July 3, 2016

A week after crash-go-boom in the stock market following Brexit, the British vote to leave the European Union, the market recovered most of the 5 – 6% lost in the two days following the vote. The reaction was a bit too intense, inappropriate to an exogenous shock, the vote, whose consequences would take several years to develop. In last week’s blog I had suggested that the market drop was a good time to put some IRA money to work for 2016. This was not some kind of magic insight. Each year’s IRA contribution amount is a small percentage of our accumulated retirement portfolio.

Buying on market dips can be an alternative strategy to regular dollar cost averaging since the market recovers within a few months after most dips, although the recovery is at a slower pace than the fall. Fear can cause stampedes out of equities; confidence grows slowly. As an example of an abrupt price decline, the SP500 index fell almost 7% in five days last August, then took more than two months to regain the price level before the fall. The 12% price drop at the beginning of this year was more gradual, occurring over six weeks. The recovery to regain that lost ground also took two months, from mid-February to mid-April. In the latter quarter of 2012, the market also took two months to erase a 7% price decline from mid-October to mid-November.

The price level of the SP500 is near the high mark set in May 2015, more than a year earlier. Only in the past year has the inflation-adjusted price of the SP500 surpassed its summer 2000 level (Chart and table). Nope, I’m not making that up. The stock market has just barely kept up with inflation for the past 15 years. The inability of the stock market to move higher indicates that buyers are not attracted to the market at current price levels. The absurdly low interest yields on bonds makes this caution especially puzzling. As stock prices recovered this past week, prices on long term Treasury bonds should have fallen as traders moved into more risky assets. Instead, bond prices have risen. As the price of long term Treasuries (ETF: TLT) broke through its January 2015 high on Friday, the last day of June, traders began betting against treasuries (ETF: TBF).

Those who are concerned about the return OF their money, the safety searchers buying bonds, are competing against those seeking a return ON their money. VIG is a Vanguard ETF that focuses on company stocks with dividend appreciation, and is favored by those seeking some safety while investing in stocks. TLT is an ETF of Treasury bonds for those seeking safety and, as expected, pays more in dividends than VIG. Rarely do we see a broad stock ETF like VIG have a yield, or interest rate, that is close to what a long term Treasury bond ETF like TLT has. At the end of this week, VIG had a dividend yield of 2.15%, just slightly below TLT. Why are investors/traders bidding up the price of Treasury bonds? Some 10 year government bonds in the Eurozone have recently crossed a dividing line and now have negative interest rates. The low, but positive, interest rates of U.S. Treasury bonds look like big open flowers to the busy bees of institutional investors around the world.

In a large group of investors, buy and sell decisions tend to counterbalance each other. Occasionally there are periods when such decisions reinforce each other and create a precarious imbalance that all too often rights itself in an abrupt fashion. Bubbles and – what’s the opposite of a bubble? – are iconic examples of this kind of self-reinforcing behavior.

In another week we will mark the middle of the summer season. The All-Star game on July 12th occurs near the halfway mark in the baseball season and advises parents in many states that there are still five to six weeks before the kids head back to school. Our mid-40s is about the midpoint of our working years, a reminder that we need to start saving for retirement if we have not done so already. It has been seven years since the market trough in March 2009. Let’s hope that this is the midpoint of a 14 year bull market but I don’t think so.

Next week will be chock full of data before the start of earnings season for the second quarter. We will get the June employment report as well as the Purchasing Managers Index. In this time of short, sharp reactions to news events, we can expect continued volatility.

/////////////////////////

Earnings

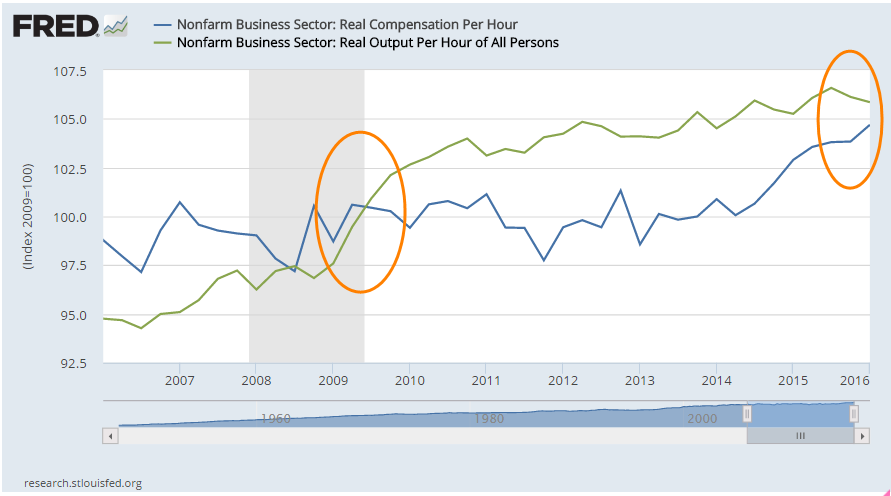

Pew Research just released a comparison of earnings by racial group and sex that is based on Census Bureau surveys, the same data that the BLS compiles into their monthly employment reports. My initial criticism of the Pew Research comparison was that they used the earnings of full and part time workers. Women tend to work more part time jobs so that would skew the earnings comparison, I thought. Thinking that a comparison of full time workers only would show different results, I pulled up the BLS report which groups the data by sex, only to find out that the differences between the earnings of men and women was about the same. At the median, women earn 82% of men.

An even more depressing feature of the BLS report is that median weekly earnings have barely kept ahead of inflation during the past decade. This wage stagnation provides a base of support for the criticisms voiced by former Presidential contender Bernie Sanders in a recent NY Times editorial.

Like a truck stuck in the mud, households are spinning their wheels without making much progress. In the coming months, Donald Trump and Hillary Clinton will try to sell themselves as the tow truck that can pull average American families out of the mud. Well, it would be nice if they would conduct their campaigns in such a positive light. The truth is that each candidate will try to convince voters that voting for the other candidate will get American families stuck deeper in the mud. The conventions of both parties are later this month. Expect the mud to start flying soon after they are over. By election day in November, we will all be buried in mud.