The dollar is the world’s reserve currency and its strength – its price relative to other currencies – is straining both the economies and the financial expectations of other countries. Businesses in developing countries with an unreliable currency regime often have to borrow in dollars – what is called “dollar denominated debt.” Businesses must make their loan payments in dollars so they must trade in ever more of their local currency to get the dollars to make the payment. European nations stocking up on liquified natural gas (LNG) from the U.S. are feeling the pinch as well. Why is the dollar strengthening?

In international finance there are two equations that model the relationship between expected inflation, exchange rates and interest rates. Currency traders are expecting inflation to moderate more quickly in the U.S. than in other countries. Because the U.S. has a better supply of natural gas, its energy prices will be less affected by the war in Ukraine. Secondly, the Fed has been increasing interest rates, enticing investors in other countries to invest their money in U.S. debt. The dollar-euro exchange rate has not been this low since 1999 when the Eurozone countries began using a common currency, the euro.

When the dollar gets stronger, exports decrease because American goods are more expensive to buyers in foreign countries. Imports become cheaper so Americans buy more stuff from other countries. However, if the U.S. is sliding into a recession, Americans are less likely to buy enough European imports to offset the LNG that European countries will buy from the U.S. This will increase the demand for dollars relative to the euro, further driving up the price of dollars in other currencies.

The dollar has been strengthening against other forms of currency like gold and digital exchange mechanisms like Bitcoin. Priced in dollars, gold has lost about 16% of its value in the past six months. Bitcoin has lost 60% since March. Gold is both a commodity and a currency. Gold holds a store of work that it can do in the future. It has cosmetic and industrial uses.

Bitcoin is the product of past work only – a “proof of work” done in the past. It stores no capability of future work. It takes a lot of electricity and computing power to mine Bitcoin but it cannot store electricity for future use. If it could do so, the price of Bitcoin would go up when electricity prices went up.

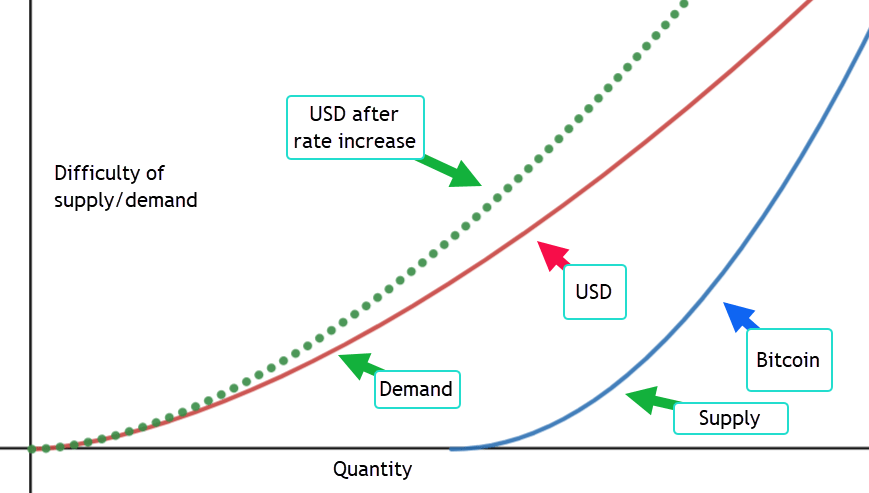

In the graph below I’ve illustrated a key difference between the dollar and Bitcoin. On the right is Bitcoin. Its algorithm incorporates a “diseconomies of scale.” As more Bitcoin is mined, it takes more effort to mine Bitcoin. Bitcoin focuses on the difficulty of supply.

On the left is the fiat dollar. There is no difficulty in supplying it. The Fed focuses on the demand for the dollar by adjusting the interest rate, the bend in the curve. It is currently tightening that bend – the dotted green curve – and increasing the difficulty of getting more dollars. The dollar can respond to changing demand more easily than gold or Bitcoin because it targets demand.

Like Bitcoin, the dollar stores no future work. In an article earlier this year (2022), I wrote that America’s store of wealth was both a proof-of-work, proof-of-stability and proof-of-trust. The dollar itself is only a sign of trust in American institutions. The checks and balances of our system of government ensures that most policymaking is incremental. While that frustrates Americans, the relative predictability of U.S. policy is reassuring to foreign investors. Americans often run around like crazy monkeys on the deck of a cruise boat but the ship is unlikely to make a large course correction.

Think of the bend in the curve as a toll for using the highway to the future. Bitcoin’s curve is rigid. The toll remains the same. Bitcoin enthusiasts would maintain that this rigidity should shift the curve to the right over time, increasing the buying power supplied by Bitcoin.

Let’s look at three approaches. 1) Bitcoin limits the length of highway that will be built. Enthusiasts claim that this will make each “mile” of the bitcoin highway more valuable.

2) MMT advocates offer a different solution. As long as there are resources – both labor and material – available, build more highway. By targeting the supply available, congestion will ease.

3) The Fed offers an approach that targets demand, not supply. The Fed raises and lowers the interest rate – the toll – to get onto the highway to the future. Raising interest rates is a form of congestion pricing. High inflation means that there are too many people using the available length of highway. The Fed has promised that it will keep raising the toll until fewer people are using the highway. As demand declines, some of those working on the highway may lose their jobs. Unemployment will increase but historically it is very low.

The strength of the dollar against other currencies, including Bitcoin and gold, indicates increasing demand for the Fed’s approach. What is the morality of an international floating rate regime where businesses in a developing country have to work even harder to pay their dollar-denominated loans? Bitcoin advocates claim that global adoption of Bitcoin will make a more even playing field, reducing the advantage that developed countries have over developing countries. That can be the subject of another article.

Over a century ago, the passage of the 16th Amendment allowed the federal government to tax earnings from labor, giving the central government entry into the lives of every American. Fifty years earlier, Congress had passed an income tax to pay the debts incurred during the Civil War. In 1895, the Supreme Court ruled that taxes on income were a direct tax that must be apportioned in accordance with Article 1, Section 8 of the Constitution. The 16th Amendment bypassed that uniformity requirement to tax incomes at different rates. The target of the income tax was the top 1% but within two decades the tax affected low and middle income groups. The stated goal of current income taxation is income distribution and a leveling of outcomes. A century after the passage of the income tax, income distribution has reached record levels of inequality (FED, 2021). As a leveling device, the income tax has failed.

As tax rates on income increase, incentives to evade the tax rise. Those with the highest rates lobby to have their income excluded or be taxed as a special class. As advocates of Modern Monetary Theory point out, a sovereign nation that issues its own currency does not need tax revenues to fund itself at the margin. Taxes act as a restraint on the purchasing power of private parties and the spending priorities of government. Because income taxes are not levied uniformly, they are especially subject to corruption and political influence by those most damaged by the tax. Billionaire investor Warren Buffett has noted that he pays a lower tax rate than his secretary. A tax law meant to curb inequality thus promotes inequality under the law.

Bitcoin* promised anonymous transactions between people at a low cost. It’s anonymity promoted the principle of uniformity, treating large and small transfers equally. The principle of peer-to-peer exchange without government oversight, taxes or exchange fees recalls an earlier time in our history when there was a quasi-boundary between society and the federal government. Society is built on agreement. The foundation of government is forced compliance with the law. An example is our courts and police forces. Political economy is the marriage of these two institutions, force and agreement. Economics is the study of exchange in the search to satisfy our needs. Politics is the study of the division of rights and power. Needs and rights must ever be in conflict.

In conventional exchange, rights are recognized and protected by a government body. Enforcement involves sanctioned force that is concentrated in a small proportion of our society and that concentration of power makes government subject to corruption. The deluge of lobbyists on Capitol Hill is a testament to the dominant power of the federal government. Bitcoin distributes the recognition of rights across a vast public ledger but it lacks an enforcement mechanism to protect those rights. Bitcoin’s principle of distributed consensus offers the promise that the sanctioning of force could be more equitably distributed among majority and minority groups in our society.

Minority groups are often victimized by selective policing that keeps them penned into socio-economic spaces on the fringes of political power. An unpaid parking ticket rapidly accumulates interest and late fees, then becomes a bench warrant and makes someone subject to arrest. The owner of a delivery truck fleet in New York City with multiple double parking violations is rarely arrested. Institutions of enforcement were designed by the majority for the benefit of the majority.

Fear of the police and those institutions is felt deep within everyone in a minority neighborhood. Power tends to concentrate and leads inevitably to autocracy. A distributed ledger principle acts as a curb on that tendency. A community with digital control of police weapons might be able to disable the weapons of an abusive officer, forcing that officer onto desk duty or patrolling parking meters while an incident is investigated. What is science fiction today becomes science fact tomorrow. Fifty years ago a flip phone communicator like the one used on Star Trek was a figment of an author’s imagination. The public ledger technology that forms the foundation of Bitcoin exchange is still in its infancy but it is a vison of distributed community constraint as opposed to the autocratic constraints imposed by government.

In principle, the law is meant to be a uniform constraint. In practice, the law is a constraint warped by those with the money to buy influence and political power. Those who currently have power fight hard to keep it. If public ledger technology could be adapted to a community constraint on the use of force, those with resources would likely develop a way to modify that constraint for their own benefit. Should society abandon the pursuit of a distributed community constraint? No. The internet is younger than the oldest millennial and is pockmarked with scams and illegal activities but the benefits outweigh the dangers. Even if Bitcoin remains a private currency with limited adoption, its technology and principles point to a better world.

Two quick asides before I get into this week’s topic. A cricket perched on the top of a 7′ fence. It drew up to the edge of the top rail, learned forward, raised its rear legs as though to jump, then settled back. It did this twice more before jumping 8′ out then down into a soft landing on some ground cover. How far can crickets see, how often do they injure a leg if they land incorrectly and do they get afraid?

The bulk of the personal savings in this country is held by the top 20% of incomes, and it is this income group that received the lion’s share of the 2017 tax cuts. It’s OK to bash the rich but that top 20% probably includes our doctor and dentist. Before you start drilling or cutting me, I want to make it perfectly clear that I was not criticizing you, Doc.

In 2016, the top quintile – the top 20% – earned 2/3rds of the interest and dividend income (Note #1). Due to falling interest rates over the past three decades, real interest and dividend income has not changed. Real capital has doubled and yes, much of it went to those at the top, but the income from that capital has not changed. That is a huge cost – a hidden tax that gets little press. The real value of the public debt of the Federal Government has quadrupled since 1990, but it pays only 20% more in real interest than it did in 1990 (Note #2). Here’s a graph of personal interest and dividend income adjusted to constant 2012 dollars. Thirty years of flat.

Ok, now on to a story. Economists build mathematical models of an economy. I wanted to construct a story that builds an economy that gradually grows in complexity and maybe it would help clarify the relationships of money, institutions and people.

Let’s imagine a group of people who move into an isolated mining town abandoned several years earlier. The houses and infrastructure need some repairs but are serviceable and the community will be self-sufficient for now. The homeowners form an association to coordinate common needs.

The association needs to hire lawn, maintenance and bookkeeping services, and security guards to police the area and keep the owners safe. How does the association pay for the services? They assess each homeowner a monthly fee based on the size of the home. How do the homeowners pay the monthly fee? Each homeowner does some of the services needed. Some clean out the gutters, others fix the plumbing, some keep the books and some patrol the area at night. They work off the monthly fee.

How do they keep track of how much each homeowner has worked? The association keeps a ledger that records each owner’s fee and the amount worked off. The residents sometimes trade among themselves, but it is rare because barter requires a coincidence of wants, as economists call it. Mary, an owner, needs some wood for a project and Jack has some extra wood. They could trade but Mary doesn’t have anything that Jack wants. He tells Mary to go down to the association office and take some of her time worked off her ledger and credit it to Jack’s monthly fee. Mary does this and they are both happy (Note #3).

As other owners learn of this idea and start trading work credits, the association realizes it needs a new system. It prints little pieces of paper as a substitute for work credits and hands them out to owners who perform services for the association. These pieces of paper are called Money (Note #4).

The

money represents the association’s accounts receivable, the fees owed and

accruing to the association, and the pay that the association owes the owners

for the work they have done. Then the association notices that there are some

owners who are not doing as well as others. It assesses an extra fee each month

from those with larger homes and gives that money to needy homeowners. These are called transfers because the owners

who receive the money do not trade any real goods or services to the association.

In this case the association acts as a broker between two people. Let’s call

these passive transfers. We can lump these transfers together with exchanges of

goods and services.

Then

some people from outside the area start stealing stuff from the homeowners. The

association needs to hire more security guards, but homeowners don’t want to

pay a special one-time assessment to pay for the extra guards.

Instead

of printing more Money, the association prints pieces of paper called Debt.

Homeowners who have saved some of their money can trade it in for Debt and the

association will pay them interest. Homeowners like that idea because Money

earns no interest and Debt does. The association uses the Money to pay for the

extra security guards.

But

there are not enough people who want to trade in their Money for Debt, so the

association prints more Money to pay the extra security guards.

Let’s pause our story here to reflect on what the words inflation and deflation mean. Inflation is an increase in overall prices in an economy; deflation is a decrease (Note #5). Inflation occurs when the supply of money fuels a demand for goods and services that is greater than the supply of goods and services. Ok, back to our story.

So

far so good. All the Money that the association has printed equals a trade or a

passive transfer. Let’s say that the association needs more security guards and

no one else wants to work as a security guard because they can make more Money

doing jobs for other homeowners. The association makes a rule called a Draft.

Homeowners of a certain age and sex who do not want to work as security guards

will be locked up in the storage room of the community center.

Now

there’s a problem. Because the association has taken some homeowners out of the

customary work force, those people are not available for doing jobs for other

homeowners, who must pay more to contract services. This is one of several

paths that leads to inflation. To combat that, the association sets price

controls and limits the goods that homeowners can purchase. After a while, the

outsiders are driven off and the size of the security force returns to its

former levels.

Now all the extra Money that the association printed to pay for the security force has to be destroyed. As homeowners pay their dues, the association retires some of the money and shrinks the Money supply. However, there is a time lag, and prices rise sharply (Note #6).

Over

the ensuing decades, there are other emergencies – flooding after several days

of rain, a sinkhole that formed under one of the roadways, and a sewer system

that needed to be dug up and replaced. The association printed more Debt to cover

some of the costs, but it had to print more Money to pay for the balance of

repairs. Because the rise in the supply of Money was a trade for goods and

services, inflation remained tame.

There

didn’t seem to be any negatives to printing more Money, so the homeowners

passed a resolution requiring that the association print and pay Money to

homeowners who were down on their luck. These were active transfers – payments

to homeowners without a trade in goods and services and without some offsetting

payment by the other homeowners.

So

far in our story we have several elements that correspond with the real world: currency,

taxes, social insurance, the creation of money and debt and the need to pay for

defense and catastrophic events. Let’s continue the story.

With

the newly printed Money, those poorer homeowners could now buy more goods and

services. The increased demand caused prices to rise and all the homeowners

began to complain. Realizing their mistake, they voted on an austerity program

of higher homeowner fees and lower active transfers to poorer homeowners.

Because

homeowners had to pay higher fees, they didn’t have enough extra Money to hire

other services. Some residents approached the association and offered to repair

fences and other maintenance jobs, but the association said no; it was on an

austerity program and cutting expenses. Some residents simply couldn’t pay

their fees and the problem grew. The association now found that it received

less Money than before the higher fees and Austerity program. It cut expenses

even more, but this only aggravated the problem.

Finally,

the association ended their Austerity program. They printed more Money and hired

homeowners to make repairs. Several homeowners came up with a different idea.

There is another housing development called the Forners a few miles away. They

are poorer and produce some goods for a lower price. The homeowners can buy

stuff from the Forners and save money. There are three advantages to this

program:

Things bought from the Forners are

cheaper.

Because the homeowners will not be

using local resources, there will be less upward pressure on prices.

The homeowners will pay the

association for the goods bought from the Forners and the association will pay

the Forners community with Debt, not Money. Since it is the creation of Money that

led to higher prices, this arrangement will help keep inflation stable.

As

the homeowners buy more and more stuff from the Forners, the money supply

remains stable or decreases. After several years, homeowners are buying too

much stuff from the Forners and there is less work available in the community.

As homeowners cannot find work, they again fall behind in paying their monthly

fees.

Several

of those in the association realize that they don’t have enough Money to go

around in the community. There is a lot to do, and the homeowners draw up a

wish list: repairs to the roads and helping older homeowners with shopping or

repairs around their home are suggested first. A person who is out of work

offers to lead tours and explain the biology of trees for schoolchildren. The

common lot near the clubhouse could use some flowers, another homeowner

suggests. I could use a babysitter more often, one suggests, and everyone nods

in agreement. I could teach a personal finance class, a homeowner offers.

Another offers to read to homeowners with bad eyesight and be a walking

companion to those who want to get more exercise.

Everyone who contributes to the welfare of the community gets paid with Money that is created by the association. What should we call the program? One person suggests “The Paid Volunteer Program,” and some people like that. Another suggests, “The Job Guarantee Program” and everyone likes that name so that’s what they called it (Note #7).

So

far in this story we have two key elements of an organized society:

Money – a paper currency created by the

homeowner association.

Debt – the amount the association owes

to homeowners (domestic) and the Forners (international).

Next

week I hope to continue this story with a transition to a digital currency, banks

and loans.

//////////////////////

Notes:

In 2016, the top 20% of incomes with more than $200K in income, earned more than 2/3rds of the total interest and dividends. IRS data, Table 1.4

In 2018 dollars, the publicly held debt of the Federal government was $4 trillion in 1990, and $16 trillion now. In 2018 dollars, interest expense was $500B in 1990, and is $600B now.

In David Graeber’s Debt: The First 5000 Years, there is no record of any early societies that had a barter system. They had a ledger or money system from the start.

In the Wealth of Nations, Adam Smith – the “father” of economics – defined money as that which has no other value than to be exchanged for a good. This essential characteristic makes money unique and differentiates paper money from other mediums of exchange like gold and silver.

An easy memory trick to distinguish inflation from deflation. INflation = Increase in prices. DEflation = DEcrease.

The account of the increased force of security guards – and its effect on prices and regulations – is the simple story of money and inflation during WW2 and the years immediately following. The process of rebalancing the money supply by the central bank is difficult. Monetary policy during the 1950s was a chief contributor to four recessions in less than 15 years following the war.

A Job Guarantee program is a key aspect of Modern Monetary Theory.

This week I had a chance to watch two documentaries hosted by journalist Bill Moyers several years ago (Note #1). They featured the shifting fortunes of two blue-collar working-class families in Milwaukee. Each family had enjoyed the security and benefits of middle-class life – a house and dreams that they would send their kids to college one day. When each breadwinner lost their jobs in the manufacturing industry, they realized just how precarious their situation was.

With more education and skills, these blue-collar workers could have made a better transition. Higher education is certainly a solution for some but how will more education help the butcher, the baker and the candlestick maker? These professions play a part in our complex society and the marketplace has not found a viable solution for those workers and their families.

What is the middle class? The Census

Bureau defines it as the middle three quintiles of income (Note #2). What does

that mean? If incomes range from $0 to $100 the range of the middle class is

from $20 to $80. Some economists use $25 and $75 as the upper and lower bounds

of the middle class. A hundred years ago the middle class was a small sliver of

the population in the middle. They were between the working class who relied

almost entirely, if not exclusively, on work for their income, and the upper

class whose major source of income was not work – profits, interest, dividends

and rents.

When economists talk about the

middle class, it is usually the lower middle-class or working class that they

use to represent the fortunes of a wide range of people with far different

circumstances, education and skills. Both videos focused on that working-class

segment because the stories are poignant and the solutions difficult, if not

intractable.

The Golden Age of the working class

was after World War II when unions were strong and blue-collar incomes grew much

faster than inflation. After the productive capacity of much of developed world

had been destroyed during World War II, America was the factory for the world.

The workers in those factories enjoyed strong bargaining power and could

command a good benefit package and wage gains from employers.

Until the Roosevelt administration established housing and mortgage programs during the decade of the Great Depression, most families had to put a third to a half down on a house and pay off the mortgage in five to ten years. The FHA (1934) and FNMA (1938) lowered those requirements to as low as 10% (Note #3). The GI bill that was passed in 1944 promised returning GIs a home for little to nothing down and low-interest long-term mortgages. Residential construction boomed.

As the European nations and Japan recovered

in the 1960s and 70s American firms were challenged by low cost imported goods.

As their pricing power eroded, they became more resistant to wage and benefit

demands by working-class unions. Protectionist policies guarded against competition

from foreign auto makers, but consumer buying power in America was a magnet for

appliances and electronics from Japan and Germany, and foodstuffs from France,

Spain, Italy and Mexico (Note #4).

The 1970s was beset by a series of bitter strikes in both private industry and in government service. The benefit and wage packages that union workers had negotiated in the 50s and 60s proved uncompetitive in the revived private international marketplace. Those who could afford the higher taxes to pay city workers began to move out of the cities to the suburbs. Cities like New York suffered under successive waves of strikes by fire, police, sanitation and transportation workers. If the firefighters got a 4% raise, other city workers wanted a similar wage package.

Rather than invest in refurbishing decades-old factories, manufacturers built new factories abroad, where labor costs were much cheaper. The savings more than offset the shipping costs of finished products back to America. Those shipping costs had been drastically reduced in 1955 when a transport owner and an engineer designed a shipping container that could be stacked and survive the rigors of an ocean voyage. They gave away the patent and the world adopted the new containers (Note #5).

As the manufacturing plants in the

northern states, particularly the Rust Belt, began to shutter their doors, some

families moved. Many families who had bought homes now found that the value of

their homes had depreciated. Some with strong ties to the community and a

lack of savings struggled on at lower paying jobs. Some lost their houses,

their cars, their dreams. The two families that Bill Moyers interviewed

exemplified this broad trend.

For some journalists and economists,

this short-lived post-War era became a benchmark for the way it should be. That

benchmark may have been a historical anomaly, an aftermath of a global war.

What is to be done? Since the Johnson Administration ushered in the War on Poverty fifty years ago, the percentage of the population in poverty has not changed (Note #2). 42% of children born into poverty remain in poverty. Either the programs have been poorly designed, or the problems are complex and resist solutions.

Will raising taxes on the rich help? Most of the capital gains go to the upper class who pay lower taxes on those gains. Is that the solution? To fund their retirement, millions of seniors each year are selling some of their IRAs and 401Ks, and incurring capital gains when they do so. Will politicians change the rules in midstream on a generation of Boomers? Old people vote in high percentages. Probably not.

Some suggest that the government stop subsidizing rich

people and give that money to people who need it. This would include means

testing Social Security, but also include a plethora of “gimmes” that

pass unnoticed to most of us from government to those who are well-off. Some

farmers receive a check from the government to not grow crops in order to

control the supply. “Dear Santa, do not give me money this year.” Who

is going to write that note?

Some have suggested we implement a Universal Basic

Income (UBI) program, a program which would give $1000, for example, to

everyone. That would be a nice subsidy for Walmart and McDonald’s who could then

pay their workers even less than they do now. Some economists argue that there

are even more problems (Note #6).

What about a higher Federal minimum wage? $15 is a

popular suggestion on the campaign trail. A $15 wage in Los Angeles has much

less buying power than it does in Alamosa, CO. Why not implement something

indexed to the median wage in each area? The BLS, the same agency that produces

the employment report each month, has the data to implement such an idea. Why a

one size fits all minimum wage? Those who prefer local solutions are not without

compassion.

History tells us that large government solutions can exacerbate the very problems they were meant to solve. The housing assistance and student loan programs are examples of the bureaucratic bramble that characterizes active Federal programs. Given that caveat, I do think that a Job Guarantee program that operated at the state and local level but was funded by the Federal government would provide stability to the more vulnerable in our work force. It would reduce the cyclical and structural unemployment that corrodes our society (Note #7). There are several proposals to implement some trial programs in the states and I support those efforts. What do you think?

In 1971 former President Nixon announced that the U.S. was abandoning the gold standard of fixed exchange that had existed for almost thirty years. Within a short time, other leading nations followed suit. Each nation’s currency simply traded against each other on a global currency, or FX, market.

Since oil was priced in dollars and the world ran on oil, the U.S. dollar became the world’s reserve currency. Each second of every day, millions of US dollars are traded on the international FX markets. The demand for US dollars is strong because we are a productive economy. The euro, yen and British pound are secondary currency benchmarks.

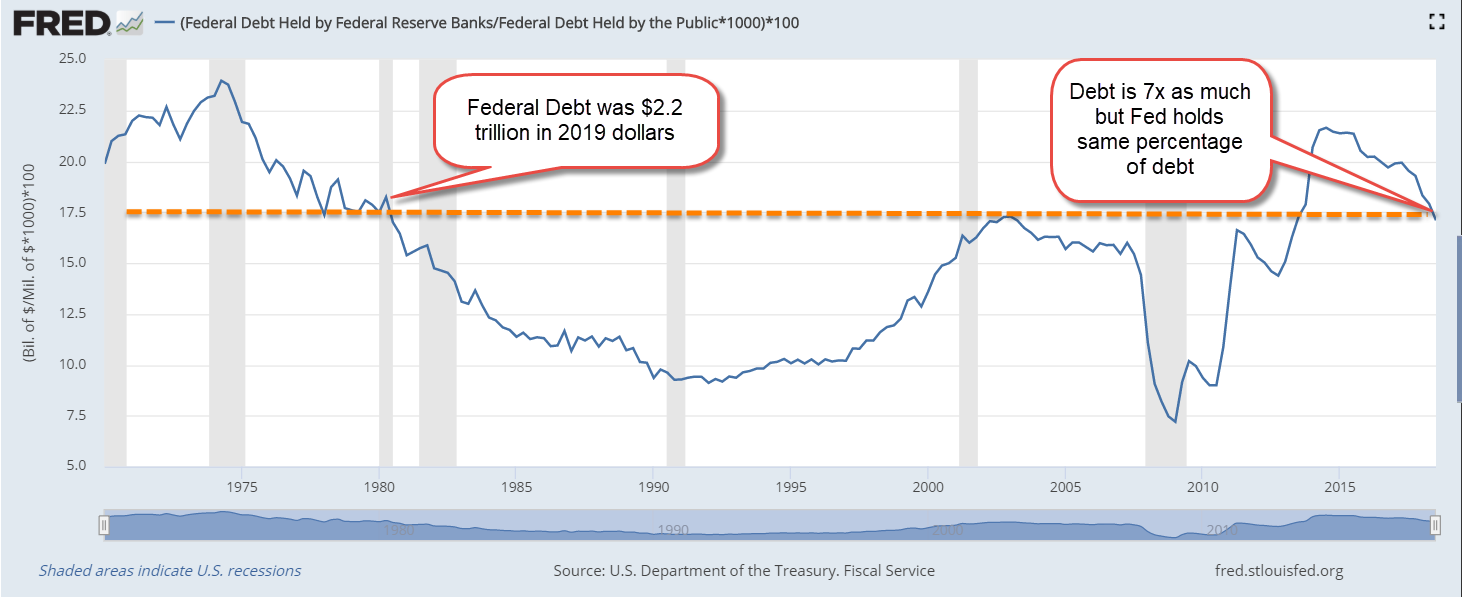

When the U.S. wants to borrow money from the rest of the world, the U.S. Treasury sells notes and bills collectively called “Treasuries” to large domestic and foreign banks who “park” them in their savings accounts at the Federal Reserve (Fed), the U.S. central bank (Note #1). The phrase “printing money” refers to a process where the Federal Reserve, an independent branch of the Federal Government, buys Treasury debt on the secondary market. It may surprise many to learn that the Fed owns the same percentage of U.S. debt as it did in 1980. The debt in real dollars has grown seven times, but the percentage held by the Fed is the same. That is a powerful testament to the global hunger for U.S. debt. Here’s the chart from the Fed’s FRED database.

In 1835, President Andrew Jackson paid off the Federal debt, the one and only time the debt has been erased. It left the country’s banking system in such a weak state that subsequent events caused a panic and recession that lasted for almost a decade (Note #2). Government debt is the private economy’s asset. Paying down that debt reduces those assets.

About a third of the debt of the U.S. is traded around the world like gold. It is better than gold because it pays interest and there are no storage costs. Foreign businesses who borrow in dollars must be careful, however. They suffer when their local currency depreciates against the dollar. They must earn even greater profits to convert their local currency to dollars to make payments on those dollar-denominated loans.

Each auction of Treasury debt is oversubscribed. There isn’t enough debt to meet demand. In a world of uncertainty, the U.S. government has a long history of respect for its monetary obligations. As the reserve currency of the world, the U.S. government can spend at will. Even if there were no longer a line of domestic and foreign buyers for Treasuries, the Federal Reserve could “purchase” the Treasuries, i.e. print money. Let’s look at the difference between borrowing from the private sector and printing money.

When the private sector buys Treasuries, it is effectively trading in old capital that cannot be put to more productive use. That old capital represents the exchange of real goods at some time in the past. In contrast, when the government spends by buying its own debt, i.e. printing money, it is using up the current production of the private sector. This puts upward pressure on prices. Let’s look at a recent example.

Quantitative Easing (QE) was a Fed euphemism for printing money. During the three phases of QE that began in 2009, the Fed bought Treasury debt. That was an inflationary policy that countered price deflation as a result of the Financial Crisis. In August 2009, inflation sank as low as -.8% (Note #3). It was even worse, but inflation measures do not include the dividend yield on money. To many households, inflation felt like -2% (Note #4). The Fed’s first round of QE did provide a jolt that helped drive prices up by 3% and out of the deflationary zone.

During the five years of QE programs, the Fed continued to fight itself. The QE programs pushed prices upwards. Near zero interest rates produced a deflationary counterbalance to the inflationary pressures of printing money. Because inflation measures do not include the yield on money, the Fed could not read the true change in the prices of real goods in the private sector. The economy continues to fall below the Fed’s goal of 2% inflation. There are still too many idle resources.

Leading proponents of Modern Monetary Theory (MMT) remind people that yes, the U.S. can spend at will, but that it must base its borrowing on policy rules to avoid inflation. A key component of MMT is a Job Guarantee (JG) program ensuring employment to anyone who wants a job. A JG program may remind some of the WPA work programs during the Great Depression. Visitors to popular tourist attractions, from Yellowstone Park in Wyoming to Carlsbad Caverns in New Mexico, use facilities built by WPA work crews. Today’s JG program would be quite different. It would be locally administered and targeted toward smaller public works so that the program was flexible.

The U.S. government has borrowed freely to go to war and has never paid that debt back. Proponents of MMT recommend that the U.S. do the same during those times when the private economy cannot support full employment. That policy goal was given to the Fed in the 1970s, but it has never been able to meet the task of full employment through crude monetary tools. With an active program of full employment, the Fed would be left with only one goal – guarding against inflation.

There are two approaches to inflation control: monetary and fiscal. Monetary policy is controlled by the Fed and includes the setting of interest rates. If the Fed’s mandate was reduced to fighting inflation, it could more readily adopt the Taylor rule to set interest rates (Note #4).

Fiscal policy is controlled by Congress. Because taxation drains spending power from the economy, it has a powerful control on inflation. However, changes in tax policy are difficult to implement because taxes arouse passions. We are familiar with the arguments because they are repeated so often. Everyone should pay their “fair share,” whatever that is. Some want a flat tax like a head tax that cities like Denver have enacted. Others want a flat tax rate like some states tax incomes. Others want even more progressive income taxes so that the rich pay more and the middle class pay less. Some claim that income taxes are a government invasion of private property rights.

Because tax changes are difficult to enact, Congress would be slow to respond to changes in inflation. The Fed’s control of interest rates is the more responsive instrument. The JG program would provide stability to the economy and reduce the need for corrective monetary action by the Fed. The program would help uplift those in marginal communities and provide much needed assistance to cities and towns which had to delay public works projects and infrastructure repair because of the Financial Crisis. As sidewalks and streets get fixed and graffiti cleaned, those who live in those areas will take more pride in their town, in their communities, in their families and themselves. This makes not just good economic sense but good spiritual sense. We can start small, but we must start.

//////////////////////// Notes:

1. Twenty to twenty-five times each month, the Treasury auctions U.S. government debt. Many refer to the various forms of bills and notes as “treasuries.” A page on the debt

2. The Panic of 1837

3. The Federal Reserve’s preferred measure of inflation is the Personal Consumption Expenditure Index, PCEPI series.

4. The annual change in the 10-Year Constant Maturity Treasury fell below -1% at the start of the recession in December 2007 and remained below -1% until July 2009. FRED series DGS10. John Maynard Keynes had recommended the inclusion of money’s yield in any index of consumer demand. In his seminal work Foundations of Economic Analysis (1947), economist Paul Samuelson discussed the issue but discarded it (p. 164-5). Later economists did the same.

5. The Taylor rule utility at the Atlanta Federal Reserve.

Modern Monetary Theory (MMT) helps us understand the funding flows between a sovereign government and a nation’s economy. I’ve included some resources in the notes below (Note #1). This analysis focuses on the private sector to help readers put the federal debt in perspective. In short, some annual deficits are to be expected as the cost of running a nation.

What is money? It is a collection of government IOUs that represent the exchange of real assets, either now or in the past. Wealth is either real assets or the accumulation of IOUs, i.e. the past exchanges of real assets. When a sovereign government – I’ll call it SovGov, the ‘o’ pronounced like the ‘o’ in love – borrows from the private sector, it entices the holders of IOUs to give up their wealth in exchange for an annuity, i.e. a portion of their wealth returned to them with a small amount of interest. A loan is the temporal transfer of real assets from the past to the present and future. This is one way that SovGovs reabsorb IOUs out of the private economy. In effect, they distribute the historical exchange of real assets into the present.

What is a government purchase? When a SovGov buys a widget from the ABC company, it also borrows wealth, a real asset that was produced in the past, even if that good was produced only yesterday. The SovGov never pays back the loan. It issues money, an IOU, to the ABC company who then uses that IOU to pay employees and buy other goods. A SovGov pays back its IOUs with more IOUs. That is an important point. In capitalist economies, a SovGov exchanges real goods for an IOU only when the government acts like a private party, i.e. an entrance fee to a national park. Real goods are produced by the private economy and loaned to the SovGov.

What is inflation? When an economy does not produce enough real goods to match the money it loans to the SovGov, inflation results. Imagine an economy that builds ten chairs, a representation of real goods. If a SovGov pays for ten people to sit in those ten chairs, the economy stays in equilibrium. When a SovGov pays for eleven people to sit in those ten chairs, and the economy does not have enough unemployed carpenters or wood to build an eleventh chair, then a game of musical chairs begins. In the competition for chairs, the IOUs that the private economy holds lose value. Inflation is a game of musical chairs, i.e. too much money competing for too few real resources.

A key component of MMT framework is a Job Guarantee program, ensuring that there are not eleven people competing for ten jobs (Note #2). Labor is a real resource. When the private economy cannot provide full employment, the SovGov offers a job to anyone wanting one. By fully utilizing labor capacity, the SovGov keeps inflation in check. The idea that the government should fill any employment slack was developed and promoted by economist John Maynard Keynes in his 1936 book The General Theory of Employment, Money and Interest.

The first way a SovGov vacuums up past IOUs is by borrowing, i.e. issuing new IOUs. I discussed this earlier. A SovGov also reduces the number of IOUs outstanding through taxation, by which the private sector returns most of those IOUs to the SovGov.

Let’s compare these two methods of reducing IOUs. In Chapter 3 of The Wealth of Nations, Adam Smith wrote that government borrowing “destroys more old capital … and hinders less the accumulation or acquisition of new capital” (Note #3). Borrowing draws from the pool of past IOUs; taxation draws more from the current year’s stock of IOUs. Further, Smith noted that there is a social welfare component to government borrowing. By drawing from stocks of old capital it allows current producers to repair the inequalities and waste that allowed those holders of old capital to accumulate wealth. He wrote, “Under the system of funding [government borrowing], the frugality and industry of private people can more easily repair the breaches which the waste and extravagance of government may occasionally make in the general capital of the society.”

Borrowing draws IOUs from past production, while taxation vacuums up IOUs from current production. Since World War 2, the private sector has returned almost $96 in taxes for every $100 of federal IOUs. Since January 1947, the private sector has loaned the federal government $371 trillion dollars of real goods, the total of federal expenditures (Note #4). What does the federal government still owe out of that $371 trillion? $15.5 trillion, or 4.17% (Note #5). If the private sector were indeed a commercial bank, it would expect operating expenses of 3%, or $11.1 trillion (Note #6). What real assets does the private sector have for the difference of $4.4 trillion in the past 70 years? A national highway system and the best equipped military in the world are just two prominent assets.

The federal government spends about 17-20% of GDP, far lower than the average of OECD countries (Note #7). That is important because the accumulated Federal debt of $15.5 trillion is only .9% of the $1.7 quadrillion of GDP produced by the private sector since January 1947. Our grandchildren have not inherited a crushing debt, as some have called it. In the next forty years, the U.S. economy will produce about $2 quadrillion of GDP (Note #8). If tomorrow’s generations are as frugal as past generations, they will generate another $18 trillion of debt.

Adam Smith called a nation’s debt “unemployed capital,” a more apt term. The obligation of a productive nation is to put unemployed capital to work for the community. Under the current international system of national accounting, there is no way to account for the accumulated net value of real assets, or the communal operating expenses of the private economy. Without a proper accounting of those items, we engage in noisy arguments about the size of the debt.

In next week’s blog, I’ll examine the inflation pressures of government debt. I’ll review the Federal Reserve’s QE programs and why it has struggled to hit its target inflation rate of 2%. We’ll revisit a proposal by John Maynard Keynes that was discarded by later economists.

////////////////////

Notes:

1. A video presentation of SovGov funding by Stephanie Kelton . For more in depth reading, I suggest Modern Monetary Theory by L. Randall Wray, and Macroeconomics by William Mitchell, L. Randall Wray and Martin Watts.

2. L. Randall Wray wrote a short 7 page paper on the Job Guarantee program . A more comprehensive 56-page proposal can be found here

3. Adam Smith’s The Wealth of Nations was published in 1776, the year that the U.S. declared independence from Britain. Smith invented the field of economics. The book runs 900 pages and is available on Kindle for $.99

4. Federal Expenditures FGEXPND series at FRED.

5. At the end of 1946, the Gross Federal Debt held by the public was $242 billion (FYGFDPUB series at FRED). Today, that debt total is $15,750 billion, or almost $16 trillion dollars. The difference is $15.5 trillion. The debt held by the public does not include debt that the Federal government owes itself for the Social Security and Medicare “funds.” Under these PayGo pension systems, those funds are nothing more than internal accounting entries.

6. In 2017, the Federal Reserve estimated interest and non-interest expenses for all commercial banks at 3% (Table 2, Column 3).

7. Germany’s government, the leading country in the European Union, spends 44% of its GDP Source

8. Assuming GDP growth averages 2.5% during the next forty years.