On a recent vacation road trip, I enjoyed a number of tourist sites. At Carlsbad Caverns in New Mexico, I learned that 2000 men with the CCC (Civilian Conservation Corp) built most of the visitor walkways and accomodations in the caverns between 1938 and 1942. Not only did the Caverns project provide enjoyment and a learning experience for me seventy years later, it provided work for a country still suffering through a long depression. In Corpus Christi, I learned that, in the early 1970s, the sand dunes had been reclaimed by a joint effort of Texas and the Federal Government. Stopping at a scenic site in west Texas, I read that visitor accommodations had been built as part of the Federal Highway project in the 1950s. At Big Bend National Park, I learned that Texas had turned these deep canyonlands into a state park in 1935, providing work for many in the process.

What tourist sites will our children and grandchildren visit? Will they read any signs that herald the hard work of those who lived through this Great Recession? Why not? Politicians argued about the budget and the national debt in the 1930s, in the 1950s, in the 1970s, just as they do today. Then they got to work and made something happen. Democrats and Republicans have sat on opposite sides of the fence and pointed fingers at each other in those past decades – then grudgingly came to a compromise and got something done, putting thousands to work on enduring projects. Fifty to a hundred years from now, will there be any projects built by this generation that will have visitor plaques that our great grandchildren can read while on vacation?

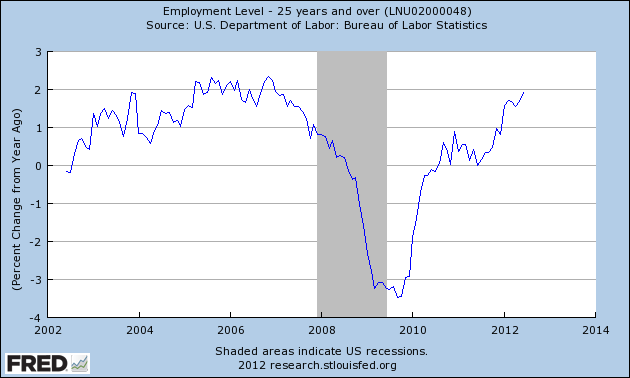

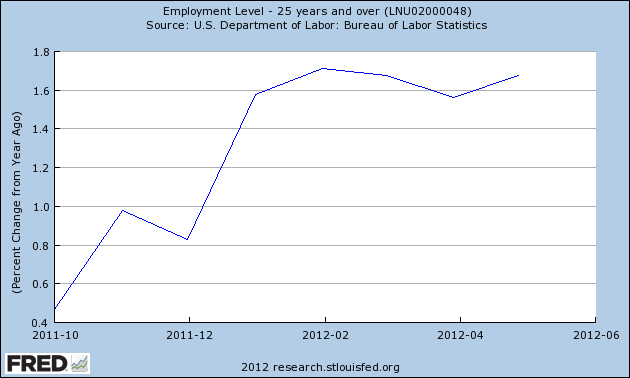

With that, I’ll turn to the June employment report. The headline number was a disappointment to many. Although the number of jobs increased by about 75,000, it was less than the 120,000 hoped for. The good news is that the year over year percent increase in jobs for most of the working population continued to increase.

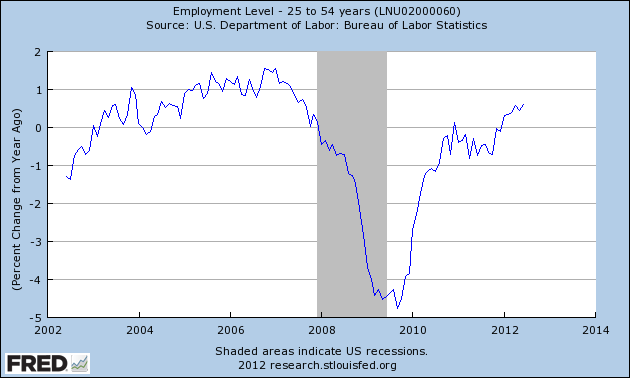

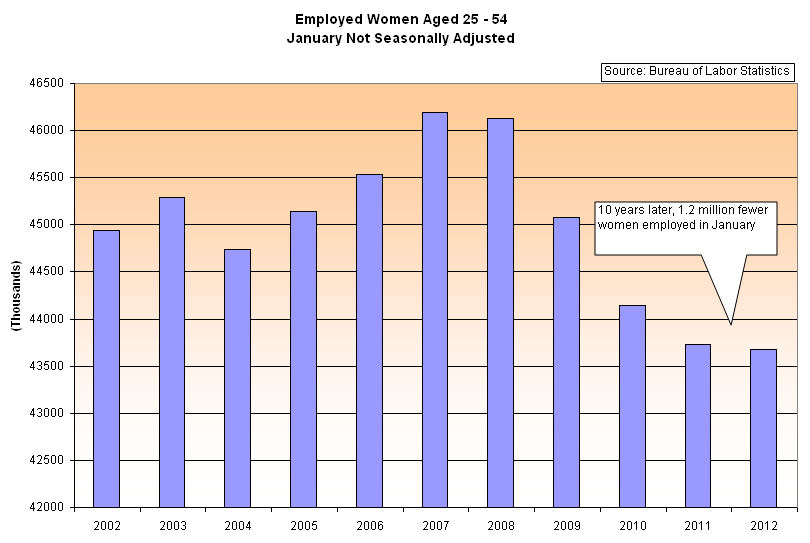

The core working force – as I call it – those aged 25 – 54 continued to show modest positive increases as well.

The problem is that it is still not enough. In the larger work force, aged 25+, we would like to see sustained 1.5% to 2% year on year growth to pull the economy up and out of the quicksand. Despite all the rhetoric from the politicians who claim they know how to create jobs, those of us who actually create jobs know that the chief reason for the lack of stronger hiring is the politicians themselves. The June survey of the National Federation of Independent Business (NFIB) a small business organization, reported that about 25% of business owners “who say it is a bad time to expand blame the current political mess.” Another quarter of respondents blame weak sales, a fifth blame taxes and another fifth blame “unreasonable regulation and red tape.” The number of firms planning to hire in the next six months offset approximately the same number of firms planning on reducing jobs. In short, a lackluster preview of the second half of the year.

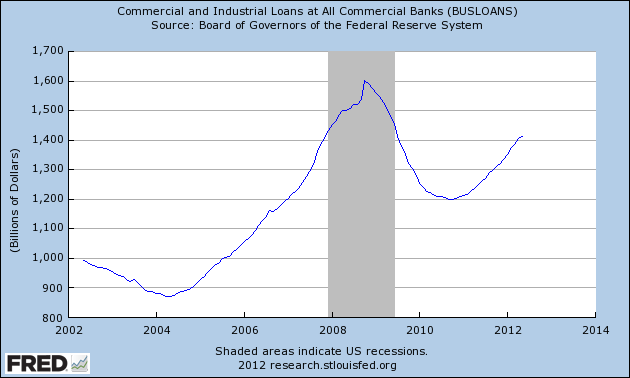

Over the past two years, business loans are continuing to grow, indicating increasing investment.

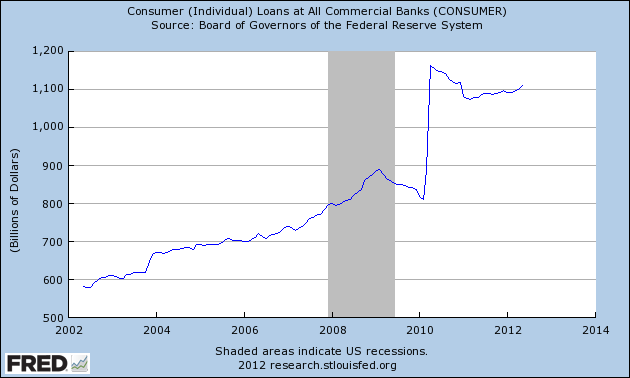

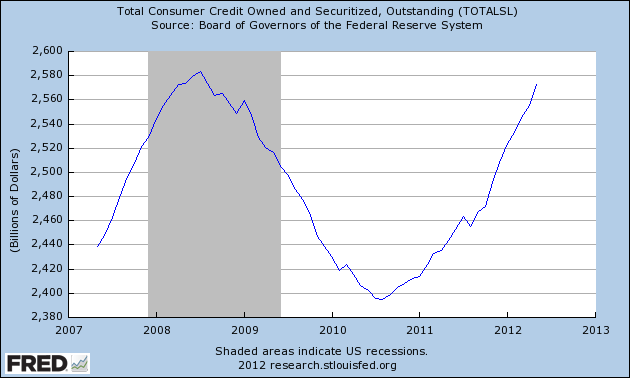

Businesses are preparing – cautiously – for increased consumer spending. But consumer loan growth has stalled after a severe decline at the onset of the recession several years ago. The spike in the first quarter of 2010 was an accounting change (explanation)

A bright spot – or dark spot – is the increase in overall consumer credit, approaching the levels of 2007. Are consumers more confident? Recent surveys don’t show that. Are consumers more desperate and charging more to make up for a lack of income growth? Probably.

Disregard the rants and promises of blowhard politicians. Consumer demand initiates most of the job creation in this country. Businesses respond to that consumer demand by hiring more employees. Without the demand, business owners create few jobs. The only jobs created are sales and advertising jobs as business owners try to increase demand or take sales away from competitors.

In the coming months before this election, I encourage all of you to ask two questions of your representatives, senators, president and presidential contender:

1. If consumers are still cautious, what policy can you implement that will encourage consumers to spend more?

2. If businesses are still cautious in their outlook, what policy can you implement that will encourage them to invest more in new jobs and equipment?

If the politician is a Republican, he or she will say that reducing regulations and taxes for businesses will help them create more jobs. Ask them how that will help create jobs if the business has only tepid sales growth. Should businesses hire more people just to sit around and fiddle their thumbs?

If the politician is a Democrat, they will talk about “investment” but what they mean is government spending to take the place of the lack of consumer spending. How are they going to encourage consumers to spend more? Silence.

Neither party has an answer to the problem of deleveraging, which is what consumers have been doing for the past several years. They borrowed against their homes and their homes went down in value. They charged more on their credit cards to make up for the lack of growth in their real incomes. They had to pay down or default on that credit before charging more. Deleveraging is a process that must be endured.

Unlike the individual states, the federal government has the constitutional capability of borrowing money. While the federal government can not solve the problem of consumer deleveraging, it can soften the impact by borrowing to initiate the same kind of projects that the federal government, together with the states, did in previous decades: build and improve stuff that we can put a plaque on! I do not like increasing government debt but I do like visitor plaques and informational signs at scenic and tourist sites. Fifty years from now, will the Boomers be known as the Stumble Bum Generation or the Plaque Generation?

{kind=link}