Each month the Federal Reserve in Philadephia compiles a Coincident Index (CI) for each state, then combines state information to get a picture of the U.S. economy. The Federal Reserve at St. Louis publishes this composite which provides an overall economic picture for the nation. (Click to view larger graphs in separate tab)

The graph shows clearly why this is the Mother of All Recessions.

These coincident indexes rely primarily on labor and production statistics and a decline in the index correlates pretty closely with the official start of recessions as set forth by the National Bureau of Economic Research (NBER). The CI gives a more accurate picture of the underlying economic strength of the country. The NBER calls an end to a recession long before it feels like the end of a recession, leading some economists and market watchers to scoff lightly when the NBER pronounces that a recession is over as it did in the middle of 2009.

When is a recession really over? In my view, it is when the index reaches the level it was at when the recession began. Using this criteria as a guide, the relatively shallow recessions of the early 90s and 2000s were longer lived than the official NBER dates. Those of us who lived through them can concur that the CI gives the more accurate picture.

Those earlier recessions look like mere wrinkles compared to this last recession and using my criteria, we are still in recession. The millions of unemployed would confirm that.

Combining some of the same labor and production data, together with fear and greed, the stock market tries to anticpate the earnings of publicly traded companies. Since earnings are based largely on the strength of economic activity in this country and abroad, the stock market is a divination of sorts. Like augurers of ancient Rome, sometimes they get it right, sometimes they don’t.

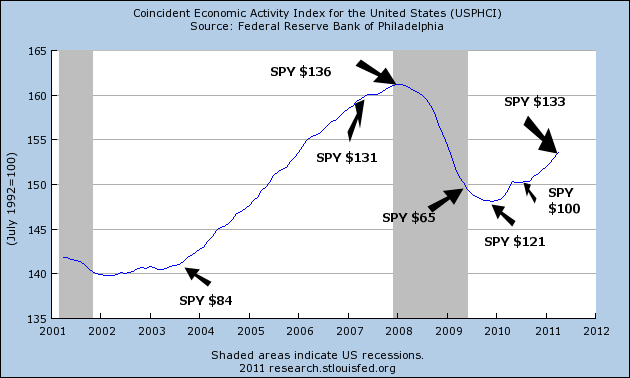

Below is a chart of the CI following the recession of the early 90s to the height of the “dot com” era in the early part of 2000. The growth of the personal computer and the advent of the internet helped usher in a decade like the 1920s when the telephone and telegraph prompted both investment and speculation. Below is a chart of the CI with a few price flags of a popular ETF, SPY, that mimics the movement of the S&P500 index.

With the rise in economic activity and the stock market, we began to take on ever more debt during that period, continuing and accelerating a trend that started in the early 1980s. In anticipation of a continuing boom in economic activity, we borrowed against the rising equity in our homes and in our stocks. That borrowing fueled ever more economic activity as we remodeled our homes, bought new cars and took more expensive vacations.

As the froth of the dot com era blew away, overall economic activity was still rising and so was household debt. The stock market may have experienced a correction but the American family was still riding the rocket of rising home prices. In his campaign, George W. Bush had warned of an impending recession and soon after he took office, the recession began. The recession officially lasted 8 months, about average, but was exacerbated by the 9/11 disaster. The true length of that recession is marked more clearly by the CI, which shows how truly weak the recovery was.

On the whole, Republicans believe that government can boost the economy by taking less in taxes out of the private sector. Democrats believe that government can boost the economy by more government spending. With a slight majority in both the House and Senate, Republicans and Democrats crafted an elegant solution – tax less and spend more. Never mind that such a solution is a long term recipe for economic disaster.

By the beginning of 2004, the CI had risen to the level of early 2001, finally ending an almost 3 year recessionary period. The stock market was beginning a strong upward move. House prices were still on the rise and accelerating, prompting homeowners to trade up to bigger houses and renters to become homeowners. It was a period of Buy, buy, buy and Borrow, borrow, borrow.

In a November 2005 research paper by the St. Louis Fed, the authors write, “Real U.S. house prices, on average, have appreciated by 6 percent annually since 2000, a historically high rate when compared with the 2.7 percent annual rate between 1975 and 1999.” But, the authors concluded, “if bubble conditions do exist, they appear only on the two coasts and in Michigan.” In the same month this research paper was published, the peak of the housing boom occurred, using the Case Shiller index as an indicator.

Fueled by borrowing and a rising stock market, economic activity continued to climb until it peaked in December 2007 – January 2008. The stock market had stumbled in August 2007 as the unemployment rate edged up toward 5% (the good old days!) and softness in the housing market became more pronounced.

An investor who simply took a cue from the rise and fall of the CI over the past 20 years would have done very well. The market anticipates an upturn or downturn in economic activity just as the CI is turning up or down EXCEPT for 2009. What did the market respond to when it turned up in the spring of 2009? It was not economic activity because activity was still falling and showed no signs of bottoming. The market was hoping that massive government spending would spur increased economic activity. As stimulus spending flowed through the economy throughout 2009, economic activity did pick up but stalled in the spring of 2010 as the greatest part of the stimulus had already been spent and the underlying weakness of the economy became apparent. Enter the Federal Reserve in September with another round of stimulus via its QE2 program of Treasury bond purchases, which again spurred an uptick in activity and the stock market.

As the CI shows, the recessionary period isn’t over. Over the past 3 years, we have shifted household debt

and bank debt

to the federal government – that’s you, me, our kids and grandkids.

It is going to be a bumpy ride. The CI has proven to be a fairly reliable road map.