August 9, 2015

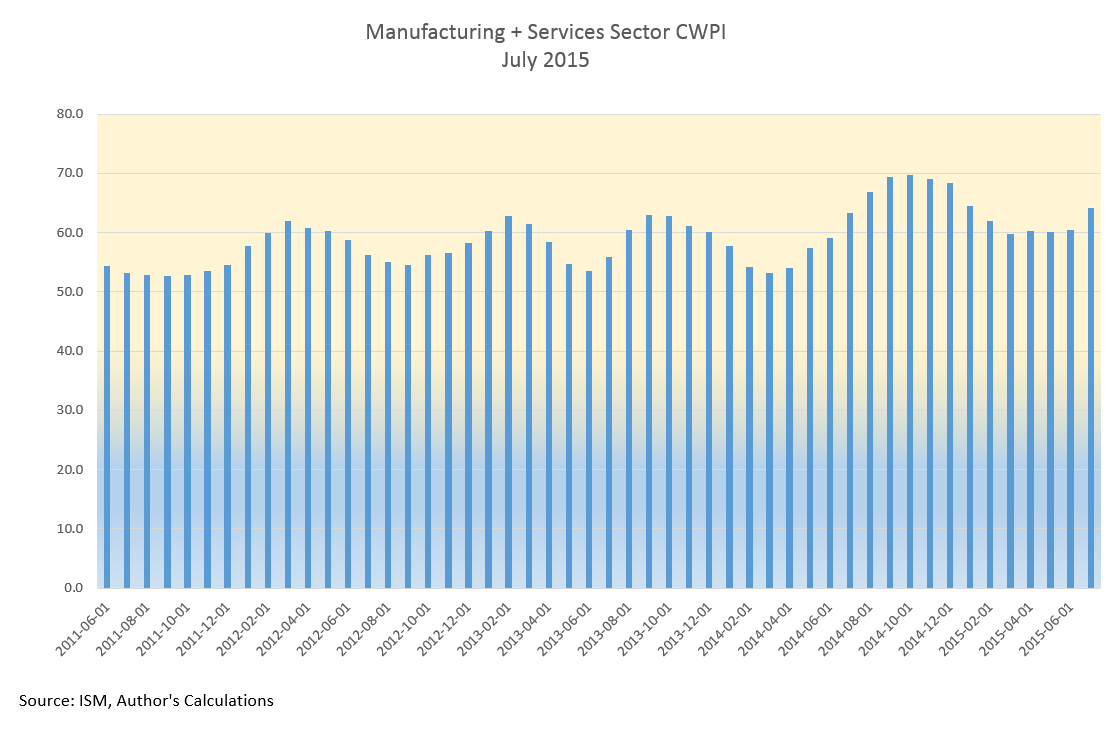

As we all sat around the Thanksgiving table last November, the SP500 was about the same level as it closed this week. Investors have pulled off the road and are checking their maps to the future. After forming a base of good growth in the past few months, July’s CWPI reading surged upwards.

Despite years of purchasing managers (PMI) surveys showing expanding economic activity, GDP growth remains lackluster. Every summer, in response to more complete information or changes to statistical methodologies, the Bureau of Economic Analysis (BEA) revises GDP figures for the most recent years. A week ago the BEA revised real annual GDP growth rates for the years 2011 – 2014 from 2.3% to 2.0%. “From 2011 to 2014, real GDP increased at an average annual rate of 2.0 percent; in the previously published estimates, real GDP had increased at an average annual rate of 2.3 percent.”

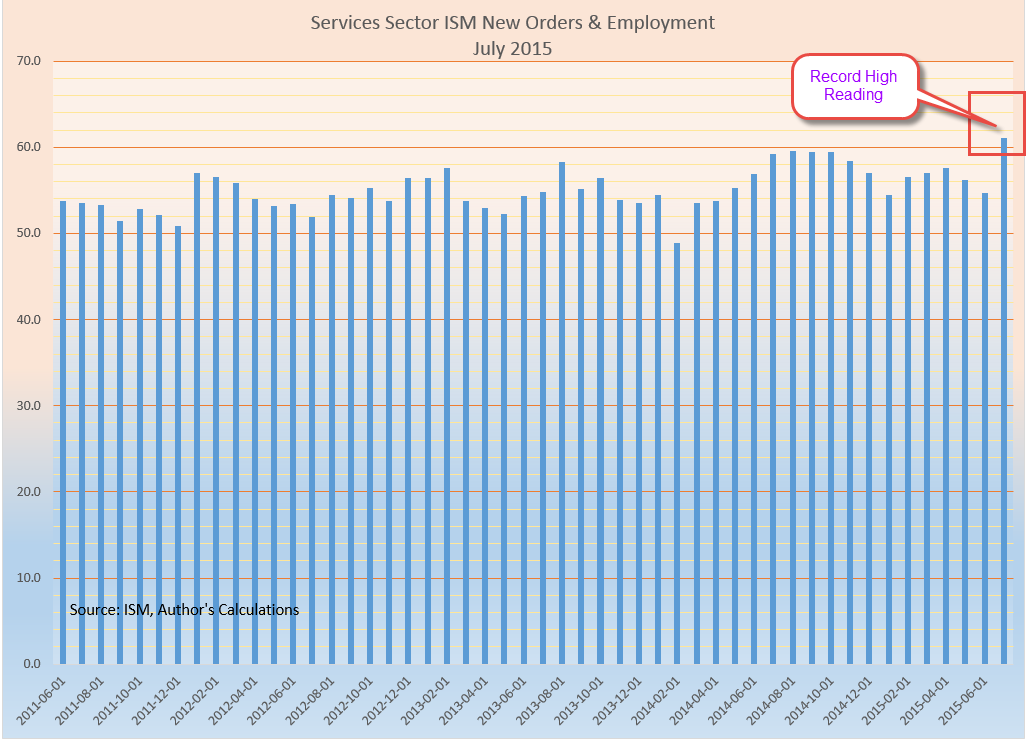

A composite of new orders and rising employment in the service sectors showed its strongest reading since the series began in 1997. The ISM reading bested the strong survey sentiments of last summer. We can assume that the PMI survey is not capturing some of the weakness in the economy.

This level of robust growth should put upward pressure on prices but inflation is below the Federal Reserve’s benchmark of 2%. Energy and food prices can be volatile so the Fed uses what is called the “core” rate to get a feel for the underlying inflationary pressures in the economy.

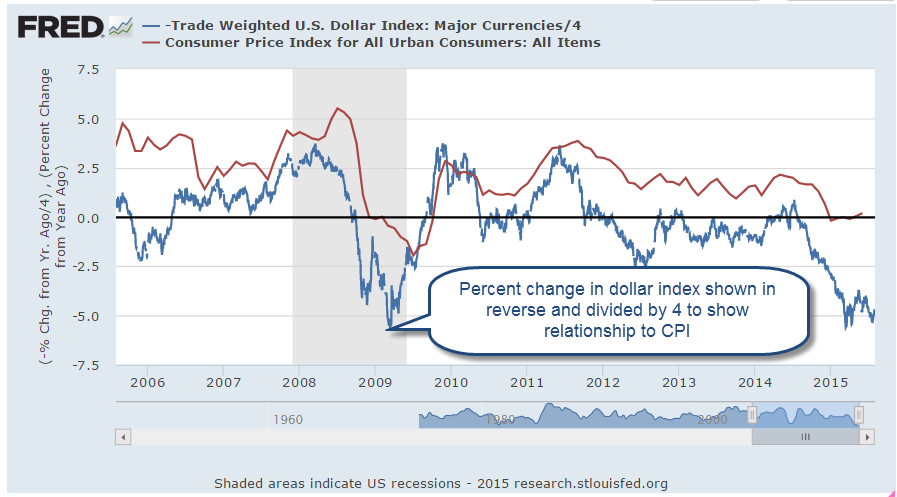

The stronger U.S. dollar helps keep inflation in check. There is less demand from other countries for our goods and the goods that we import from other countries are less expensive to Americans. . Because the U.S. imports so much more than it exports, the lower cost of imported goods dampens inflation. In effect, we “export” our inflation to the rest of the world.

When the economy is really, really good or very, very bad we set certain thresholds and compare the current period to those benchmarks. When the financial crisis exploded in late 2008, the world fled to the perceived safety of the dollar in the absence of a exchange commodity of value like gold. Because oil is traded in U.S. dollars and the U.S. is a stable and productive economy and trading partner, the U.S. dollar has become the world’s reserve currency. The conventional way of measuring the strength of a currency like the dollar has been to compile an index of exchange rates with the currencies of our major trading partners. This index, known as a trade weighted index, does not show a historically strong U.S. dollar. In fact, since 2005, the dollar has been extremely weak using this methodology and only recently has the dollar risen up from these particularly weak levels.

As I mentioned earlier, a strong dollar helps mitigate inflation pressures; i.e. they are negatively correlated. When the dollar moves up, inflation moves down. To show the loose relationship between the dollar index and a common measure of inflation, the CPI, I have plotted the yearly percent change in the dollar (divided by 4) and the CPI, then reversed the value of the dollar index. As we can see in the graph below, the strengthening dollar is countering inflation.

What does this mean for investors? The relatively strong economy allows the Fed to abandon the zero interest rate policy (ZIRP) of the past seven years and move rates upward. A zero interest rate takes away a powerful tool that the Fed can employ during economic weakness: to stimulate the economy by lowering interest rates.

The strong dollar, however, makes Fed policy makers cautious. Higher interest rates will make the dollar more appealing to foreign investors which will further strengthen the dollar and continue to put deflationary pressures on the economy. The Fed is more likely to take a slow and measured approach. Earlier this year, estimates of the Effective Federal Funds Rate at the end of 2015 were about 1%. Now they are 1/2% – 3/4%. In anticipation of higher interest rates, the price of long term Treasury bonds (TLT) had fallen about 12% in the spring. They have regained about 7% since mid-July.

DBC is a large commodity ETF that tracks a variety of commodities but has about half of its holdings in petroleum products. It has lost about 15% since May and 40% in a year. It is currently trading way below its low price point during the financial crisis in early 2009. A few commodity hedge funds have recently closed and given what money they have left back to investors. Perhaps this is the final capitulation? As I wrote last week, there is a change in the air.

*************************

Labor Report

Strong job gains again this month but labor participation remains low. A key indicator of the health of the work force are the job gains in the core work force, those aged 25 – 54.

While showing some decline, there are too many people who are working part time because they can’t find a full time job. Six years after the official end of the recession in the summer of 2009, this segment of the work force is at about the same level.

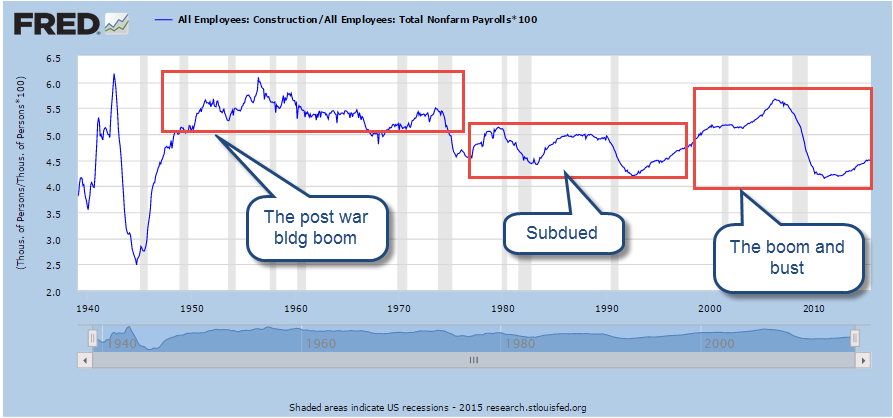

In some parts of the country job gains in Construction have been strong. Overall, not so much. As a percent of the work force, construction jobs are relatively low. In the chart below I have shown three distinct phases in this sector since the end of World War 2. Extremes are most disruptive to an economy whether they be up or down. Note the relatively narrow bands in the post war building boom and the two decades from 1975 through 1994. Compare that to the wider “data box” of the past two decades.

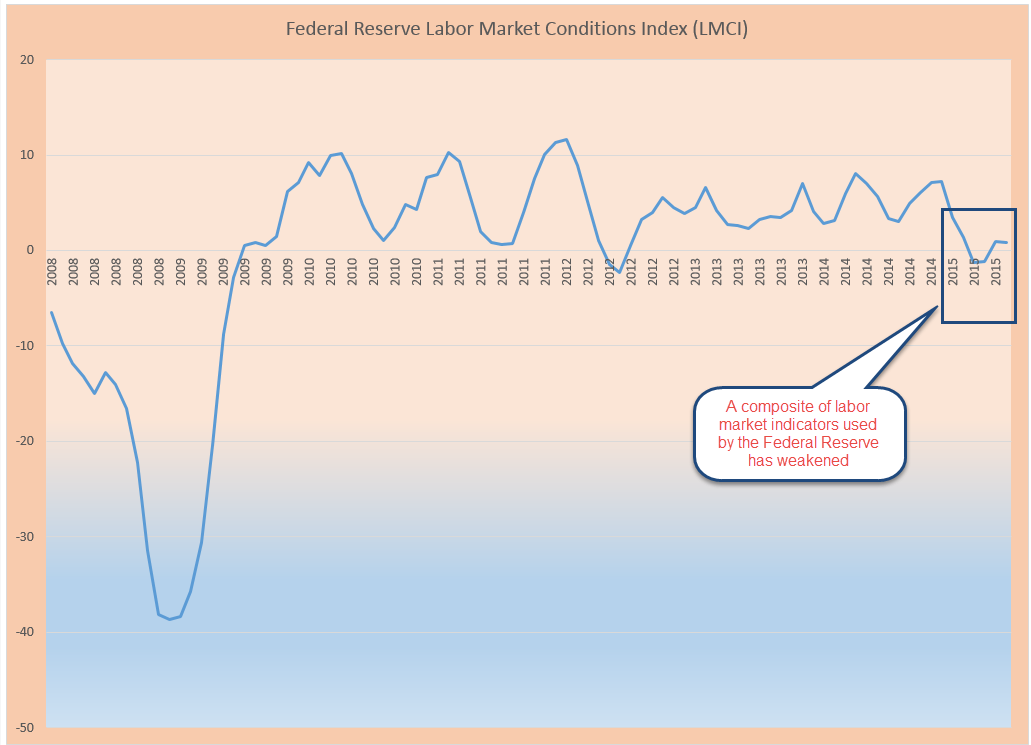

For several months the headline job gains have averaged about 225,000 each month. The employment component in the ISM Purchasing Managers’ Index (on which the CWPI above is based) is particularly robust. New unemployment claims are low and the number of people confident enough to quit their jobs is healthy. The Federal Reserve compiles an index of many factors that affect the labor market called the Labor Market Conditions Index (LMCI). They have not updated the data for July yet but it is curiously low and gives more evidence that the Fed will be cautious in raising rates.