Earlier this past week there were rumors that, due to the government shut down, the Bureau of Labor Statistics (BLS) might not release the monthly employment report on Friday. The employment report is probably the foremost key indicator that guides stock and bond market action as well as a prime metric used by the Federal Reserve in the determination of future monetary policy. On Thursday, the BLS confirmed that they would not release the report, which prompted a drop in the stock market, followed by an almost equal rise over the next day.

On Wednesday, ADP released a tepid 166,000 estimate of net job gains for September accompanied by a downward revision of their August estimate. On Thursday, the weekly report of new unemployment claims held no surprise. Traders probably figured that they had enough information to guesstimate the BLS number of net job gains – tepid growth a bit above the 150,000 needed to keep up with population growth. In short, there was less likelihood that the Federal Reserve would be tapering their QE program before the end of the year.

So this is a good opportunity to take a look at some historical employment trends. Measuring wage growth and inflation adjustments to wages is a complex task, far more complex than the gentle reader wants to delve into. Labor economists crunch a lot of regional employment data gathered by the BLS. Whenever there is a wealth of data, there is also a wealth of ways to treat that data, which data to focus on, etc. Some economists focus on median compensation. The median represents the middle, i.e. 50% of workers make more than the median, 50% make less.

In a 2011 paper published by the Economic Policy Institute (EPI), author Lawrence Mishel states “Between 1973 and 2011, the median worker’s real hourly compensation (which includes wages and benefits) rose just 10.7 percent.”

“Real” means inflation adjusted but there are different methods used to calculate inflation. One method, the Consumer Price Index, or CPI, has been changed over the years, making it difficult to make comparisons of data.

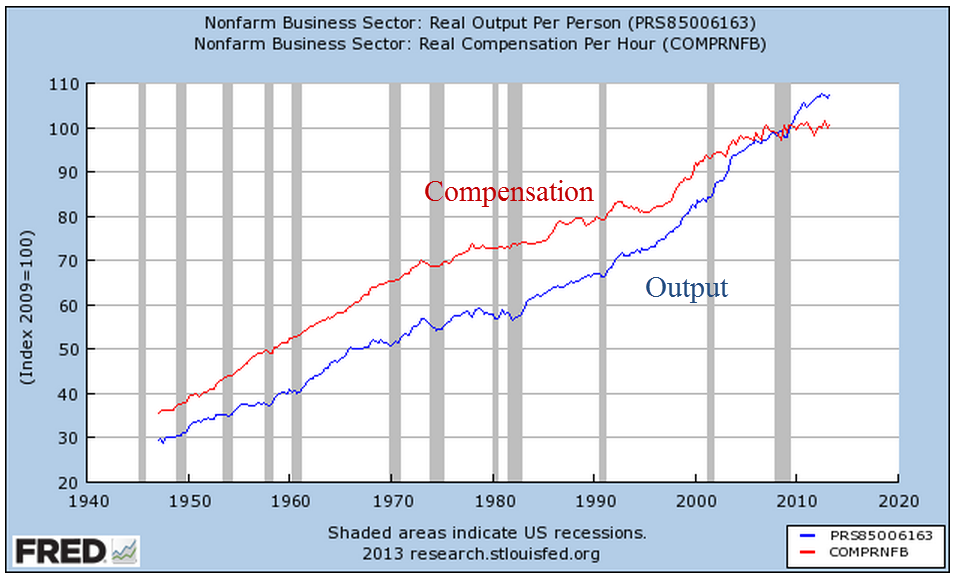

For a longer term perspective into the controversy over measurement, let’s turn to a graph of real output and total compensation per hour worked for the business sector. Here we see a narrowing between compensation and output until output crosses above compensation in the mid-2000s.

The flattening of compensation growth is shown when we focus on the past twenty years.

But the hourly data seemingly contradicts the claim that there has been only an 11% increase in real compensation over the past forty years. Looks like the total compensation of all workers has risen about 40% or more in the past forty years. How can the median growth be so far below the total? To understand that, a reader would have to examine the data sources behind the claim. We might find that median weekly, not hourly, compensation has risen only 11%. This could be due to more part time workers, or the rising percentage of women in the labor force who generally work fewer hours than men. What we do know is that a competent economist can find or crunch the data to prove his or her point.

The ability to work empirical magic with data often leads to contradictory claims by noteworthy economists. The contentiousness of the discussion among economists baffles the intelligent reader.

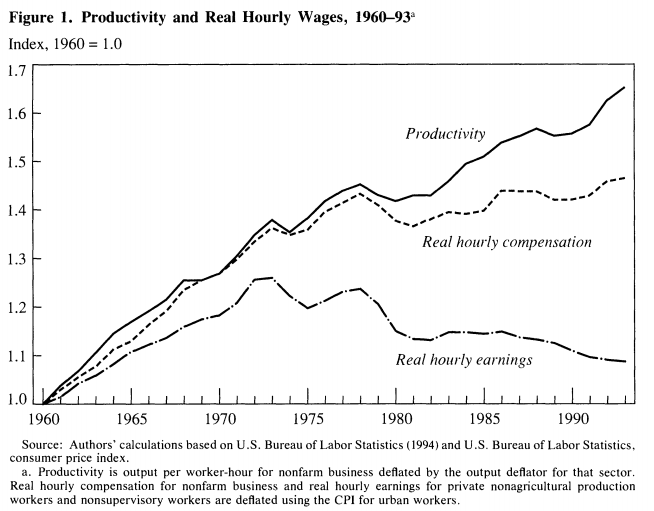

Let’s return to that bugaboo mentioned earlier: measuring inflation. Twenty years ago, economists Brian Bosworth and George Perry noted the trending gap between output and productivity: “In an economy where real wage growth has paralleled the rise in productivity over the long run, this apparent divergence implies that the benefits of increased productivity have not been distributed in the expected way over the past two decades.” A chart from their paper illustrates the trend.

A notable trend in the numbers is the steep rise of employee taxes and benefits, or non-wage employer costs. Economists or politicians sometimes point to the decline in the real hourly wage over the past forty years, without bothering to note the growing non-wage costs of employment, a convenient omission.

Bosworth and Perry document problems and changes in measuring inflation in both consumption and output but noted that “the prices that workers pay as consumers have been rising significantly more rapidly than the prices of the products they produce.” Further analysis by the authors shows that the wage growth in that twenty year period 1973 – 1993 did not flatten till after 1983. They conclude that the major reason for the divergence is the difference between how inflation was measured before and after 1983. The authors recommended the use of a Personal Consumption Expenditure (PCE) deflator instead of the CPI, which overstates inflation relative to output.

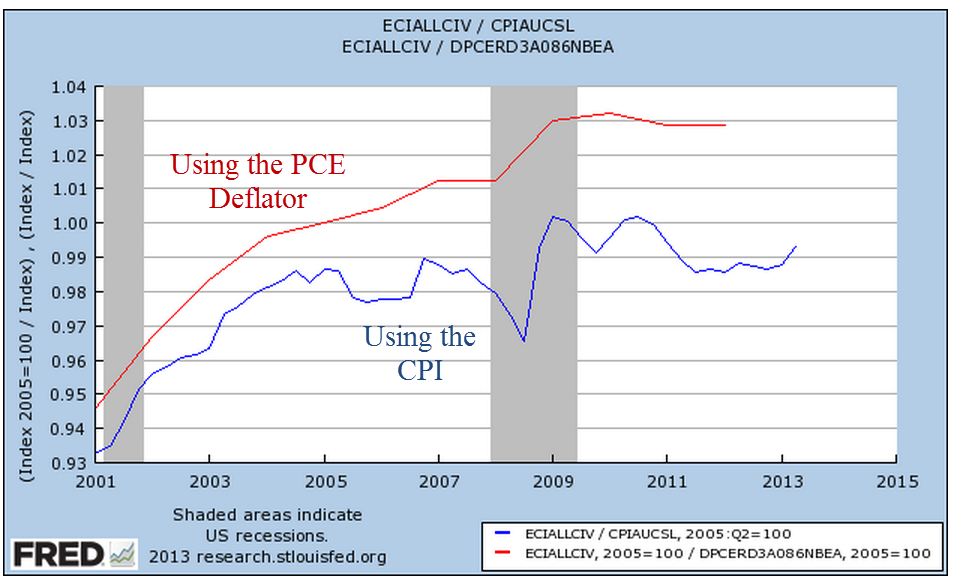

Let’s look at wage growth over the past twelve years using two methods to see the difference. The BLS calculates real wage growth using the CPI-U inflation index (Source). Here is a graph from their data.

Now let’s use the PCE deflator to get a slightly different picture of the same Employment Cost Index.

Now let’s compare the two.

They tell two different stories. Using the CPI inflation adjustment, the blue line, I could tell a story that wage growth has stagnated over the past ten years. Using the PCE inflation adjustment, I could tell a story that wage growth has stagnated since the financial crisis.

Now imagine a politician who wants to bash the policies of former President George Bush and exalt the policies of the current administration. That politician would use the blue line to tell the story of how the Bush Administration undercut the wages of American workers and that this led to the worst recession since the Great Depression.

On the other hand, if a politician wanted to criticize the Obama administration, she would point to the red line. Worker’s wages grew during the Bush years. Since Obama took office, wages have stagnated, indicating that Obama’s policies are hurting American workers.

Thus a dense and complicated argument on how to measure inflation becomes a talking point for a politician. Even worse, noteworthy and popular economists who understand the difficulties of measuring both employment and inflation choose one line or the other to tell a simple story based on their own bias.

During this ongoing government shut down, we will hear a lot of spin and invective. The profusion of TV, radio and internet media sources ensures that anyone can choose exactly – to a ‘T’ – the version of reality that they want to hear. Of course, our sources and opinions are unbiased and perfectly reasonable. But can you believe what the other side is saying? Boy, are they crazy!