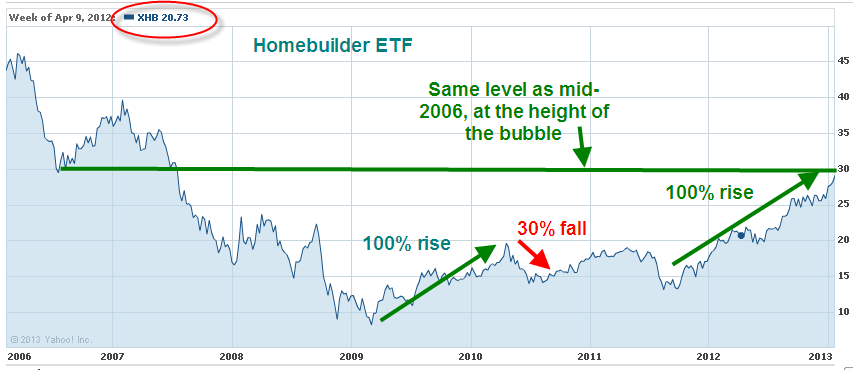

Nationally, we are close to sustainable price trend but still a bit inside the bubble. Sensing that home prices may have hit bottom, Home Builder stocks as a group are up about 50% in the past year. Think that’s good? They rose almost 100% from the spring of 2009 to the spring of 2010, only to fall back again.

Tight credit, rigid underwriting standards and a still frail consumer will present challenges to the housing market as it climbs slowly out of the doldrums of the past few years.