December 12, 2021

by Stephen Stofka

This past week the government’s estimate of inflation in November was a whopping 6.9% increase over last year’s prices. A comparison to November 2019 prices shows an annual increase of 4.1%. From June through September of this year, the year-over-year increase in prices flattened out at 5.4%. This plateau supported the view that higher inflation readings were a temporary effect. With the availability of vaccines, Americans were resuming their lives. Supply bottlenecks at western ports were contributing to higher demand. Since September inflation has steadily increased. That wasn’t in the script.

Each month the Bureau of Labor Statistics (BLS) surveys thousands of establishments and records the prices of many goods to compute the inflation estimate. We don’t need to know the mechanics of constructing a price index to get a sense of personal inflation. Many of us conduct a smaller survey of our friends, family and fellow workers. Our basket of goods contains a few important items like food, fuel, utilities and other housing costs. From that we build an inflation base that anchors our expectations of future price changes – until it doesn’t.

If there are a series of surprises to our expectations, we modify our individual behavior in anticipation of further surprises. That behavior can aggravate inflationary pressures so that we contribute to the very condition we anticipate. In its setting of interest rates, the Federal Reserve is mindful of this effect and earlier this year two economists at the Kansas City Fed worried that inflation expectations were anchored too low (Bundick & Smith, 2021). Fed policy and a decade of low inflation had lulled people into expecting minimum disruptions in price. People might have strong reactions to price changes, small or large.

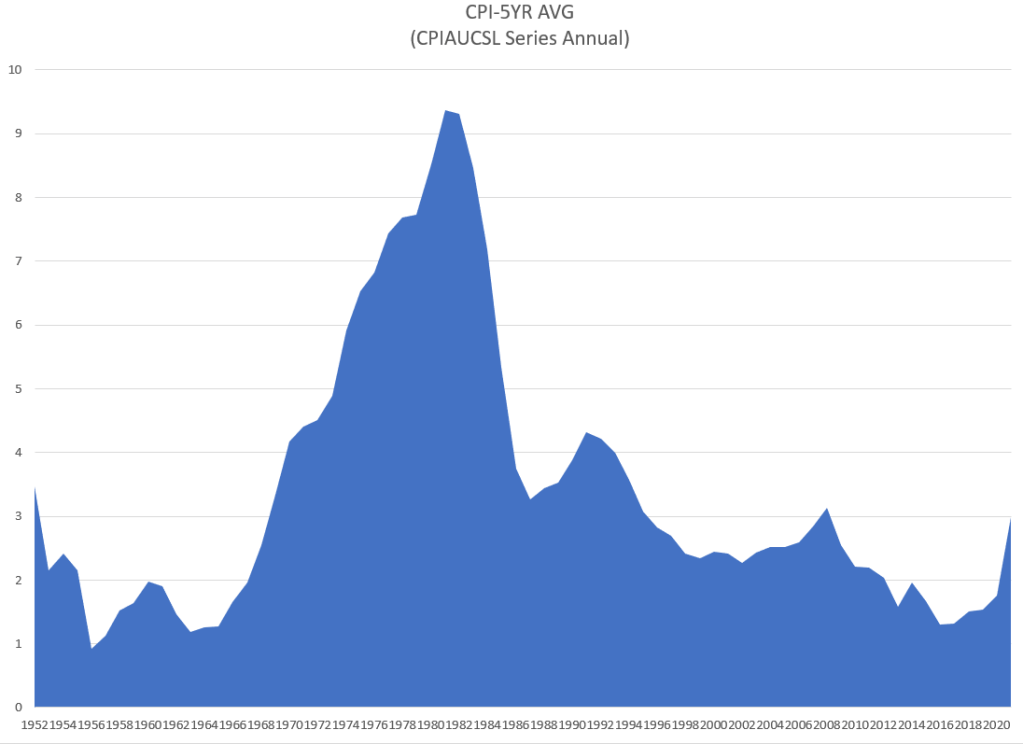

Our base of inflationary expectations is formed over several years. In the chart below is the 5 year average of annual inflation in the Consumer Price Index, the most popular measure of price change.

The mountain of inflation during the 1970s has provoked much thought by economists and policy analysts. One hundred years after World War 1, historians continue to debate the causes of that war. In 2070, economists will debate the causes and effects of that inflation mountain. The peak of the 5-year mountain shown above was more than 9% but the annual rate in 1980 was 14%. Still, our big brains make us very adaptable. It is the surprises to those long-term trends that catch our attention.

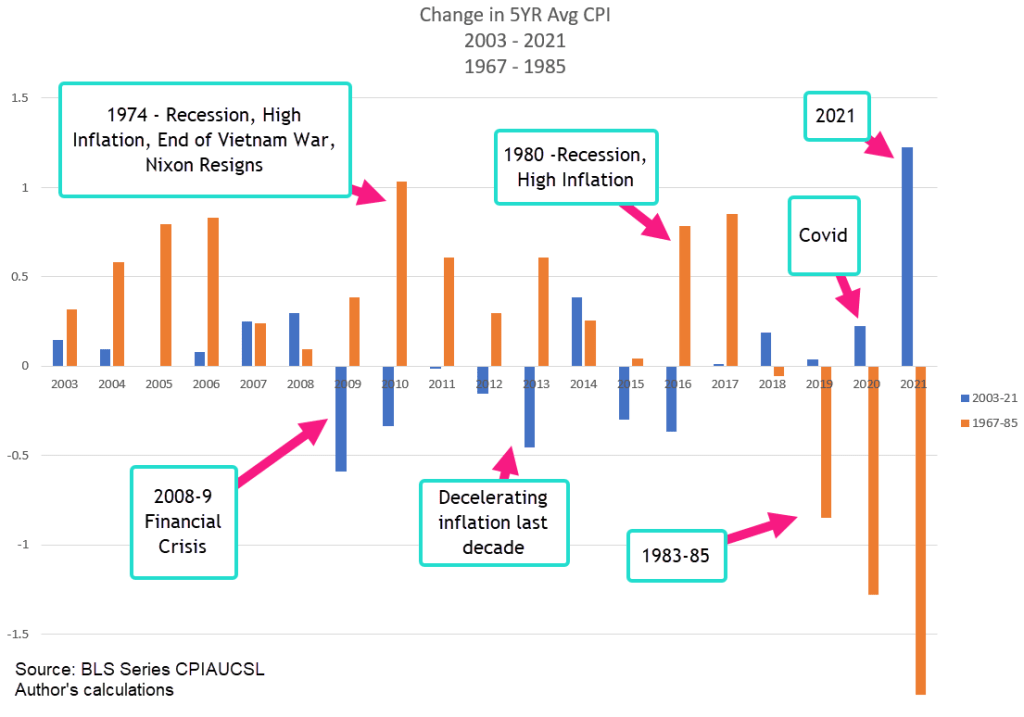

In the chart below are two 18-year periods, from 1967-1985 when we climbed the inflation mountain, and the most recent period when we have become used to sluggish growth and declining inflation expectations. The earlier period is in orange, the recent period in blue. The year labels are the most recent period. 2003 and 1967 are Year 1 in the series.

The graph illustrates the stark difference between the 1970s (orange bars) and the most recent two decades (blue bars). Between 2003 and 2020, Americans came to expect only minor change in the long-term inflation trend. The 2021 blue bar on the right is greater than the highest change post-war inflation which occurred in 1974. It’s even more dramatic because we have become accustomed to slight changes in many prices.

The discourse in this country was already aggravated and people are quick to take offense. Social media is built on people gaining attention by alerting others to offensive remarks or behavior. Politicians try to calm the narrative but inflation surprises disrupt the political conversation. Each person responds to their personal sense of inflation and whatever media voice, mainstream and radical, they prefer. Inflation surprises get people’s attention and the media’s business model is built on that attention. Even as inflation decelerates, the nightly news will continue to feature stories that heighten people’s inflation worries because worried people pay attention.

The political waters have been turbulent this past decade but price changes have been exceptionally placid. Like a rock thrown in calm waters, big surprises make big waves that take some time to dissipate. The task of the Federal Reserve’s rate setting policy is to dampen those waves – a series of small rate increases – without sending the economy into a recession.

/////////////////

Photo by Daniel Vogel on Unsplash

Bundick, B. & Smith, A. (2021). “Did the Federal Reserve Anchor Inflation Expectations Too Low?” Economic Review, Federal Reserve Bank of Kansas City. Available from https://www.kansascityfed.org/research/economic-review/did-the-federal-reserve-anchor-inflation-expectations-too-low/