Nov. 30, 2014

The short week of Thanksgiving should have been rather uneventful. The week before, officials in Ferguson, Missouri had announced an imminent decision in the grand jury hearing of the fatal shooting of Michael Brown, an African American, by Darren Wilson, a Ferguson police officer who was European American.

Slavery, the denial of civil rights to African Americans, and persistent housing and job discrimination against African Americans are an integral part of American history. Bankruptcy is a formal discharge of debt. There is no formal procedure for discharging past wrongs. Some Southerners are still distrustful of the Federal bureaucracy in Washington that committed so many wrongs in the period after the Civil War. The wounds inflicted by white skinned Americans on dark skinned Americans is fresher than those suffered by Southerners during the Reconstruction period almost 150 years ago. Fresh wounds bleed easily when scratched.

The grand jury took several days longer than “imminent” to reach its decision, announced Monday night. Several weeks of protests during the course of the hearing erupted into violent rioting at the grand jury’s decision that Officer Wilson should not be indicted for any charges, ranging from first degree murder to manslaughter. The decision, right or wrong on the facts, picked at the scab of the soul of some African Americans, provoking senseless violence. Americans of every skin color riot when their team wins the World Series (San Francisco 2014) or Super Bowl (Denver 1998). Dark skinned Americans riot when they perceive that some injustice has been committed against them.

The costliest riots, over $1 billion in damages, had occurred in Los Angeles in 1992 after the Rodney King beating. Whether in response to victory or injustice, rioting provoked confusion and condemnation in any society. It was both uncomfortable and strangely seductive to watch the emergence of a super two-year old, having a temper tantrum, from a group of civilized human beings.

Property damage from civil unrest was covered by many business insurance plans, George knew, but he wondered how many businesses damaged in the Ferguson riots were covered for interruption of business operations, replacing some or all of the owner’s lost income. Sometimes these were sold as riders to a commercial policy.

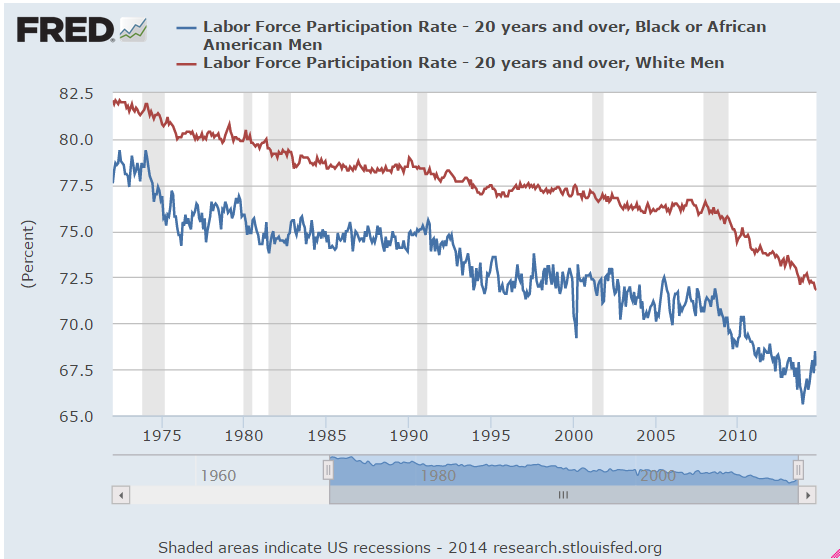

People with jobs were less likely to get angry. Unemployment among African Americans was at the same level as the early seventies, when the economy was in a severe recession, and the oil embargo and inflation had prompted Nixon to enact wage price controls. Those had not been good times for many Americans. Five years after the official end of this last recession, the unemployment rate among African Americans was twice the rate of the general labor force.

The participation rate among African Americans was about 1% less than that for the entire labor force but the rate difference for men was about 4 to 5%.

George was a bit concerned that Monday night’s riots in Ferguson might have a secondary effect on Tuesday’s trading if the 2nd estimate of GDP growth for the 3rd quarter was below 3%. Yes, he should have been more focused on making turkeys out of construction paper for the Thanksgiving dinner. He and Mabel – well, mostly Mabel – had started the tradition when the kids, Robbie and Emily, were younger. Somehow they had continued the tradition after the kids had gone. George told Mabel that he would do it while they watched the season finale of Dancing With the Stars on Tuesday night. Somehow he felt like a kid saying he would do his homework later. Long marriages result from both partners doing stuff they don’t particularly like doing, George thought.

Tuesday morning’s report of GDP growth allayed George’s concerns. October’s initial estimate of growth had been 3.5%. This second estimate was higher, at 3.9%. The Case Shiller 20 city home price index showed a slight month-to-month increase, but the yearly increase in price was just about 5%, more in line with historical averages.

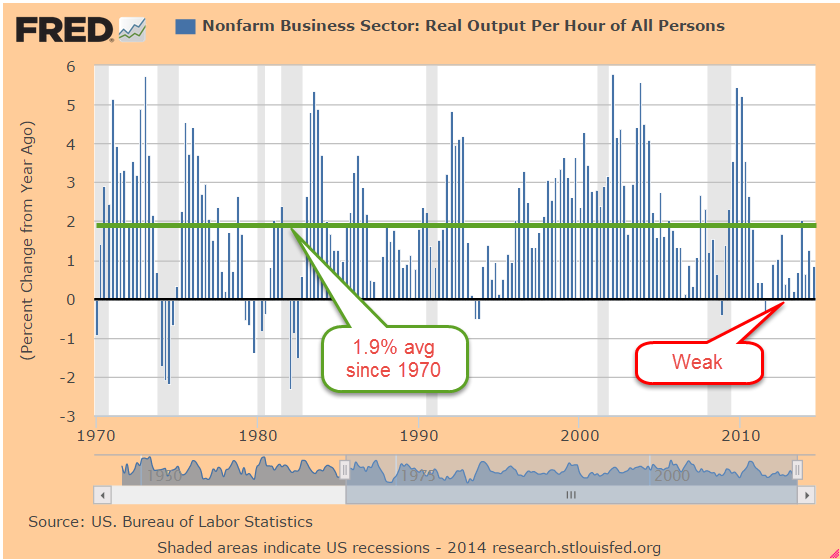

Corporate Profits for the 3rd quarter gained 3.8% year-over-year, slowing down from the 4.6% year-over-year growth in the 2nd quarter. Profit growth was ultimately driven by growth in productivity. Capital investments in technology had reaped the greater share of overall growth in the past decade or more. Labor’s share of growth had been particularly weak the past few years, far below the average of the past forty years.

A closer look at labor productivity gains in the past decade showed just how meager they were.

A work force unable to capture productivity growth could not command strong pay growth. Economists at the BLS

anticipated increasing overall output growth in this next decade but those projections were sullied by the lack of clarity regarding the causes for the slow growth in labor productivity of the past decade. Did the shift further away from manufacturing make gains harder to come by? Was there a limit to growth that could be achieved by better management, process design and innovation? Some blamed the exponential growth of the regulatory state, forcing businesses to devote an increasing number of hours on compliance and reporting. Others blamed the increase in social benefit programs for softening the competitive edge of American workers. Got a reason? Throw it in the hat, George thought. The market traded in a flat range for the day.

On Wednesday, George went to the bank to cash in the joint CD that he and Mabel had discussed the previous week. He was surprised to learn that the bank did not require the both of them to cash in a joint CD. Mabel was busy with Thanksgiving fixings so it was convenient that George could go alone to handle the matter. He picked up a certified bank check from one bank and drove over to the bank where they kept their checking account to deposit the money. He was also surprised to find that the bank did not credit the money to their account for a few days. “The other bank is just like 10 to 15 blocks away,” George told the teller. “Well, we have to guard against fraud,” the teller responded. “So it would have been better to have gotten cash?” George asked. “Well, yeh, but then I think you would have to fill out a form because it’s a large cash transaction,” the teller informed him. “You know, to say you got the money by legal means, that you’re not a drug dealer,” he went on, “but I’d have to ask my supervisor about that.”

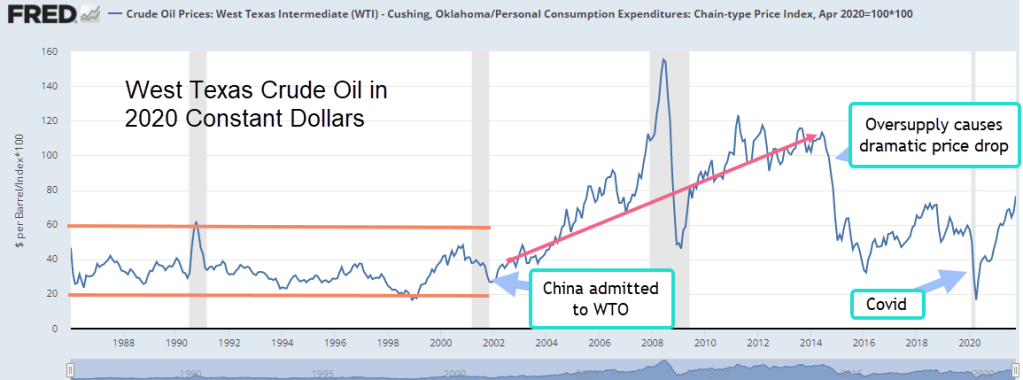

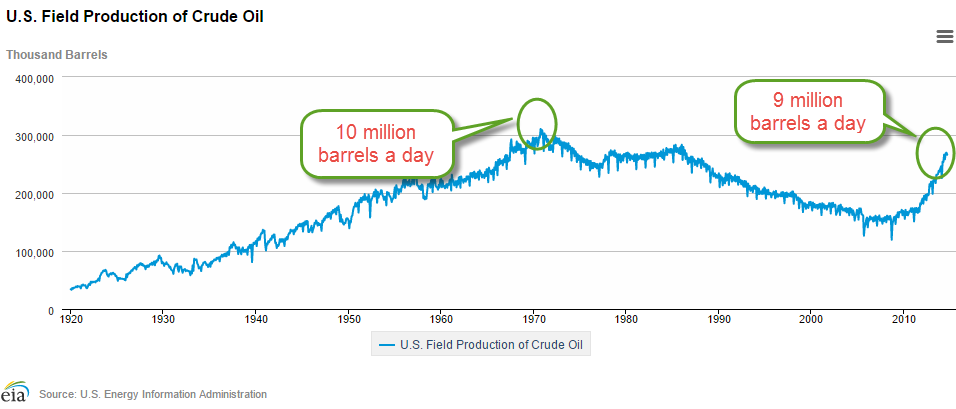

George was going to transfer the money that day to their brokerage but thought he should wait till Monday. George was tempted to buy maybe a 1000 shares of USO, the commodity ETF that tracked West Texas Intermediate Oil. OPEC was scheduled to meet Thanksgiving day to discuss the near term future of oil prices. They had dropped by about a third in the past year as increasing barrels of U.S. shale oil were added to the supply for a weakening global demand. U.S. oil production was now at 9 million barrels a day, the same level as the mid-1980s, and rising toward the record production of 10 million barrels in the early 1970s.

Poorer countries in OPEC who funded their government with the sale of oil, wanted to set production cuts to halt any further declines in oil prices. With their huge supply of oil and relatively inexpensive production costs, the Saudis were content to let the slide continue. On Tuesday, oil prices had dropped a few percent. But if the other members of OPEC prevailed and production cuts were announced, George reasoned, he could make a bundle of money in a short time by buying oil the day before. That was the speculative angel, or devil, on his shoulder whispering in his ear. His other angel simply asked, “Are we investing or gambling?” George gave in to his cautious angel. He could also lose a bunch of money really quickly if the Saudis prevailed.

Thanksgiving dinner was a relatively muted affair, unlike those of past years. Bob, George’s older brother, and his wife, Flo, had flown down to Cabo to work on an archaeological dig. The digging part of that “vacation” didn’t sound appealing to George but this archaeological club, or group, would put them up for 10 days in exchange for their labor and they would still have time for sun and surf. Bob had become fascinated with archaeology when he was about 60 years old and had pursued it with a passion since then.

Mabel, the oldest of five siblings, had taken on the Thanksgiving festivities. Two of her sisters lived in Colorado but only Susan, the youngest, came to dinner this week. Most unusual, George thought, that Charlie was the only child at the dinner this year. The talk at the dinner table turned to Ferguson. Robbie had read quite a lot of the testimony at the grand jury hearing and was full of facts. Charlie got bored as the adults chattered on during the meal. He saw a squirrel coming down the trunk of the tree in the front yard and asked George if he could have some peanuts to feed them. George had showed Charlie how to sit still on the back deck after putting peanuts out for the squirrels in the middle of the backyard. He was quite surprised that a child of that age could be motionless and silent for that long as they waited for the squirrels to scurry out from the bushes to snatch up a peanut in their wiry paws.

As the talk and opinions swirled around the table, Mabel was quiet, chewing methodically while listening attentively to the others. George had already had a few testy words with her earlier in the week so he knew how strong her opinions were. Robbie’s wife Gail all but accused her husband of being a racist because he did not understand that the facts of the case had been carefully cultivated in favor of the police officer. Robbie asked his mom for some affirmation. Mabel finished a bite of sweet potato.

“About fifteen years ago, I stayed a bit late after school, finishing up some paperwork,” she said to Robbie, then turned to the others around the table. “It was late October, maybe early November. The sun had already set. There were only a few cars left in the parking lot. There was one of those parking lot lights, the high ones like street lights, near my car but it would go on for a few seconds, then go off for about a minute. As I walked to my car in the semi-darkness, I noticed a figure walking to me from my right as though to intersect me as I got to my car. A second glance up and I saw he was wearing one of those,” she paused, “hoodies, I think they’re called. As he got closer, maybe twenty feet away, I realized that I couldn’t see his face, that it was a black man in a hoodie. My heart instantly started flippity flopping as I realized that I was going to be attacked.”

Mabel had everyone’s attention, a difficult thing to do in an family that was not reluctant to share their opinions. “There was no one else in the parking lot that I could call out to for help,” she continued in a purposeful voice. “I hurried my step, reached into my bag, fumbling for the car keys as I approached the car. I didn’t want to look panicked, fearing I don’t know what. Maybe that my panic would provoke the attacker. As I reached out my arm to unlock the car, the man’s voice broke the darkness. All I heard was ‘Hey’ and I turned and I yelled back ‘Aaaaahhhhh,’ grunting it out like some Kung-Fu movie. “Mabel? Is that you? I didn’t mean to startle you,” the voice from the hoodie said. He brushed back the hood of his parka and I could see that it was James, the biology teacher.

He was so apologetic and I pretended that I had not noticed him until just that minute. ‘My battery’s dead and I was wondering if you have some cables, could give me a jump,’ he explained to me. ‘I was going to call AAA and then I saw someone come out of the school entrance and I thought it might be you but I wasn’t sure,’ he went on. I had cables in the trunk, but I was so upset that I lied and told him no, I didn’t have any. He thanked me and went back across the parking lot to his car.” Mabel took a quick sip of water from her glass. George had never heard this story. After 35 years of marriage, that rarely occurred.

“I started up the car, then sat there crying,” she continued, her lips tense. “It’s as though my ideals, my view of myself, was a cloak that I had worn and then, that night, I looked in the mirror without my cloak on. I wasn’t racist in spirit,” she paused, searching for the words to complete the thought, “or intention, but I realized that I was a racist in perception. Racism is embedded in our culture, in me, whether I like it or not.”

She stopped and there was silence around the dinner table, a rare event at a Liscomb family gathering. Robbie, sitting close by his mother, reached across the table to grasp his mother’s hand. From the far end of the table, George was struck by her – what would he call it? Her forthrightness. She had an ability he lacked, and perhaps that’s why the seeing of it in her gave him a sense of admiration. The moment snapped like a crisp carrot as the front door swung open and Charlie burst through the doorway. “The squirrel was eating a peanut this far from me!” he yelled excitedly and spread wide his arms.

On Friday, George learned that the Saudis had prevailed at the OPEC meeting. By the end of the day, USO had dropped more than 8%. We bear the fruits of what we do and don’t do, George reminded himself, then wondered if that was a line from Shakespeare or maybe Leonard Cohen?

While the stock market stayed relatively quiet during the week, ten year bond prices continued to gather strength. Stocks and bonds tended to move opposite each other in a dance of risk and return. When they both gained in strength, something had to give. The last time they met at this strong level was at the end of August, when bonds faltered first, falling about 5% over two weeks while the SP500 remained fairly stable. In mid-September they flipped. Bonds rallied up 8-9% as stocks fell the same amount. Then stocks rallied to all time highs in the past four or five weeks but bond prices had not fallen more than a few percent. George resolved to watch this dance during the following week. It was the first week of the month, filled with a number of reports including the employment report that could renew or drain confidence in the stock market.