June 5, 2016

In parts of the country, particularly in the west, demand for housing is strong, causing higher housing prices and lower rental vacancy rates. For the first quarter of 2016, the Census Bureau reports that vacancy rates in the western U.S. are 20% below the national average of 7.1%. At $1100 per month, the median asking rent in the west is about 25% above the national average of $870 (spreadsheet link).

With a younger and more mobile population, home ownership rates in the west are below the national average (Census Bureau graph). Housing prices in San Francisco have surprassed their 2006 peaks while those in L.A.are near their peak. Heavy population migration to Denver has spurred 10% annual home price gains and an apartment vacancy rate of 6% (metro area stats).

From 1982 through 2008, the Census Bureau estimates that the number of homeowners under age 35 was about 10 million. These were the “baby bust” Generation X’ers who numbered only 70% of the so-called Boomer generation that preceded them.

Shortly before the financial crisis in 2008, a new generation came of age, the Millenials, born between 1982 and 2000, and now the largest age group alive in the U.S. (Census Bureau). Based on demographics, homeownership should have increased to about 13 million in this younger age group, but the financial crisis was particularly hard on them. Starting in 2008, homeownership in this younger demographic began to decline, reaching a historic low of 8.8 million in 2015, a 15% decline over seven years, and a gap of almost 33% from expected homeownership based on demographics.

In response to lower homeownership rates, builders cut back and built fewer homes. I’ll repost a graph I put up last week showing the number of new homes sold each year for the past few decades.

Look at the period of overbuilding during the 2000s, what economists would euphemistically call an overinvestment in residential construction. Then, financial crisis, Great Recession and kerplooey!, another technical term for the precipitous decline in new homes built and sold. As the economy has improved for the past two years, the demand for housing by the millennial generation, supressed for several years by the recession, has shifted upwards. More demand, less supply = higher prices. This younger generation prefers living closer to city amenities, culture and transportation, causing a revitalization of older neighborhoods. In Denver, developers are buying older homes, scrapping them off, and building two housing units where there was one. Gentrification influences the rental market as well as affordable single family homes and pushes out families of more modest means in some parts of town.

The housing market really overheats when rentals and home prices escalate at the same time. During the housing boom of the 2000s, many tenants left their apartments to buy homes and cash in on the housing bonanza. Rising vacancies put downward pressure on monthly rents. Move-in specials abounded, announcing “No Deposit!”, “First Month Free!” or “Free cable!” to attract renters. This time it’s different.

Rising rents and home prices put extraordinary pressure on working families who find they can barely afford to live in central city neighborhoods which offered low rents and affordable transportation. They consider moving to a satellite city with lower costs but face longer commute times and additonal transportation costs to get to work. Demographic trends shift more slowly than building trends but neither moves quickly so we can expect that housing pressures will not abate soon until the supply of multi-family rental units and single family homes increases to meet demand.

////////////////////////

Incomes

For the past four decades, household income has declined, as Presidential contender Bernie Sanders is quick to point out. Some economists also note that household size has declined greatly during that time as well so that comparisons should take into account the smaller household size. A recent analysis by Pew Research has made that adjustment and found that middle class incomes had shrunk from 62% of total income in 1970 to 43% in 2015.

But, again, comparisons are made more difficult because some categories of income, which have risen sharply in the past few decades, are not included. Among the many items not included are “the value of income ‘in kind’ from food stamps, public housing subsidies, medical care, employer contributions for individuals (ACS data sheet). Generally, any form of non-cash or lump sum income like inheritances or insurance payments are excluded. There is little dispute with the exclusion of lump sum income but the exclusion of non-cash benefits is suspect. An employer who spends $1000 a month on an employee health benefit is paying for labor services, whether it is cash to the employee or not.

The lack of valid comparison provokes debate among economists, confusion and contenton among voters. The political class and the media that live off them thrive on confusion. Those who want the data to show a decline in middle class income cling to the current methodology regardless of its shortcomings.

//////////////////////////

Employment

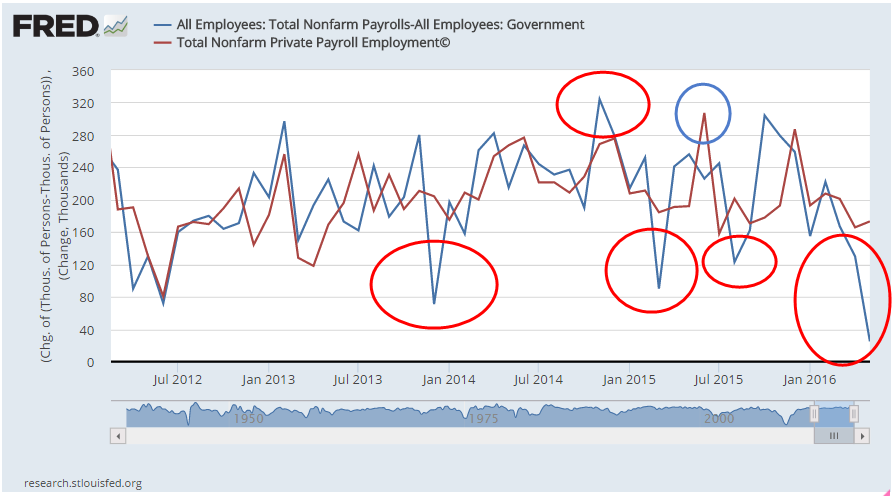

The BLS reported job gains of only 38,000 in May, far below the gain of 173,000 private jobs reported by the payroll processor ADP and below all – yes, all – the estimates of 82 labor economists. The weak report caused traders to reverse bets on a small rate increase from the Fed later this month.

Almost 40,000 Verizon employees have been on strike since mid-April and just returned to work this past week. On the presumption that a company will hire temporary workers to replace striking workers, the BLS does not adjust their employment numbers for striking workers. However, most employers of striking employees hire only as many employees as they need to, relying on salaried employees to fill in. Do strikes contribute to the spikes in the BLS numbers? A difficult answer to tease out of the data. In the graph below we notice the erratic data set of the BLS private job gains (blue line; spikes circled in red) compared to the ADP numbers (red line; spike circled in blue).

Each month I average the BLS and ADP estimates of job gains to get a less erratic data swing. The 112,000 average for May follows an average of 140,000 job gains in April – two months of gains below the 150,000 new jobs needed to keep up with population growth. Let’s put this one in the wait and see column. If June is weak, then I will start to worry.