January 4th, 2015

As the calendar flips from December to January, some favorite activities are predictions for the coming year and reviews of the past year. Here are a few predictions I’ve heard in the past few weeks:

“We think oil will continue to drift downwards as global demand slackens.”

“We think long term Treasuries will continue to show strong gains in the coming year.”

“Output remains strong, and the labor market continues to strengthen. We expect further gains in the stock market this year.”

“We expect gold to find a bottom in the $900 to $1000 range and we will be initiating a long position at that time.”

Predictions are foolish, of course. They are too certain. An expectation is a bit more sober, a pronouncement of a probability. Did anyone hear these expectations at the beginning of 2014?

“Oil prices will decline by 40% this year.”

“We expect long term Treasuries to gain 25% in 2014.”

“We expect the euro to fall to a 4-1/2 year low against the dollar.”

I don’t remember any of those predictions at the beginning of 2014. So here’s my expectation – er, prediction: in 2015, I will be surprised by some of the events that will unfold.

If that doesn’t satisfy your prediction craving, here are several – let’s call them guesstimates – of SP500 earnings and price predictions in 2015.

*********************

Blue Light Specials

As I mentioned a few weeks ago, there are a few stock sectors that are “on sale,” selling below their 200 week, or 4 year average. Falling gas prices in the last half of 2014 have had a negative impact on energy stocks (XLE, VDE). Selling below their 200 week averages in December, both ETFs are hovering at their 200 week average. The 50 week average is above the 200 week average, indicating that this is, so far, a relatively short term trend.

Emerging markets have been in the doldrums for a year and a half. The 50 week average is just about to cross above the 200 week, signalling that the downturn may have exhausted itself.

The mining sector (XME) is down – way down. The 50 week average is below the 200 week average and current prices of this ETF are below the 50 week average. The mining sector can be quite cyclical but could be quite profitable in the next six months.

In the summer of 2011, the oil commodity ETF USO lost a third of its value. In the melt down of 2008, it lost 75% of its value, falling from $115 down to near $30. This week USO broke below $20, losing half of its value since July. Since September 2009, shortly after the official end of the recession, the 50 week average has been trading in a range of $34 to $38, and is currently at the low point of that five year range. While this may not be appropriate for a casual investor, it might be worth a look for those with some play money.

Other sectors – industrials, materials, finance, health, technology, consumer staples, consumer discretionary, retail and utilities – are above both their 50 and 200 week averages.

*********************

Happiness Is An Open Wallet

The Conference Board’s Consumer Confidence gauge rose still further above 90 in December. At some time in the distant past, in a year called 1985, all the people were happier than they are today. That long ago time became the benchmark 100 for this index. The index number is less important than the trend of confidence – whether it is rising, falling or staying the same.

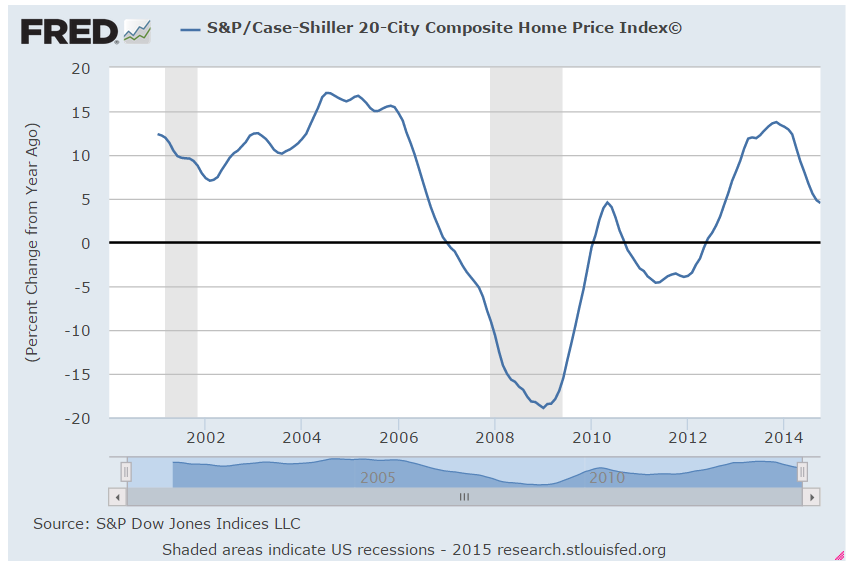

The Case Shiller 20 City Home Price Index for October showed a 4.5% yearly gain. The double digit gains of last year and the first six months of 2014 were unsustainable. However, I would be concerned if this continues to fall toward zero, indicating a serious softening of demand, or a lack of affordability or both.

***************************

The non-SP500 World

The SP500 index, composed of the 500 largest companies in the U.S., was up 11.4% for 2014. An index of mid, small and micro-cap companies was up a more modest 7.1% (Standard Poors) for the year. An index of REITs was up 25.6% in 2014 after stalling during much of 2011, 2012 and 2013. I was surprised to learn that during the past twenty years, REITs outperformed the SP500.

Conventional wisdom holds that rising interest rates are bad for REIT stocks. A study of REIT performance shows that the impact is less than most investors think. In addition, the income growth generated by REITs has outpaced inflation in all but one out the past 15 years. VNQ and RWR are two ETFs in this market space. VNQ has a 10 year return of about 9%, RWR a bit less.

***************************

Social Security

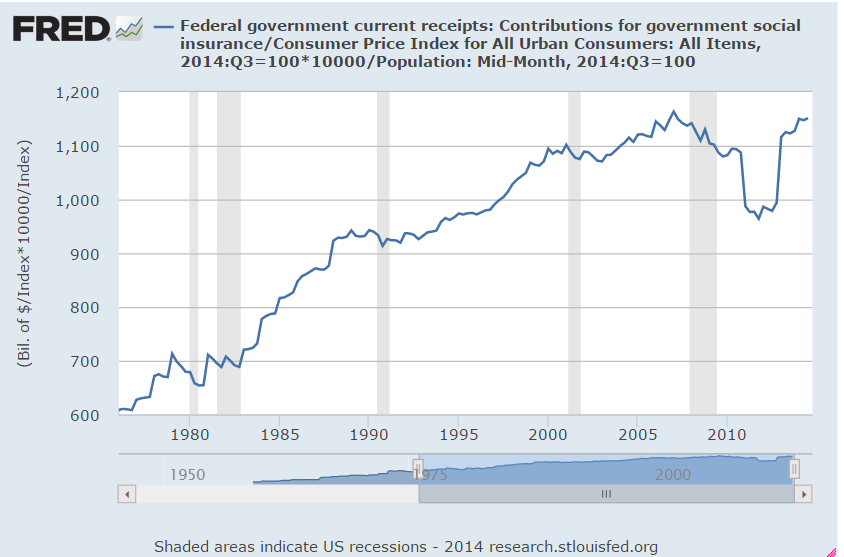

The Social Security program depends on current taxes to pay current beneficiaries. In per person inflation adjusted dollars, the federal government collects twice the amount of money it did forty years ago. Per person revenues have almost caught up to the levels of 2006.

The problem is that there are a lot of people starting to retire. Politicians of both parties have spent the excess social security taxes collected in the past decades. Last week I asked what you would do if the stock market lost 30% of its value.

This week’s sobering question for those in or near retirement: what would you do if social security payments were reduced, or means tested? With the stroke of a pen, Congress could reduce the maximum monthly benefit from $2533 to say $2100. This would affect a relatively small percentage of voters, those with higher incomes, a favorite target for benefit cuts. Perhaps you are taking care of an ailing child or parent and need the income. You might submit a 4 page form listing your pensions, IRAs, the assessed value of your home and any mortgage you had against the house, your mutual funds, stocks and bonds. Using a complex formula to factor in your age, special circumstances, the cost of living index in your area and the total of your assets, the Social Security Administration would calculate your monthly benefit. Can’t happen here in the land of the free, home of the brave?