March 20, 2022

by Stephen Stofka

Why do unexpected price changes bother us so much? Prices reflect two forces central to our lives – time and utility. Both are common measures yet each is uniquely experienced. The price of our utility – what we need and enjoy – and the price of our time is deeply personal. Price surprises upset a finely balanced mechanism inside each of us. We can adapt to a one-time price change. We struggle to make sense of repeated and erratic price changes.

A proverb in the tool business is that customers don’t want a ¼” drill bit – they want a ¼” hole. The price of goods we buy is the price of the experience we get when we consume a good. We don’t want an ice cream – we want the pleasure of eating ice cream. The cost of ice cream is the price of our time enjoying it.

Interest is the price of money’s time the way that wages are the price of our time. Einstein once quipped that interest was the most powerful force in the universe. We compliment ourselves when we enjoy an unexpected bonus return on our savings. We are outraged when the power of interest works against us. A credit card debt or student loan debt may grow even though we are making regular payments.

The price of money’s time and the price of our time are like two riders on a seesaw who seek an approximate level. For two decades the Federal Reserve has sat on the interest rate side of the seesaw to keep them close to the ground. In response, the prices of consumption assets (houses) and productive assets (stocks) have risen high. What about the price of consumption goods?

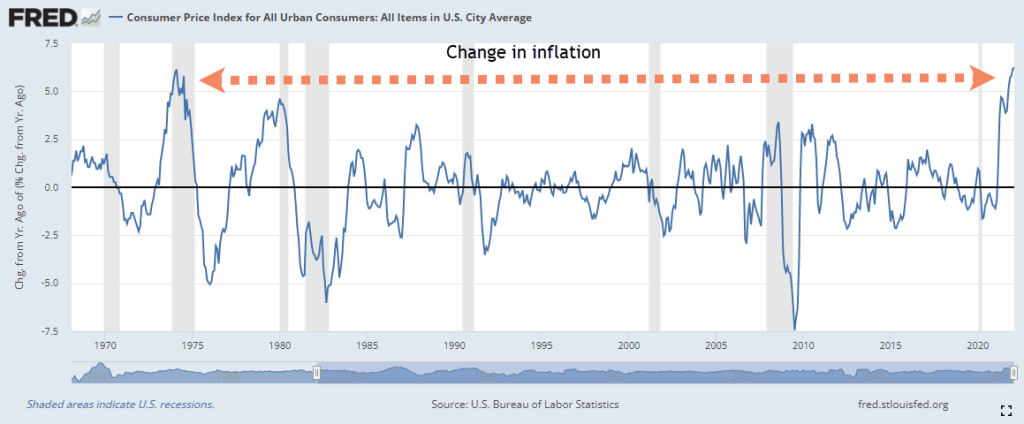

Inflation measures changes in the price of consumption goods the way that our car’s speedometer – the mileage indicator – measures our change in position on the road. We adapt to constant speed or inflation. What we notice then are the changes in speed or inflation – the acceleration. After a decade of low inflation, the pandemic was like approaching a highway junction and coming to a near stop before having to accelerate onto another highway. In mid-2021, the sudden acceleration of price changes seemed normal, a catching up after the economic lockdowns of 2020. The acceleration has continued for months now, as though the gas pedal got stuck. Using the FRED data tool at the Federal Reserve, I have charted the price acceleration – the change of inflation.

Today’s price acceleration is as high as that of the deep recession in 1973-74. Two shocks – one of them short term, one long term – produced a singular phenomenon economists called stagflation. The short term shocks were two oil crises in 1974 and 1979 that decreased world oil production (Gross, 2019). The long term shock was the large influx of the Boomer generation into the labor force, doubling the 1% average growth of the labor force. Forty years ago, the Boomers were in their late 20s and early 30s – at that age when we have increasing incomes and material needs. Lopsided demographics and supply shocks combined to produce erratic price changes.

To bring price acceleration under control in 1979 Fed Chair Paul Volker kept raising interest rates (FEDFUNDS) to keep them above the inflation rate. Interest rates acted as a cap on price changes. Once these two forces balanced, the change in inflation decreased but there was a cost. At that time, small businesses paid 20% interest for unsecured short term loans to cover payroll and accounts receivable. The change in interest rates was swift enough and large enough to drive the economy into recession. Until the 2008-9 financial crisis, the 1981-82 recession was the worst since the Great Depression of the 1930s.

This week, Fed Chair Jerome Powell announced a series of small and steady interest rate hikes with a target that is far below the interest rates of four decades ago when a 10% mortgage rate was a bargain. The demographics are different today. Because the labor force is barely growing structural price pressures should weaken. The large Boomer generation is aging and old people don’t buy as much stuff. The Fed can let the interest rate side of the seesaw rise up a bit and hope that inflation will lower in response. Instead of having to cap price changes as they did four decades ago, they can work to a negotiation between these two price forces.

////////////

Photo by Miles Loewen on Unsplash

Gross, S. (2019, March 5). What Iran’s 1979 revolution meant for US and Global Oil Markets. Brookings. Retrieved March 18, 2022, from https://www.brookings.edu/blog/order-from-chaos/2019/03/05/what-irans-1979-revolution-meant-for-us-and-global-oil-markets/