October 2, 2022

by Stephen Stofka

The dollar is the world’s reserve currency and its strength – its price relative to other currencies – is straining both the economies and the financial expectations of other countries. Businesses in developing countries with an unreliable currency regime often have to borrow in dollars – what is called “dollar denominated debt.” Businesses must make their loan payments in dollars so they must trade in ever more of their local currency to get the dollars to make the payment. European nations stocking up on liquified natural gas (LNG) from the U.S. are feeling the pinch as well. Why is the dollar strengthening?

In international finance there are two equations that model the relationship between expected inflation, exchange rates and interest rates. Currency traders are expecting inflation to moderate more quickly in the U.S. than in other countries. Because the U.S. has a better supply of natural gas, its energy prices will be less affected by the war in Ukraine. Secondly, the Fed has been increasing interest rates, enticing investors in other countries to invest their money in U.S. debt. The dollar-euro exchange rate has not been this low since 1999 when the Eurozone countries began using a common currency, the euro.

When the dollar gets stronger, exports decrease because American goods are more expensive to buyers in foreign countries. Imports become cheaper so Americans buy more stuff from other countries. However, if the U.S. is sliding into a recession, Americans are less likely to buy enough European imports to offset the LNG that European countries will buy from the U.S. This will increase the demand for dollars relative to the euro, further driving up the price of dollars in other currencies.

The dollar has been strengthening against other forms of currency like gold and digital exchange mechanisms like Bitcoin. Priced in dollars, gold has lost about 16% of its value in the past six months. Bitcoin has lost 60% since March. Gold is both a commodity and a currency. Gold holds a store of work that it can do in the future. It has cosmetic and industrial uses.

Bitcoin is the product of past work only – a “proof of work” done in the past. It stores no capability of future work. It takes a lot of electricity and computing power to mine Bitcoin but it cannot store electricity for future use. If it could do so, the price of Bitcoin would go up when electricity prices went up.

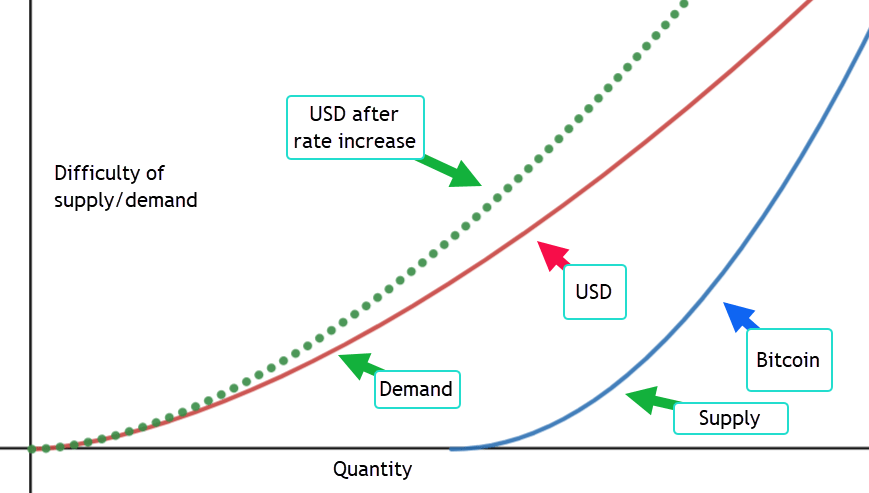

In the graph below I’ve illustrated a key difference between the dollar and Bitcoin. On the right is Bitcoin. Its algorithm incorporates a “diseconomies of scale.” As more Bitcoin is mined, it takes more effort to mine Bitcoin. Bitcoin focuses on the difficulty of supply.

On the left is the fiat dollar. There is no difficulty in supplying it. The Fed focuses on the demand for the dollar by adjusting the interest rate, the bend in the curve. It is currently tightening that bend – the dotted green curve – and increasing the difficulty of getting more dollars. The dollar can respond to changing demand more easily than gold or Bitcoin because it targets demand.

Like Bitcoin, the dollar stores no future work. In an article earlier this year (2022), I wrote that America’s store of wealth was both a proof-of-work, proof-of-stability and proof-of-trust. The dollar itself is only a sign of trust in American institutions. The checks and balances of our system of government ensures that most policymaking is incremental. While that frustrates Americans, the relative predictability of U.S. policy is reassuring to foreign investors. Americans often run around like crazy monkeys on the deck of a cruise boat but the ship is unlikely to make a large course correction.

Think of the bend in the curve as a toll for using the highway to the future. Bitcoin’s curve is rigid. The toll remains the same. Bitcoin enthusiasts would maintain that this rigidity should shift the curve to the right over time, increasing the buying power supplied by Bitcoin.

Let’s look at three approaches.

1) Bitcoin limits the length of highway that will be built. Enthusiasts claim that this will make each “mile” of the bitcoin highway more valuable.

2) MMT advocates offer a different solution. As long as there are resources – both labor and material – available, build more highway. By targeting the supply available, congestion will ease.

3) The Fed offers an approach that targets demand, not supply. The Fed raises and lowers the interest rate – the toll – to get onto the highway to the future. Raising interest rates is a form of congestion pricing. High inflation means that there are too many people using the available length of highway. The Fed has promised that it will keep raising the toll until fewer people are using the highway. As demand declines, some of those working on the highway may lose their jobs. Unemployment will increase but historically it is very low.

The strength of the dollar against other currencies, including Bitcoin and gold, indicates increasing demand for the Fed’s approach. What is the morality of an international floating rate regime where businesses in a developing country have to work even harder to pay their dollar-denominated loans? Bitcoin advocates claim that global adoption of Bitcoin will make a more even playing field, reducing the advantage that developed countries have over developing countries. That can be the subject of another article.

////////////

Photo by kyler trautner on Unsplash

Stofka, S. (2022, April 16). Fortress of Trust. Innocent Investor. Retrieved October 1, 2022, from https://innocentinvestor.com/2022/04/17/fortress-of-trust/