November 18th, 2012

This past week, President Obama gave a post-election news conference, answering a number of questions about the fiscal cliff due to take effect on January 1st if the lame duck Congress and the President can not come to an agreeement on some budget bandaging. The stock market has had the jitters since the first week of October, falling 9% since then; about half of that decline came after the election. At almost the same hour that it became apparent that the balance of power in Washington would remain the same came the unwelcome forecast of no growth for the Eurozone in 2013. When in doubt, get out.

For the past two years, there have been few “Kumbaya” moments in the halls of Congress or the White House. The market has had a good run this year; capital gains taxes could increase next year; many decided to take their profits and run. A I wrote a month ago, the drop in new orders for durable goods was troublesome. Three weeks ago, the newest durable goods report showed further declines yet consumer confidence was up, creating a tug of war and I waved the yellow flag, saying that the “prudent investor might exercise some caution.”

For the long term investor who makes annual investments in their IRA, this drop in the stock market is an opportunity to make some of that contribution for this year. If the wrangling over revenue and spending cuts continues over the next few weeks, the market could drop another 10 – 15%. When budget negotiations collapsed in July – August 2011, the market declined almost to bear market territory – about 19%. All too often, some of us wait till the last minute in April to make our annual IRA contribution.

The “cliff” terminology was spoken by Fed Chairman Ben Bernanke at a hearing in February. He probably wished he had chosen less colorful language but he was probably trying to wake up some of the senators at the hearing. How bad is this cliff?

The total measured economic output of the U.S., its GDP, is estimated by the BEA (Bureau of Economic Analysis) at around $16 trillion – $15.85 trillion, to be exact, based on this year’s estimated growth of about 2.2% and next year’s average 2.75% estimate of growth. What’s a trillion dollars? About $9000 for every household in the country.

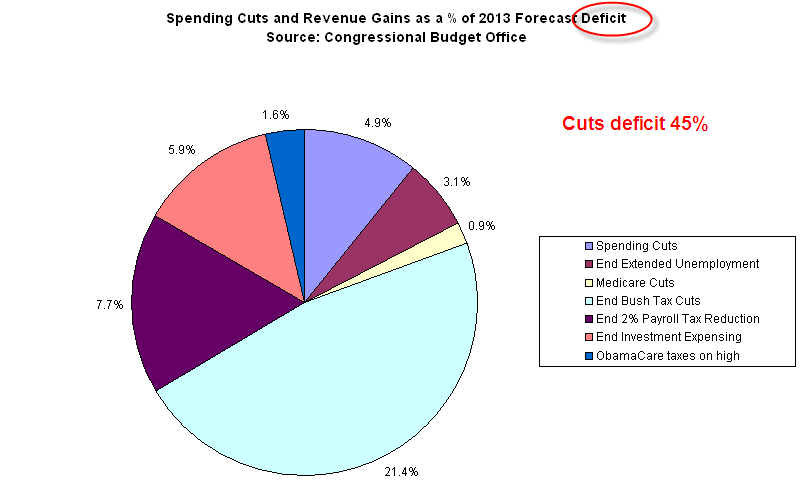

The non-partisan Congressional Budget Office (CBO) estimated some of the economic impacts if we did go over the cliff; in other words, if the spending cuts and revenue increases occurred next year. Below is a chart of the percentages of GDP that each component of spending cuts and revenue were to occur.

The total of these is 3.2% of the economy. Well, that’s not Armageddon, you might think and you would be right. As I mentioned earlier, forecast growth is only about 2.75% for next year so that means that GDP would contract slightly next year. On the other hand, the cliff sure helps the deficit for next year, cutting it by almost half. The deficit is projected at about $1.1 trillion before spending cuts and revenue increases. In more manageable numbers, the country is going to go further into debt next year to the tune of almost $10,000 for every household.

Politicians in front of a microphone are prone to hyperbole. So are news anchors. Politicians try to sell their version of the story; news anchors try to keep our attention. Small numbers like 3.2% of GDP might not get our attention so we could hear more dramatic numbers. News anchors may say “Spending cuts of $100 billion” because $100 billion sounds important. But without a total or a percentage, we have no context to evaluate the amount of money. Is $100 billion a little or a lot? $100 billion in spending cuts is .6% of the entire economy, or 2.6% of the budget for this coming year. We may hear “Revenue increases of $400 billion,” which sounds gigantic. It is 2.5% of the economy, or an additional 13.8% of the projected federal revenue. Remember, even with the revenue increases, should they take effect, the country’s budget will still be “in the red” an estimated $600 billion dollars, or $5400 per household.

This country needs more revenue and it needs to cut expenses. Each side of the aisle will fight to protect the “job creators” (interpretation: people with money) or the “working poor” (interpretation: people who are barely making it week to week) or the “middle class” (interpretation: the rest of us). Tax the other guy, not me. Cut the other guy’s deductions, not mine. Cut subsidies, but not mine. Cut expenses but not in my industry or area of the country. This is the same kind of behavior that 5 – 8 year old kids exhibited in an experiment featured on CBS’ 60 Minutes tonight. Maybe, just maybe, we need to grow up.