January 19th, 2014

A strong retail report for December and an improvement in sentiment among small business owners buoyed the market at the start of the week. Both reports continue a trend that indicates a healthy economy: results are at at the upper bound or above expectations.

The latest report of jobless claims at 325,000 pulled the 4 week average further down away from the psychological mark of 350,000. This is sure to reassure short to mid term traders. The weak BLS employment report released a week ago may have just been an anomaly. Other employment indicators, as well as retail sales and business production simply do not confirm the headline numbers from the BLS.

The Consumer Price Index for December showed a mild 1.5% year over year increase and will reassure the Fed that its stimulus program poses little danger of igniting inflation.

The National Assn of Homebuilders reported continued strong growth in their Housing Market Index.

******************************

Featured on one of the blogs that I link to is a chart of the annual returns of the SP500. Double digit gains in the index, like the one we had last year, are rather common, occurring about 40% of the time. A reassuring takeaway for the longer term investor is that the market goes up in 75% of the years for the past eighty years.

******************************

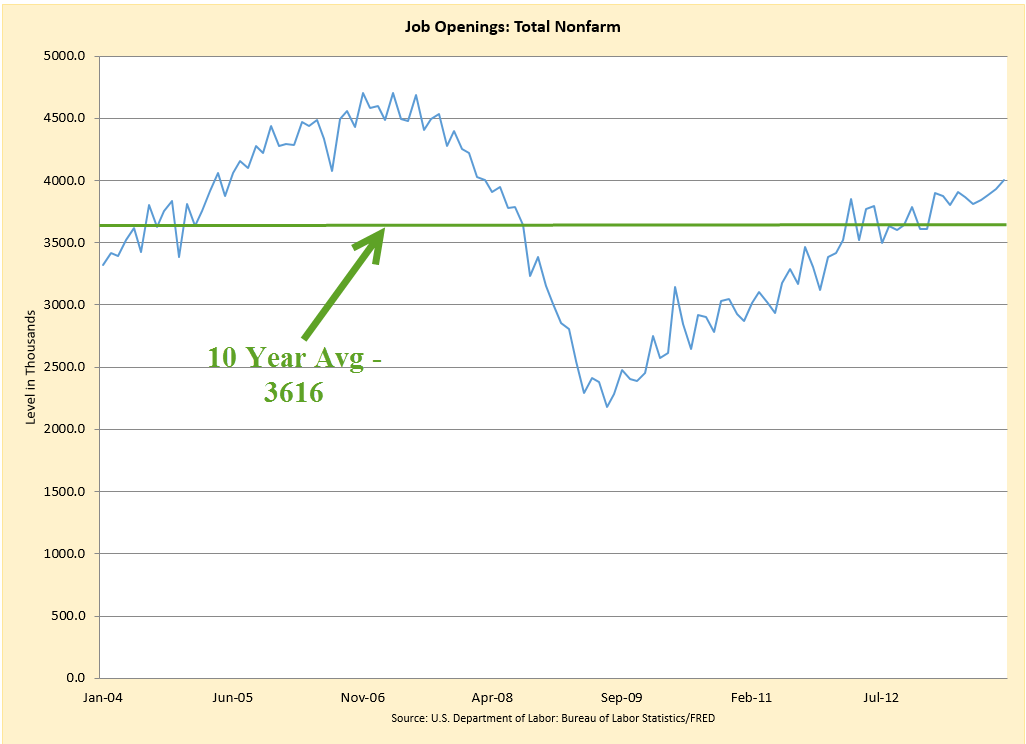

The number of unfilled job openings in November was the highest since March of 2008, indicating continuing strengthening in the labor market. Job openings have been above the ten year average for over a year now.

The number of people who voluntarily quit their jobs continues to climb over the past year. Employees quit when they feel more confident about job prospects. While this metric has been improving, it is only at the lowest levels of the past decade.

******************************

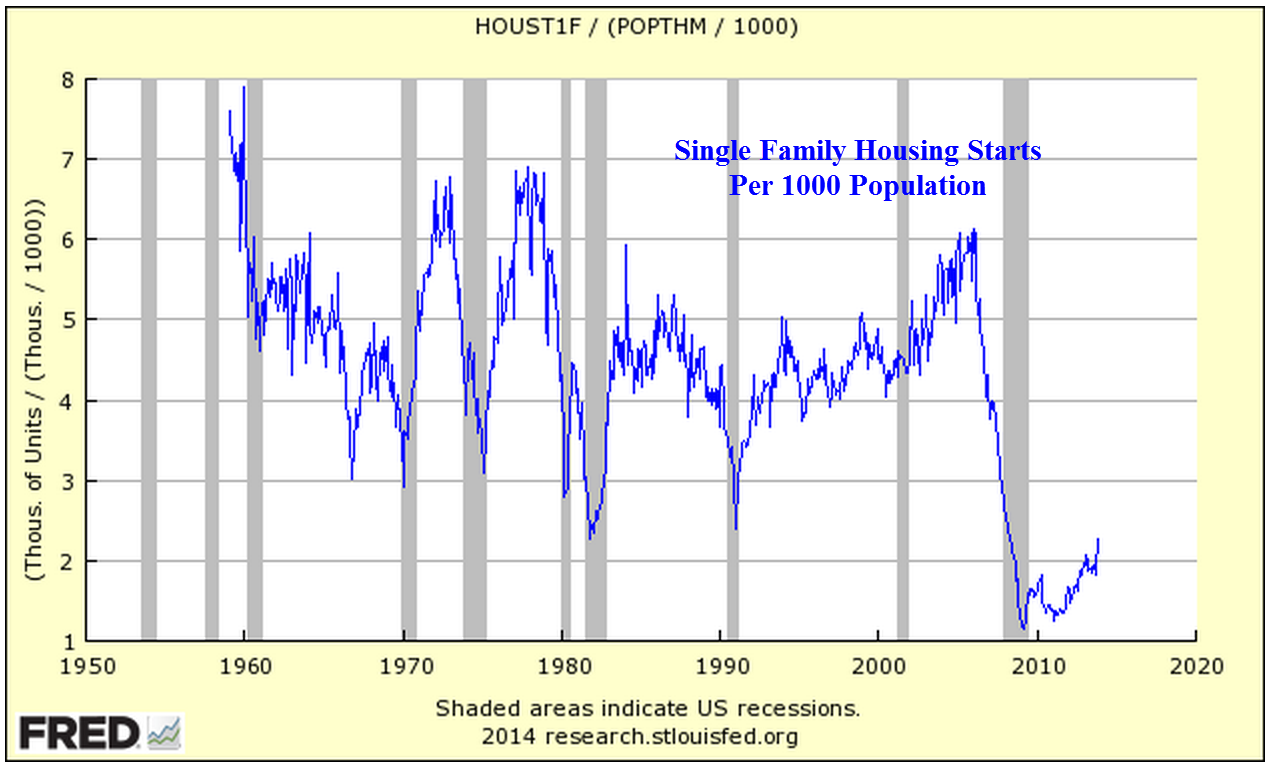

Housing starts declined slightly in December to a million but is still growing from the lows of the bust.

Let’s get a bit of perspective. There is a decided shift downward from the post war building boom. Below is a graph of housing starts adjusted for population growth.

Adjusted for population growth, the multi-family component of housing starts has reached the normal levels of the past two decades. This is the more stable component of housing starts.

Starts of single family homes have not yet reached the lows of past recessions. The words “improvement” and “recovery” should be viewed in the context of these abysmal lows.

*******************************

The Consumer Price Index (CPI) for December showed a year over year increase of 1.5%. I believe this understates current inflationary pressures on consumers but it is the official rate, one that the Federal Reserve will use to guide policy. The low rate will help allay fears that continuing stimulus will spur inflation in the near term.

*******************************

Stock prices will be driven largely by earnings reports at this time. About 10% of SP500 companies have reported this past week, too few to get a solid feel yet for the past quarter. 62% of companies have beat expectations, a bit less than the more normal 70%. The market is largely trading sideways as it digests both the past quarter’s results and the forward guidance that companies give when they report. IBM, Johnson and Johnson, and Verizon kick off this holiday shortened week when they report earnings on Tuesday. McDonald’s, Microsoft, Proctor and Gamble, and Netflix are due to report this week as well. There don’t appear to be any significant market moving economic reports coming up this week. Existing Home Sales on Thursday might have some minor impact and traders will be watching the continuing trend in new unemployment claims.