May 17, 2015

Life expectancy (LE) is often measured at birth (CDC). The great increases in LE during the 20th century can be largely attributed to rapidly declining childhood mortality rates. Advancements in medical practice have certainly played an important role but clean drinking water and modern sanitation disposal and treatment have had the most effect. Improvements in life expectancy at age 65 have been much less dramatic.

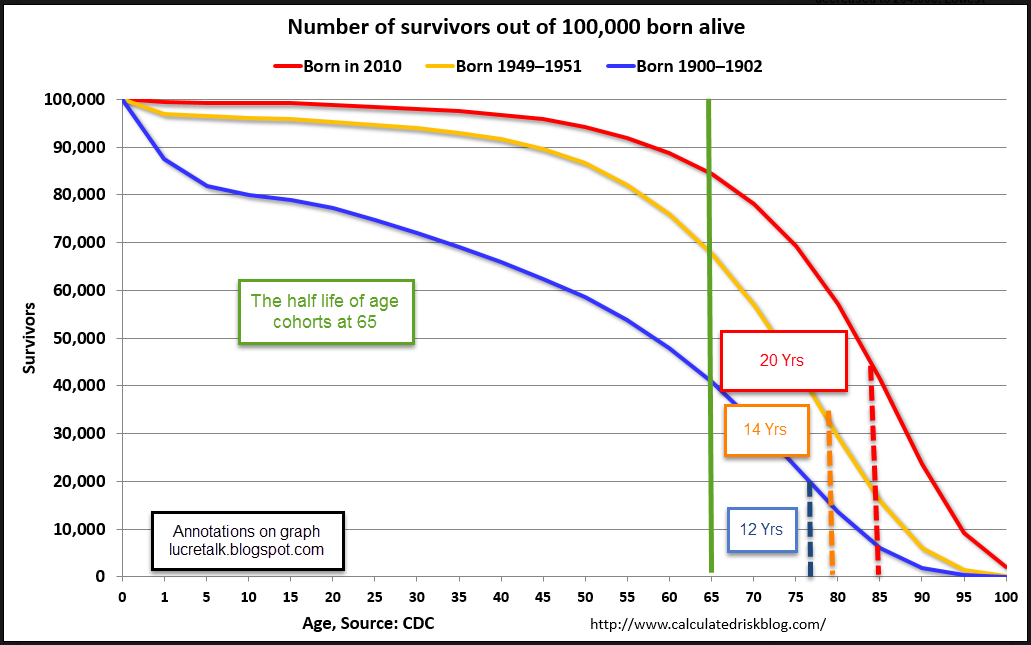

Last week’s Calculated Risk blog presented LE with more clarity – by graphing age cohorts, a group of people born in a particular year or range of years. If 100 people were born in 1950 – an age cohort – how many of that cohort were alive in 2000? The chart convincingly illuminates several problems with Social Security funding and payouts in the future.

One of the cohorts shown in the first graph (blue line) are those born in the years 1900 – 1902. This age group was in their mid–thirties when Social Security was enacted. Many funded the Social Security system through their working years but only 40% reached the age of 65 to become eligible for Social Security. Just over 70% of the early Boomer cohort (gold line) born in 1950 is still alive this year, their 65th birthday. More than 85% of the people born in 2010 are expected to reach 65.

When the Social Security act was written, what if the language of the act reflected life expectancies at that time? Instead of setting a specific retirement age, it could have specified that every five years, for example, Congress would revise the retirement age based on the half life of an age cohort, that age when half of a generation is alive and half is dead.

For the 1900-1902 cohort, the retirement age would have been 59. For early Boomers, those who just turned 65, retirement would still be almost a decade away, at 74. The 2010 generation could expect to retire at around age 83.

As important as the age of eligibility is the number of years that retirees collect Social Security. What is the half life of an age cohort once they have reached 65? If 50 out of 100 of a cohort are alive at age 65, how many years before only 25 are alive? I’ll call this the age-65 half life. I marked up the chart at Calculated Risk to show the current and projected increases in age for these retirees who will be funded by Social Security.

Although life expectancy at birth has increased dramatically, the half life of people who manage to reach the age of 65 shows much slower increases. The difference between the age-65 half lives of the 1900 and 1950 cohorts is projected to grow only slightly, from 12 to 14 years. That’s just a two year increase for two generations born 50 years apart. The growth of that half life is projected to quicken for the 2010 generation but we should be suspicious of estimates eighty years in the future.

Of the 76 million boomers born, 65 million were still alive in 2012 (Source) Even though the age-65 half life of people had changed by only two years, that is a lot of people eligible for Social Security payments. Politicians find it difficult to discuss changes in this program, the “third rail” of politics. People who have paid taxes into the program during a lifetime of work feel that they have earned the payments they receive in retirement. Any changes have to be done incrementally, like raising the temperature of a pot of water so that the frog doesn’t jump out. Voters will probably punish lawmakers who suggest wholesale changes. Former Senator Rick Santorum discovered that brutal truth when he endorsed former President Bush’s proposal to privatize Social Security. Bush was a lame duck President with little to lose but quickly withdrew the idea in response to the angry response to the idea. Santorum lost his seat.

Congress might initiate some rules based approach like the half life criteria to setting the retirement age for future decades. This would help avoid political repercussions for any changes to Social Security. If Congress set the retirement age criteria at 60% instead of 50% (half life), the retirement age would be 69 for this generation, just two years more than current law for the late Boomers.