November 12, 2023

by Stephen Stofka

Note: at the end is a correction to last week’s letter.

This week’s letter continues to investigate the subsidies, both direct and indirect, that secure re-election for politicians but make deficits inevitable. This week there was weak market demand for $24 billion of newly issued 30-year Treasury bonds, forcing primary dealers like J.P. Morgan to absorb 24% of the debt, more than twice their usual participation rate. Treasury bonds carry little if any credit risk because the U.S. can always pay its debts by issuing more debt. However, long term debt exposes traders to market risk that they must offset by demanding a higher rate of interest for purchasing the debt. Higher interest payments narrow the budget space for subsidies and benefit programs that politicians dole out to gain constituent support. The long term outlook is that our arguments over fairness will cause greater fractures in our society.

As social animals we begin at an early age to form a sense of fairness that can test parents’ patience. An older sibling gets to stay up later at night and that is unfair. The level of chocolate milk is lower in one glass than in a sibling’s glass and that is unfair. We sympathize with animals who suffer the loss of their parents, their herd, or their environment. While we may have an instinctive ability to recognize unfairness, we must be taught how to construct rules that are based on fairness. These involve conflicts over sharing toys, a playroom, or a TV game console. Through experience and temperament, we build a framework of fairness that is unique. As we grow older we glue these values together with justifications and associate with others who share similar values. We form interest groups that compete for federal, state and local benefits, reasoning that our welfare is the general welfare.

We have been taught since childhood that public laws and public monies should be spent on the public good. We may not recognize property arrangements that advantage one group by disadvantaging another group, or at the expense of the general public. The exchange of goods and services take place in a web of property rights whose density obscures the dependencies between parties. Those rights are instituted and enforced by a network of government institutions – a legislature or council, an executive agency, the courts and a police force. Those rights favor a majority according to some characteristic, or an effective interest group that directs public money and property to their cause.

At the heart of most contentious Supreme Court decisions is the reality that one group of people in this country are going to indirectly subsidize others. One group of people will have to give up something – call it rights, power or a sense of safety – for other people to enjoy rights, power or greater security. More than 200 years ago, Adam Smith wrote that a well governed society with a respect for private property could produce a greater prosperity for everyone in the society. His was a long term vision. In the short term empowerment is a zero sum game and that is why so many issues in our society are contentious.

When a subsidy benefits a relatively small group of people, they fight hard to protect that subsidy. When the costs for the subsidy are spread over a large group, there is little opposition to the subsidy. An interest group becomes part of an Iron Triangle to protect the subsidy. This triangle consists of the interest group, a legislative subcommittee and an executive agency. An example is the ethanol subsidy. Department of Energy data shows that, in 2022, 35% of the corn crop in America was devoted to the manufacture of ethanol. Over its life cycle, ethanol added to gasoline reduces greenhouse gas emissions (GHG) by 40%, according to several studies. Farmers receive a maximum subsidy of $20 per dry ton of corn or other feedstock that they sell to biofuel plants. Biofuel producers receive a tax credit of 46 cents per gallon of ethanol. The consumer’s cost for the 10% addition of ethanol is small. The benefits to the ethanol blenders and farmers is large. A senator or representative in a farm state like Iowa is expected to protect that subsidy.

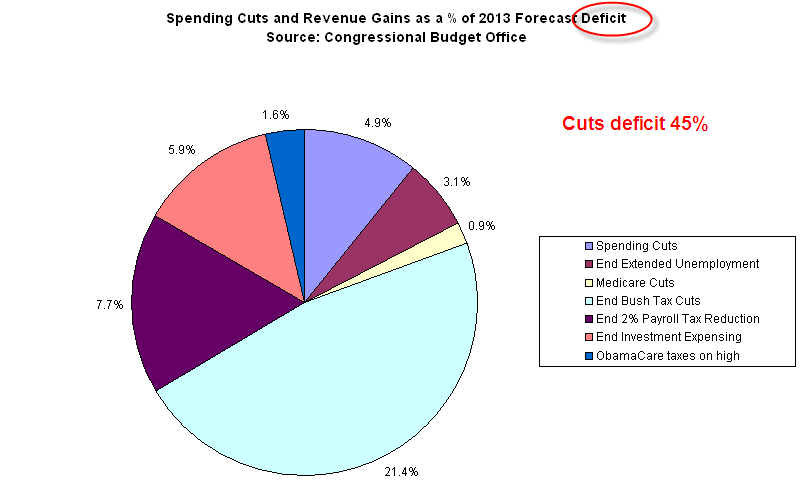

As I noted last week, just six tax expenditures reduced tax revenue to Treasury by almost $700 billion last year, more than half the total deficit. The largest expenditures were the exclusion of employer paid pension contributions and health insurance premiums. How many of us will agree to give up their tax exclusion in the interest of making tax rules uniform? Homeowners can enjoy 30-year mortgages at low rates because the federal government effectively underwrites those mortgages. In Britain, homeowners do not enjoy the protection of decades-long mortgages. According to a recent article in Forbes, 800,000 fixed rate mortgages in Britain were due in 2023, and 1.6 million will be due in 2024. Homeowners will have to remortgage at higher rates.

The slim Republican majority in the House cannot agree within their own caucus to bring a bill before the House for a vote. Lawmakers prefer to complain about spending because that is a popular stance with their constituents. A lawmaker’s abiding concern is getting re-elected by their constituents. Few will complain about raising tax revenues if the revenues are to come from a broad group of taxpayers. Democratic politicians argue for higher taxes on a small group of the rich for fear of antagonizing the majority of their voters. Reducing revenue by subsidies and tax exclusions is as much a policy choice as spending appropriations. Without a continuing resolution in the next week, the federal government will begin to shut down non-essential facilities. The House has not been able to produce a budget on time in thirty years because lawmakers have limited choices. Taxpayers, favored industries and social welfare interest groups will oppose a lawmaker who advocates the elimination of a tax exclusion, a subsidy reduction for producers or households.

We are a nation competing for space at the public trough. For at least a generation, our federal government will be unwilling to collect enough revenue to meet spending commitments. Buyers of U.S. debt will realize the inevitability of deficits rising faster than economic growth and reduce their holdings of long term bonds.

//////////////////

[Photo by Anna Samoylova on Unsplash

Keywords: ethanol, subsidy, tax expenditures, deficit

Correction: In last week’s letter I wrote “ twice last year’s deficit of $118 billion.” The link was to the average monthly deficit. That should have read “twice last year’s average monthly deficit of $118 billion,” not the deficit for the entire year. The total deficit for last year was $1.375 trillion.