July 12, 2015

In the past few weeks, I have looked at savings and investment as forms of spending shifted in time. Now let’s examine the idea of income. We earn money, spend most of it, and hopefully save a little of it.

In the 1930s John Maynard Keynes proposed an income expenditure model to explain business cycles. (More here) Although Keynes’ model was mathematically simple by today’s standards, it showed an interlocking relationship between employment, interest rates and money. Keynes popularized his ideas in lectures, debates and magazine articles. Although he died shortly after World War 2, financial institutions and economic policies still bear his mark. It was he who first proposed and then co-developed the framework for the International Monetary Fund (IMF) and World Bank.

One of Keynes many seminal insights was that one person’s income is another person’s spending. If I decide to save $5 by not buying a latte at the neighborhood coffee shop, I am in effect putting my $5 in a savings account at my local bank. But the coffee shop owner has $5 less in income. $5 less in income is $5 less profit, keeping all else the same. The owner of the coffee shop must go to the local bank and take $5 out of their savings account to make up for the lost income. There is no net savings when a person decides to not spend money and we see the relationship between savings and profit; namely, savings = profit.

We are now ready to develop that insight of Keynes, that income = spending. As we discussed in previous weeks, the amount that we don’t spend on current consumption is savings. Savings = spending, either yesterday’s spending, i.e. an investment in someone’s debt, or tomorrow’s spending, i.e. an investment in someone’s future profits, or savings. When we spend for tomorrow, we are effectively moving our savings into the future. Likewise, when we spend for yesterday, we move our savings into the past to replace the savings that someone else did not have at the time they borrowed the money.

All of these categories – income, spending, saving, investment – are all forms of spending shifted in time. Next week we’ll look at the GDP accounting identity and the government component of that equation.

*****************************

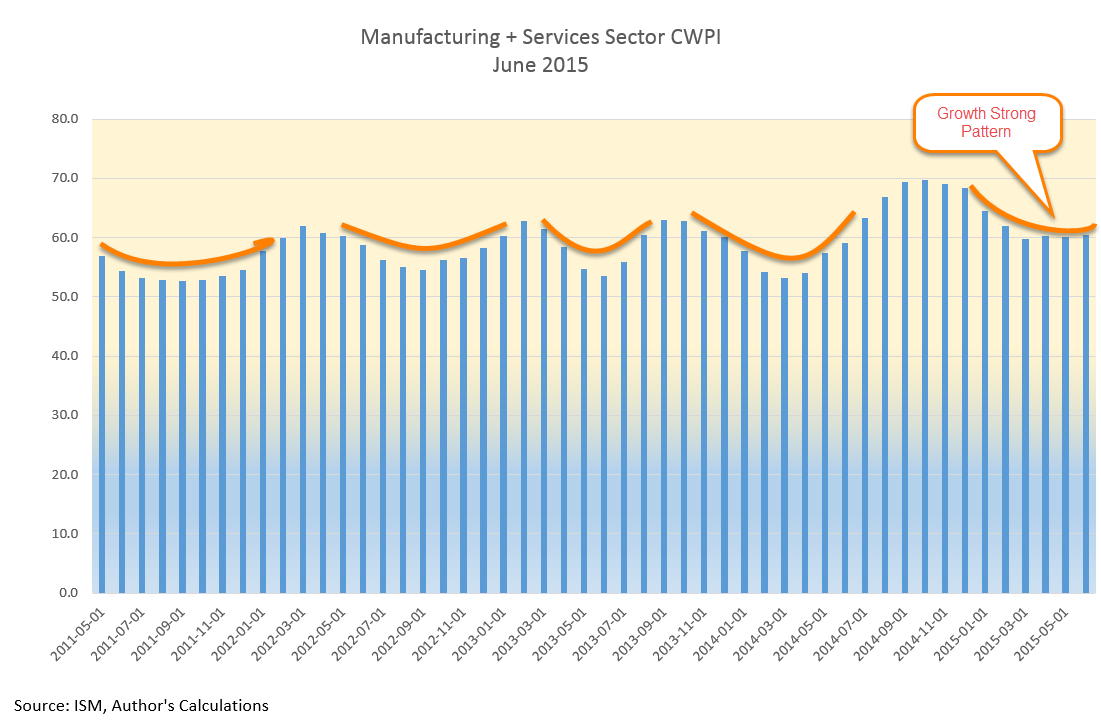

CWPI

The manufacturing sector stumbled during the harsh winter and strengthening dollar. The service sectors fell somewhat but remained strong. In June, the manufacturing sector regained strength, helping offset a slight slackening in the service economy. The composite index remains strong in a several month growth trough.

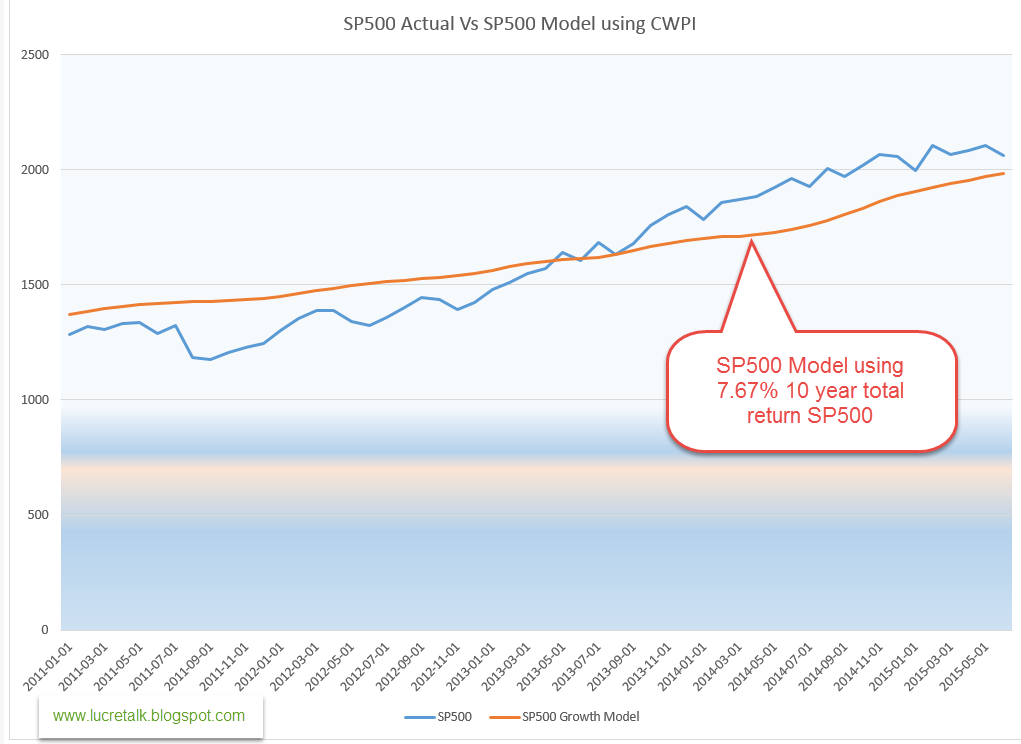

Some are of the opinion that the stock market can be overvalued or undervalued. In my opinion, liquid markets are usually fairly valued. Expectations of buyers and sellers change, causing a recalculation of future growth and a change in valuations. Comparing an index like the SP500 to a valuation model can help identify periods of investor optimism and pessimism.

I built a model based on a 930 average price of the SP500 in the 3rd quarter of 1997. At the end of 2014, the 10 year total return of the SP500 was 7.67% (Source) which I used as a base growth rate modified by the change in growth shown by the CWPI index. The CWPI measures a number of factors of economic growth but measures profits indirectly as a function of that economic growth. Profit growth may outpace or lag behind economic growth and investors try to anticipate those varying growth rates when they value a company’s stock.

Until mid-2013, the SP500 lagged behind the model, indicating a degree of pessimism. In 2013, the SP500 gained 30% and it is in that year that we see the crossover of investor sentiment from pessimism to optimism. In the first six months of this year, the SP500 has changed little and we see the index drifting back toward the model, which was only 4% less than the closing price of the SP500 index at the end of June.

In hindsight, we can identify periods when investors were too exuberant and miscalculated future growth. But we can only do so because in that future, profits and growth were not as hoped for. That is the problem with futures. We never know which one we are going to get.