February 14, 2015

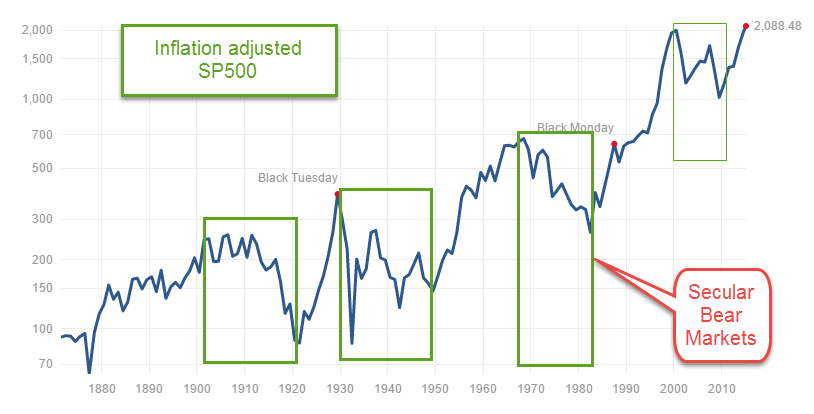

In January of this year, the SP500 finally rose above the inflation adjusted high set in 2000. Here is a chart from multpl.com that I have overlaid with a few boxes. Long term market trends are dubbed “secular” to contrast them with the shorter cyclical swings in valuation. A secular bear market is a prolonged market downturn in which the inflation adjusted price of the SP500 never gets above a certain historical peak.

These long term periods are easier to define in hindsight. They have begun with some peak and ended at some trough. Years after the trough when the market has made a new inflation adjusted high price, market watchers get out their crayons and set the end of the bear market just after that trough. Based on that historical rule, we would then say that the secular bear market that began in 2000 ended in 2009 at a market low six months after the onset of the financial crisis.

If history is any guide, an investor could expect further price increases for another 2 years (as in the late 1920s), or another 10 years (as in the late 1950s to late 1960s), or another 8 years (as in the 1990s). In other words, history may not be much of a guide.

If the market tanked in 2017, two years after setting a new high, some sages would nod soberly and say it was just like the 1920s and was to be expected. If the market continued rising another eight years before falling, ah yes, just like the 1990s. The signs were all there if you knew where to look.

Secular bear markets share characteristics other than long term price swings. During past prolonged downturns there have been five recessions within each period. We have had two recessions since 2000. Price to earnings, or PE, ratios went really low – about 6 – at the lowest trough of past downturns. This is also the approximate low in the Shiller CAPE ratio. Since 2000, the PE ratio has fallen to 10; the CAPE ratio to 13. The current PE ratio based on the trailing twelve months earnings is almost 20, about 25% above the average. The number of years from peak to trough has been 19. 2000-2009 would be only 9 years, the shortest secular bear period on record. The number of years from peak to peak has been about 26 years, much longer than the current 15 year period.

This has led some to predict a further final crushing decline in the market to end the secular bear. If the doomsayers are correct and we are only two-thirds through a secular bear market, we would expect market prices to plateau this year. Then will come some shock – China’s real estate market implodes, or its regional banks collapse. The so called PIGS – Portugal, Ireland, Greece, and Spain – could exit the euro. There could be a major armed conflict with Russia or Iran that causes investors to abandon equities in droves. The stronger dollar can put strains on countries whose currencies are pegged to the dollar. Such strains can cause a financial crisis similar to the one in Mexico in 1995 and the Asian and Russian crises of 1997 – 1998. In the summer of 1998, the SP500 fell 15% in one month as fears grew that regional monetary imbalances would infect the economies of the entire world.

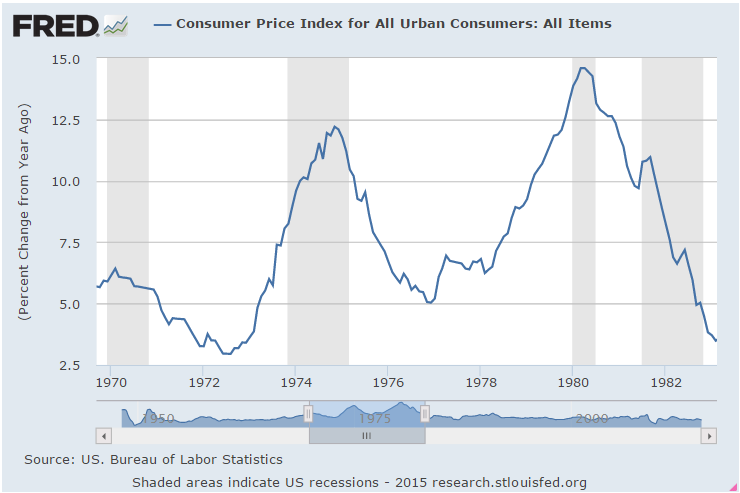

Secular bear markets come in types. The two that started in 1929 and 2000 arose from what I call discovery shocks. Investors lose conviction in their own hopes of future gains and leave the market. The bear market that began in the late 1960s was a series of conflict shocks that spurred erratic changes in inflation. As the country borrowed money to fund the Vietnam war, inflation rose above 3%, peaking at 6% in the spring of 1970. The 1970s was marked by domestic and international conflict: the Watergate scandal and the oil supply wars with OPEC drove inflation to a high of 12% in late 1974. As oil prices quadrupled through the 1970s, inflation spiked at almost 15% in the spring of 1980. Through most of the decade, inflation stayed above 5% – a low that was almost double the historical average.

The SP500 made new records again this week although FactSet notes that the blended earnings growth for the fourth quarter of 2014 was only 3.1%. The forward P/E of the SP500 is 17.1%, substantially above both the five and ten year averages (see paragraph below for illustration of changes in forward P/E). FactSet reports that nine out of ten sectors have forward P/E ratios that are above their ten year averages. Only the telecom sector is selling slightly below its ten year average. The forward P/E of the SP500 is based on projected earnings over the next year and volatile oil prices have made such earnings estimations difficult. First quarter earnings by energy companies have been revised downwards by 50%, resulting in a 7.4% decrease in earnings estimates for the SP500.

Small changes in earnings estimates are multiplied 10 to 30 times to reach an evaluation of fair market price. If 2015 earnings for SP500 companies are estimated at $100, an index price of 2000 is a forward P/E of 20. If estimates are revised upwards to $110, then an index price of 2000 reflects a forward P/E of 18. If the forward P/E of the SP500 is above the five and ten year averages as it is today, it means that investors and traders are betting that estimates of forward earnings will be revised upwards, resulting in a lower forward P/E ratio.

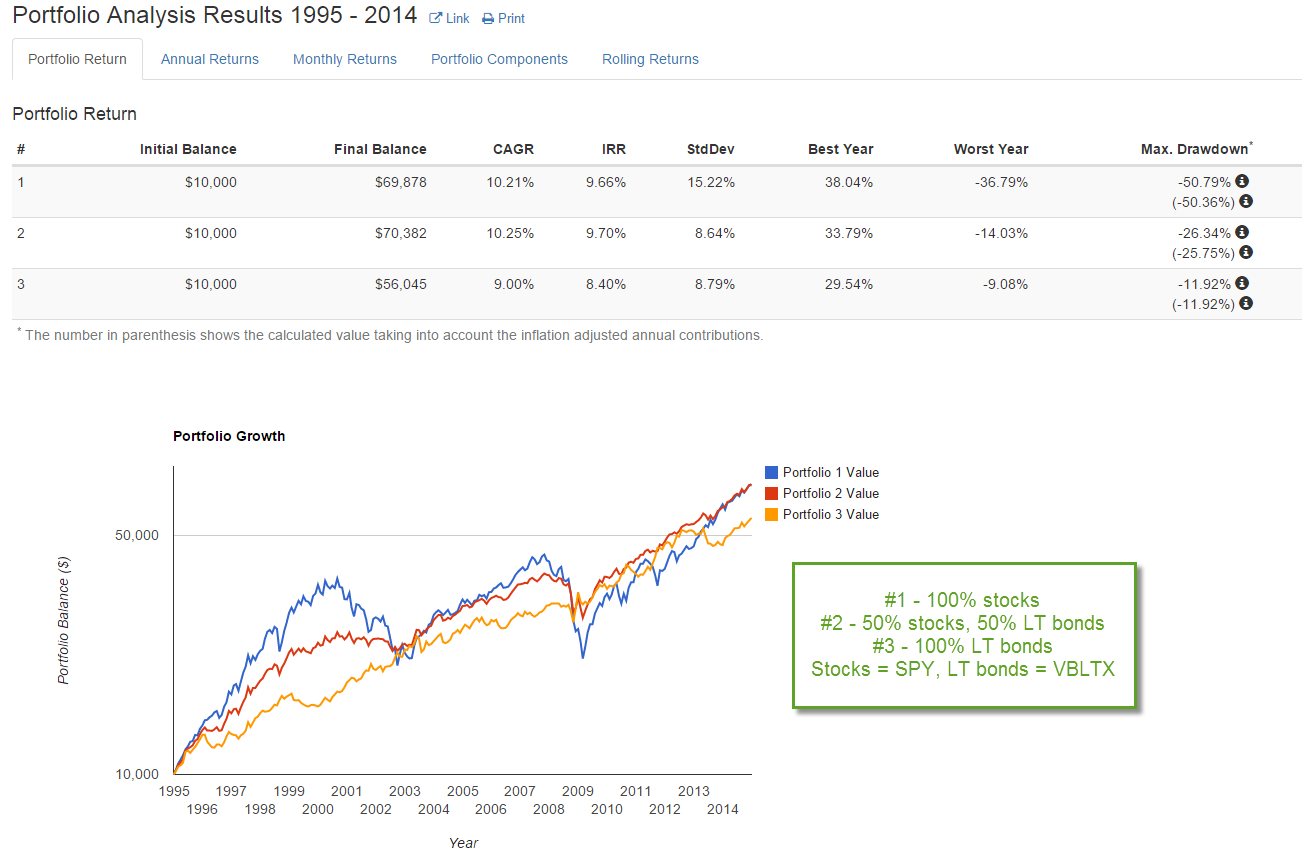

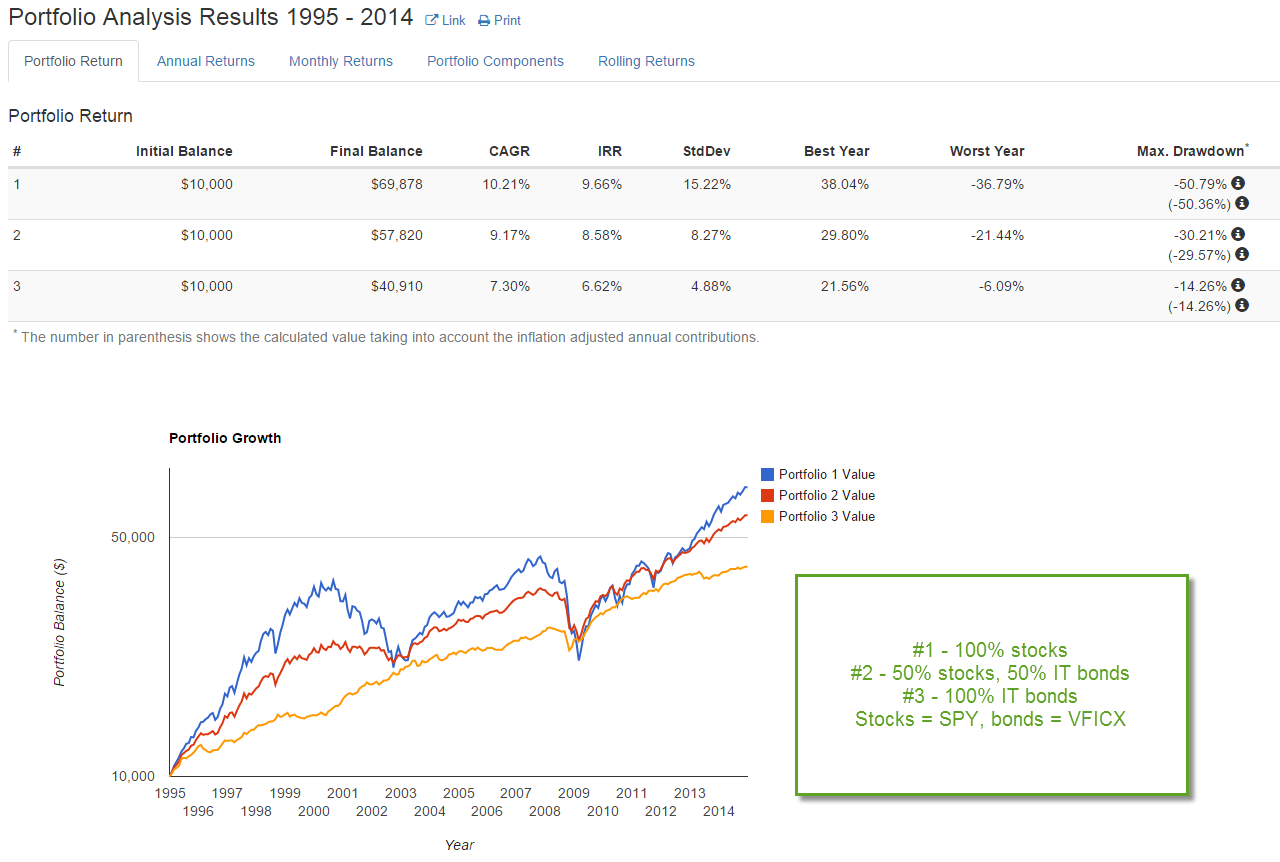

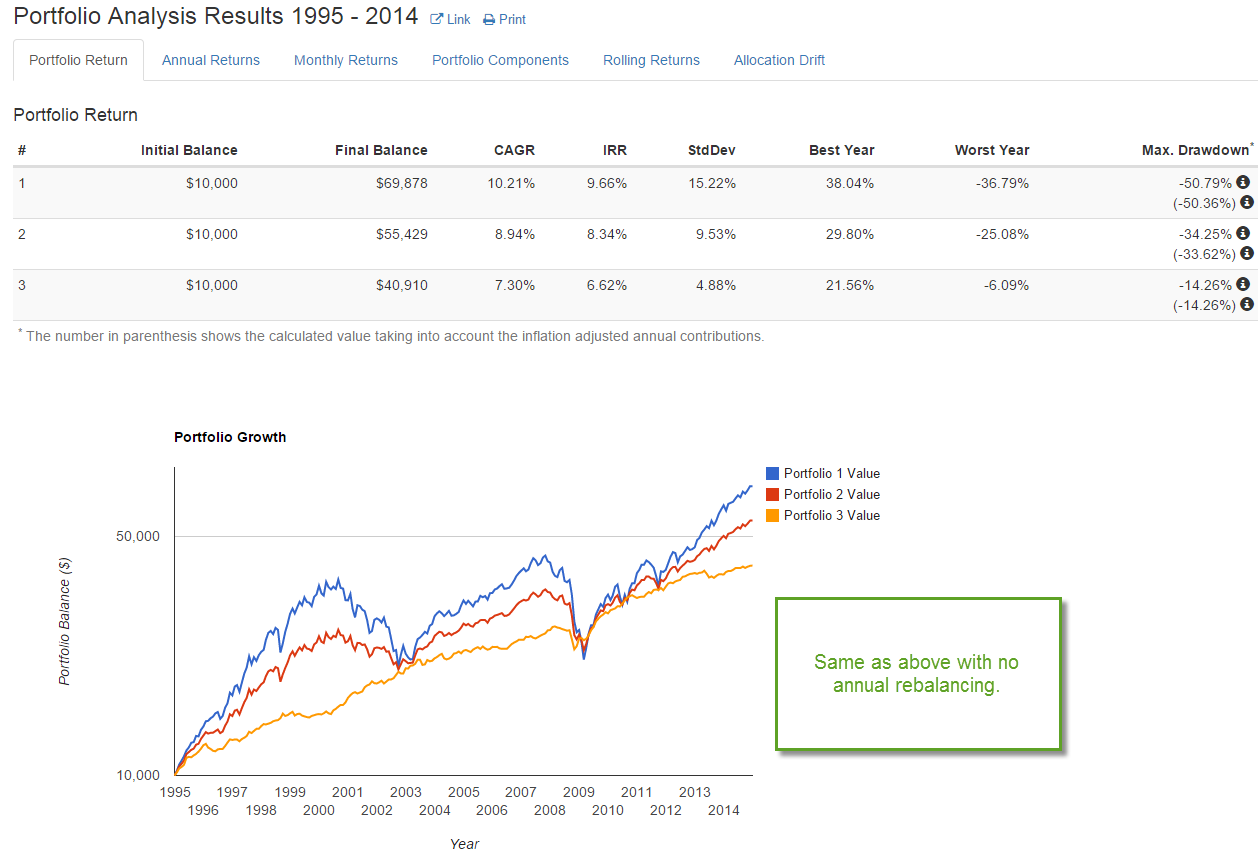

Long-term Treasuries (TLT) rose up 11.5% in the five weeks from late December to the end of January – too much, too fast. After falling back in the last two weeks from their peaks, they are priced at the same level as in July 2012. In 2014, traders who bet against long term bonds in anticipation of rising interest rates got slaughtered as long term Treasuries rose 25%. Investors who moved out of long term and into shorter term bonds were disappointed as well.

*****************

Retail Sales

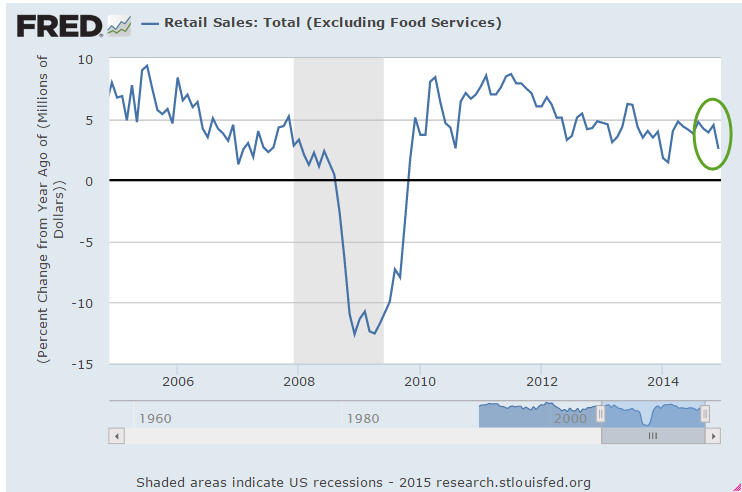

Investors regard the monthly employment report and the retail sales report as the most important barometer of a consumer driven economy. As an example of the correlation, consider a graph of inflation adjusted retail sales and the SP500 index.

Retail sales in January declined slightly from December. Investors were somewhat heartened by the 2.4% annual gain, at least 1% above inflation, but remember that last January was particularly poor and was an easy benchmark to beat. On the other hand, lower gasoline prices lowered this year’s total, offsetting the comparison with a weak benchmark.

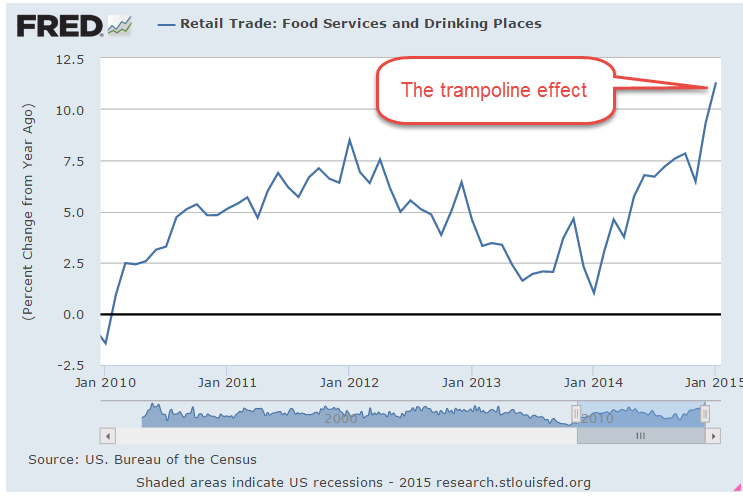

Sales at food and drinking establishments rose more than 11% y-o-y in January.

Large y-o-y gains in food and drink usually occur in the winter months. January 2000, 2001, 2004, 2006, December 2006, January 2012, and these past two months all peaked at more than 8% y-o-y gains. Eating and drinking out are largely discretionary for most of us. A change in the pace of growth in this behavior signals changes in consumer attitudes that are more real than a consumer confidence survey. Changes in this discretionary budget item is a survey of wallets. In the past year, the growth of food and drink sales has accelerated, indicating a more confident, less fearful consumer.

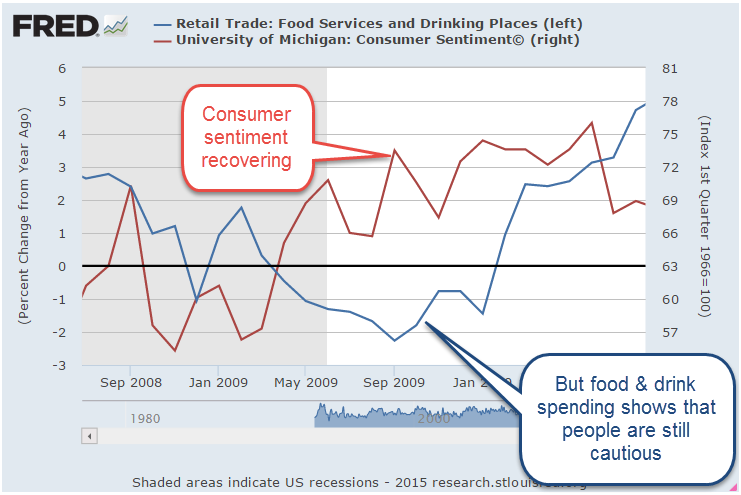

While the various consumer sentiment surveys indicate what we tell interviewers, the wallet survey indicates what we really think. In early 2009, the U. of Michigan Consumer Sentiment Survey showed a rebound of confidence. What the survey indicated was more a rebound of hope, not confidence. Consumer spending on eating and drinking out was still declining.

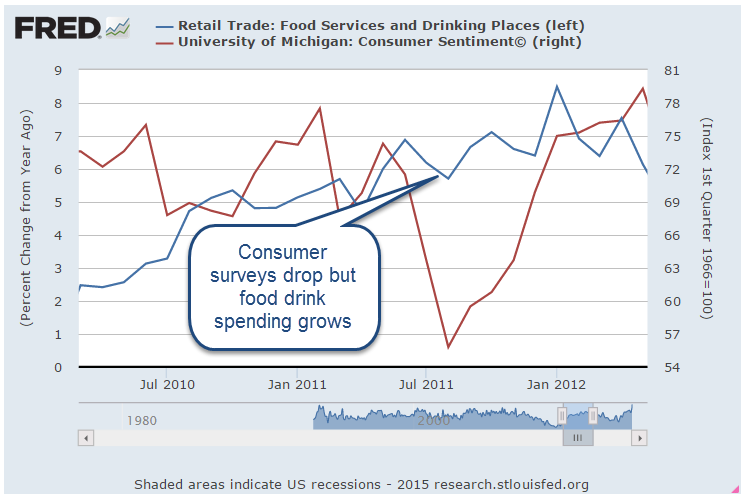

2011 is an indication of the opposite – plunging sentiment according to a survey but growing spending at food and drink establishments, indicating that the volatile drop in sentiment might be short lived. The plunge in confidence was a response to the budget battles between the Republican House and the President.

Low inflation, relatively low gasoline prices, strong employment and retail sales gains all point to steady moderate growth. Judging by the PE (19.7) and forward PE (17.1) ratios, the market may have already priced in that growth.