January 25, 2015

Valuation

Blogger Urban Carmel has written a thorough article on current market valuation, focusing on Tobin’s Q as a metric. This is the market price of equities divided by the replacement cost of the companies themselves. During the past 65 years, the median ratio is .7, meaning that the market price of all equities is about 70% of the replacement cost. At the end of December, the Tobin’s Q ratio was more than 1.1.

Are stocks overvalued? Valuing the replacement cost of a company might have been more accurate when the assets were primarily land, factories and other durable equipment. Today’s valuations consist of networks, processes, branding, and other less easily measured assets. The valuation discussion is not new. In 1996, before the U.S. shed much of its manufacturing capacity, economists and heads of investing firms argued about valuation, including Tobin’s Q. You can punch the way back button here and read a NY Times article that could have been written today if a few facts were changed.

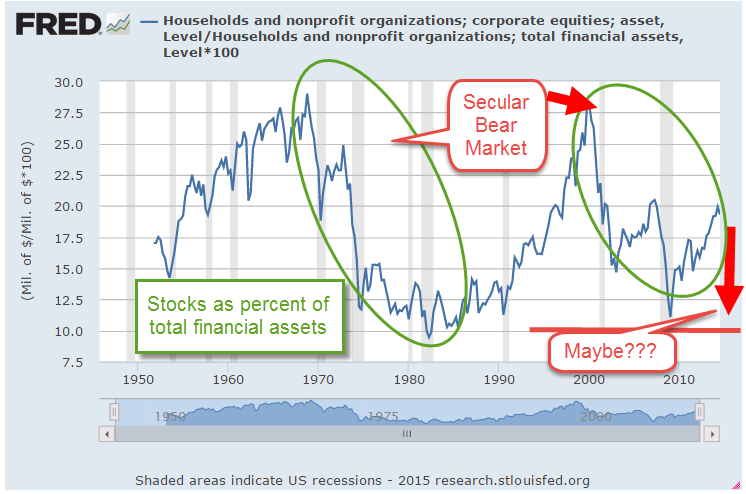

Currently, households have 20% of their financial assets in stocks, the same percentage as in 1996. In December 1996, then Federal Reserve chairman made a comment about “irrational exuberance” in market valuations. Prices would continue to rise, then soar, before falling from their peaks in mid-2000. At that peak, households held 30% of their financial assets in stocks. At an earlier peak, 1968, households had the same high percentage of their assets in stocks.

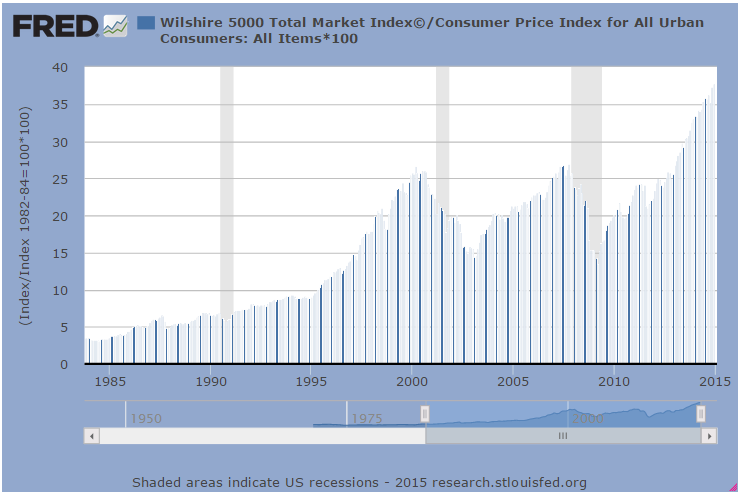

On an inflation adjusted basis, the SP500 has only recently closed above the all time high set in 2000 (Chart here). The Wilshire 5000 is a market capitalization index like the SP500 but is broader, including 3700 publicly traded companies in its composite. On an inflation adjusted basis this wider index is 40% above the peaks of 2000 and 2007.

Long term periods of optimistic market sentiment are called secular bull markets. Negative periods are called secular bear markets. (See this Fidelity newsletter on the characteristics of secular bull and bear markets). These long-term periods are easier to identify in hindsight. Some say that we are nearing the end of a long-term bear market, and that there willl be a big market drop to close out this bearish period. There have been so few long term market moves in 150 years of market data, that it is possible to tease out any pattern one wants to find. The aggregate of investor behavior is not a symphony, a piece of music with defined structure and passages.

******************************

REIT

As Treasury yields decline, mortgage rates continue to fall. The Mortgage Bankers Association reported that their refinance application index had increased by 50% from the previous week. The refinancing process involves the payoff of the previous higher interest mortgage. Mortgage REITs make their money on the spread, or the difference, between the interest rate they pay for money and the interest on loaning that money on mortgages. When a lot of homeowners prepay their higher interest mortgages, that lowers the profits of mortgage REITs like American Capital Agency (AGNC) and Annaly Capital Management (NLY). Both of these companies have dividend yields above 10% and are trading below estimated book value.

*****************************

Housing

Back in ye olden days, around 1950, the world was a bit different. The Bureau of Labor Statistics published a snapshot of incomes, housing, and other census data, including the data tidbit that people consumed fewer calories in 1950 than today, 3260 then vs. over 3700 today.

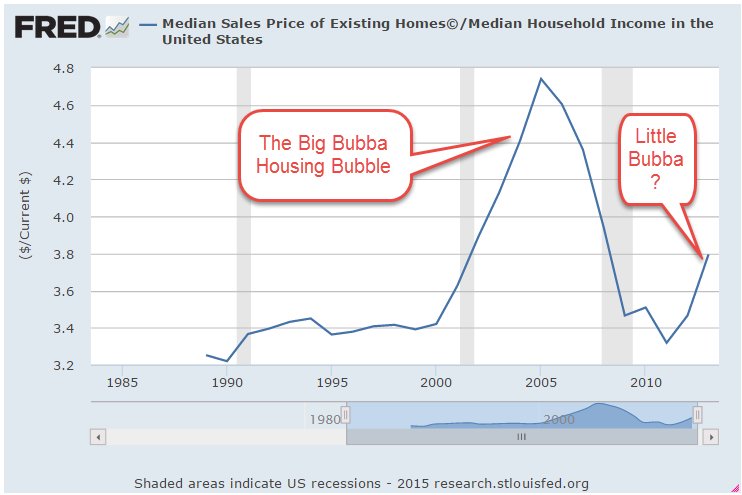

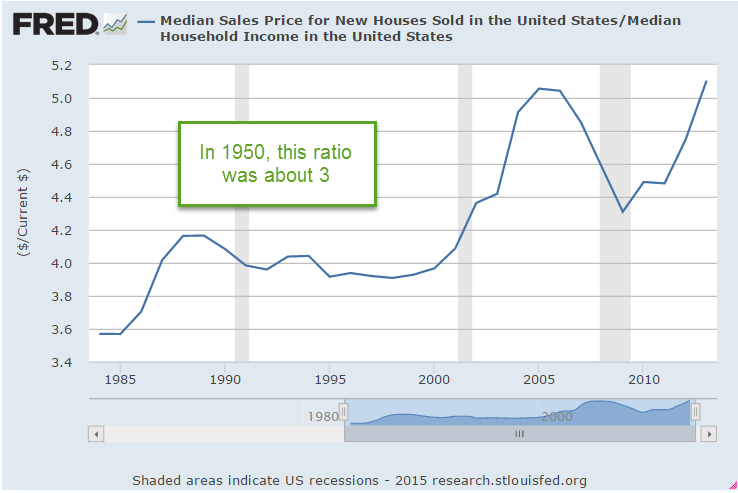

Housing and utilities averaged 27% of income in 1950 vs. 40% today. Food costs were 33% then, 15% today. The median house price of $9500 was about 3 times the median household income (MHI) of $3200. For most of the 1990s, the prices of existing homes were slightly higher, about 3.4 times MHI.

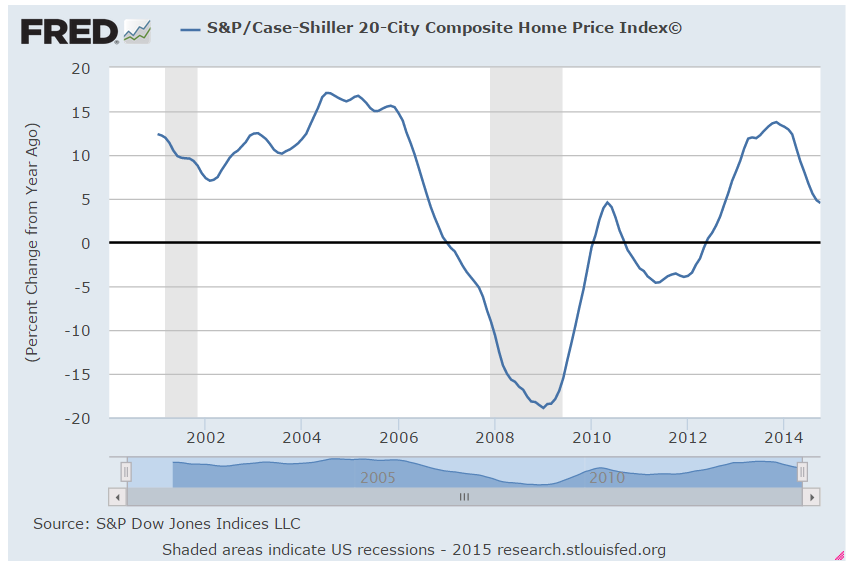

The prices of existing homes rose 6% in 2014 – healthy but not bubbly. However, the ratio of median price to median income is now at 3.8. Historically low interest rates have enabled buyers to leverage their income to get more house for their bucks, but the lack of income growth will continue to rein in the housing market.

The ratio of median new home prices to MHI has now surpassed the peak of the housing bubble.

*******************************

Retirement Income

Wade Pfau is a CFA who has written many a paper on retirement strategies and occasionally blogs about retirement income. Here is an excellent paper on the change in psychology, risk assessment and strategies of people before and after retirement. Wade and his co-author summarize the critical issues, the two dominant withdrawal approaches, the development of the safe withdrawal rate, and the caveats of any long term planning. The authors review the strategies of several authors, discuss variable spending rules, income buckets and income layering, annuities, and bond ladders. You’ll want to curl up in an armchair for this one.