November 10th, 2013

Friday’s release of the monthly employment situation showed strong net job gains of 204,000 jobs and big upward revisions to the previously reported gains in August and September. The market should have reacted negatively to these positive numbers (yeh, go figure) in anticipation of the Fed tapering their stimulus program of monthly bond purchases.

But first we must go back to Thursday. The first estimate of real GDP growth in the third quarter came in above even the most optimistic forecasts at 2.8%, about a full percentage point above second quarter growth. The primary reason for the gains though was the continuing build in inventories. Inventory building is good in anticipation of robust sales but, as I’ll cover later, consumer spending has not been so robust. The market reacted to the report with it’s largest daily loss in a few months.

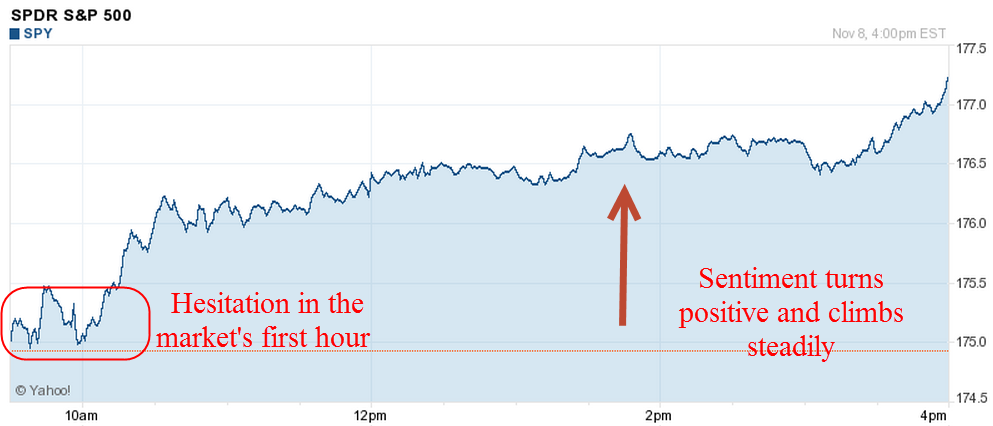

On Friday, the employment report was released an hour before the market opened. Trading began at the same level as Thursday’s close with little response to the strong job gains. We can imagine that traders were twittering furiously to each other in the opening hour, trying to gauge the sentiment. Buy in on strength in the employment numbers or sell on the strength in the employment numbers? After the initial hesitation, the main index gained continuing momemtum throughout the day, with a final spike at the closing bell.

After digesting some of the numbers in the report, I think that traders realized how weak some of its components were, dimming the probability that the Fed will ease up on the gas pedal. The Consumer Sentiment Survey, released a half hour after the opening bell, showed a continuing decline. Within minutes, the market started trading higher.

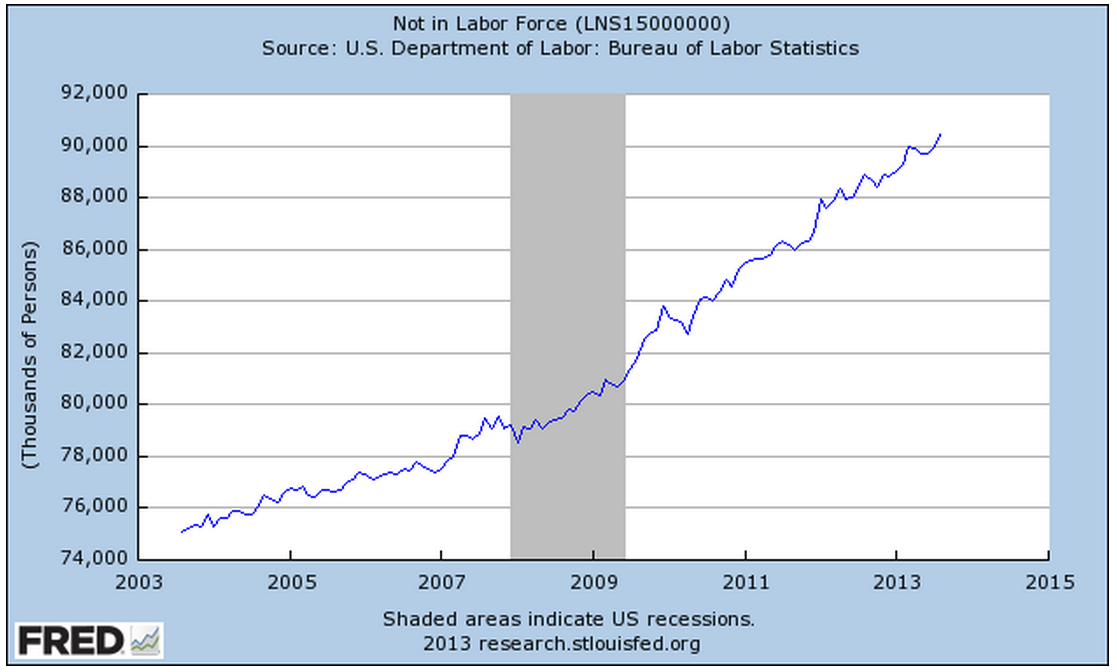

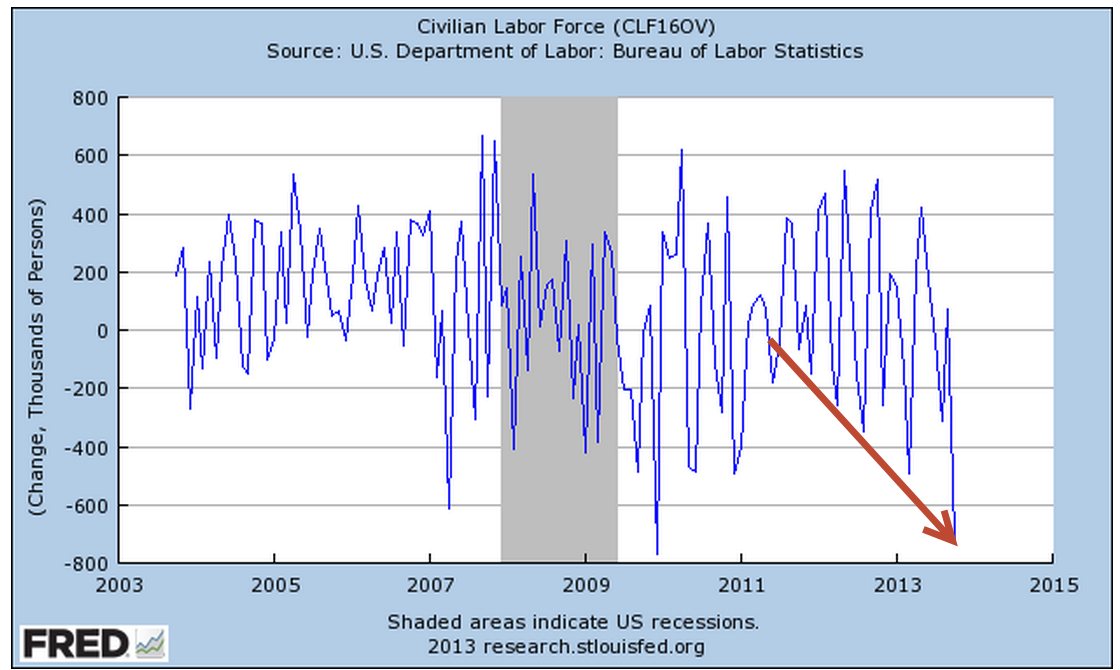

The first number popping in the employment report is the 702,000 people who dropped out of the labor force. To put that number in perspective, take a look at the chart below which shows the monthly changes in the labor force for the past ten years. This is the second worst decline after the decline in December 2009, shortly after the official end of the recession.

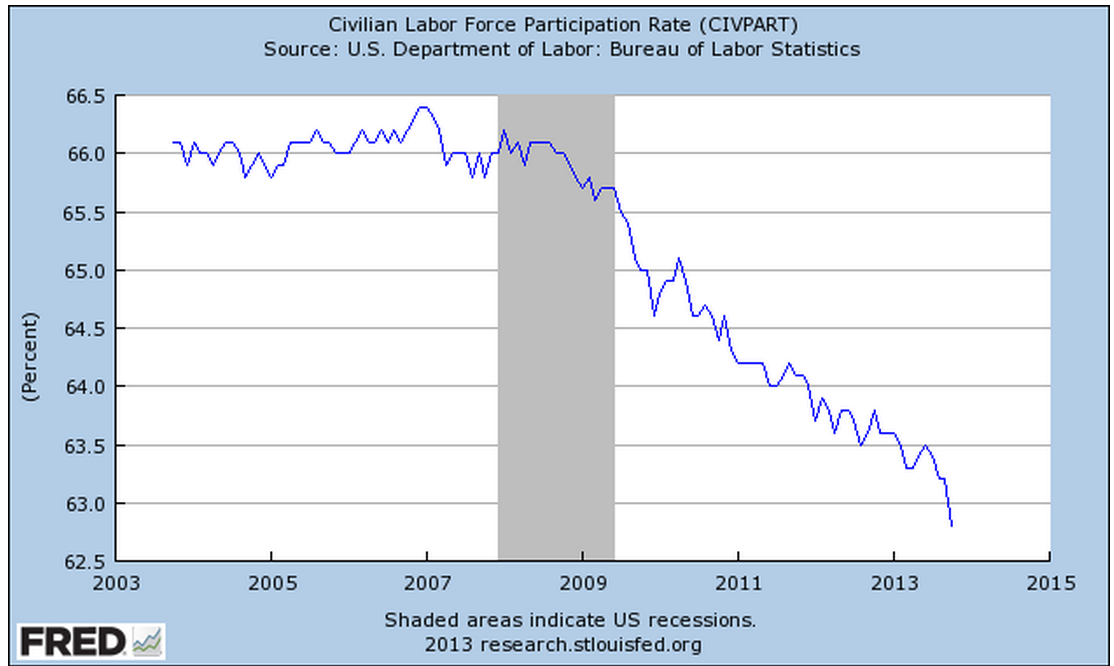

This month’s .4% steep drop in the Civilian Force Participation Rate ties the record set in December 2009 when the economy was still on its knees. The rate has now fallen below the 63% mark, far below the 66% rate of several years ago.

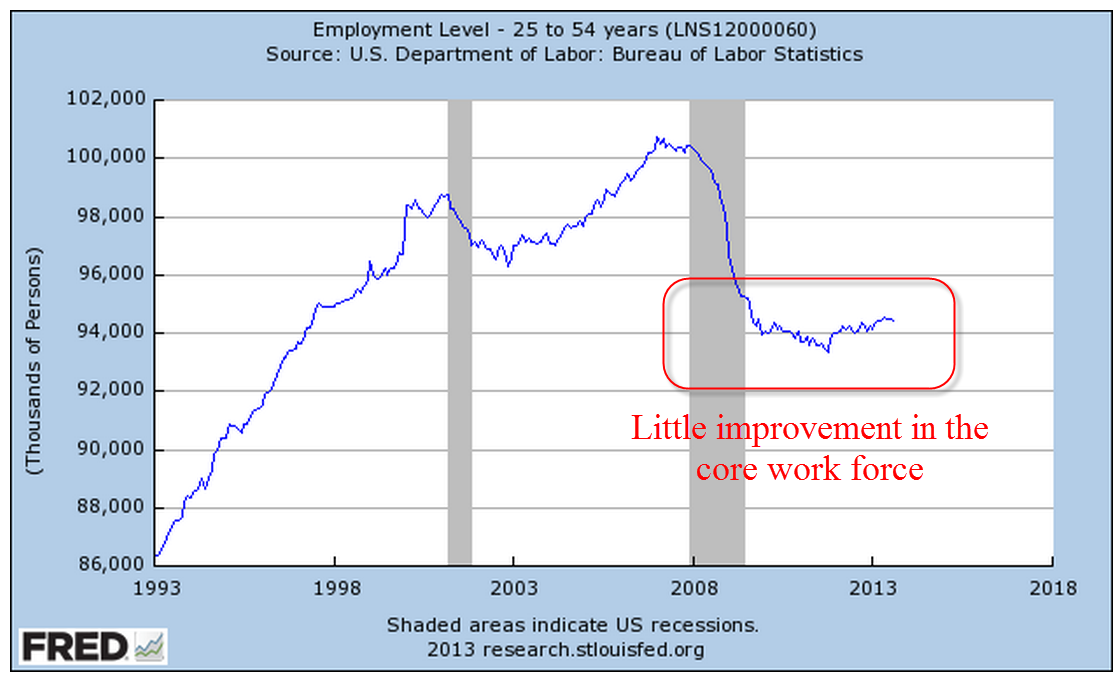

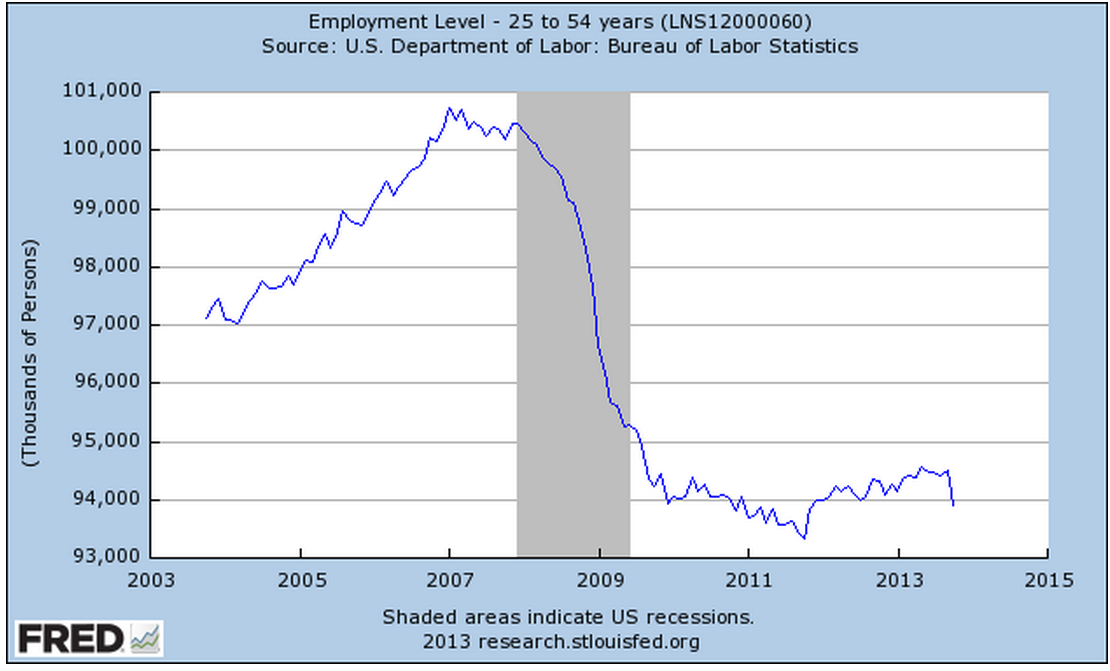

Employment in the core work force aged 25 – 54 actually dropped this past month. Classifications of employment by age, sex, and education come from the survey of households, not employers, and may have been affected somewhat by the goverment shutdown. But the numbers of the past years show that there has been no recovery for this segment of the population. In each lifetime, there are stages that last approximately twenty years. This time of life should be about building careers, building families, building assets and growing income. I fear that for too many people in this age group, the slowly growing economy has not been kind. This affects both a person’s current circumstances and dampens prospects for the future.

The headline job gains and classification of the types of jobs come from a separate survey of employers called the Establishment Survey. Employers report their payroll count as of the 12th of each month. Because they received paychecks, federal employees furloughed during the government shutdown in the first two weeks of October were still counted as employed in October.

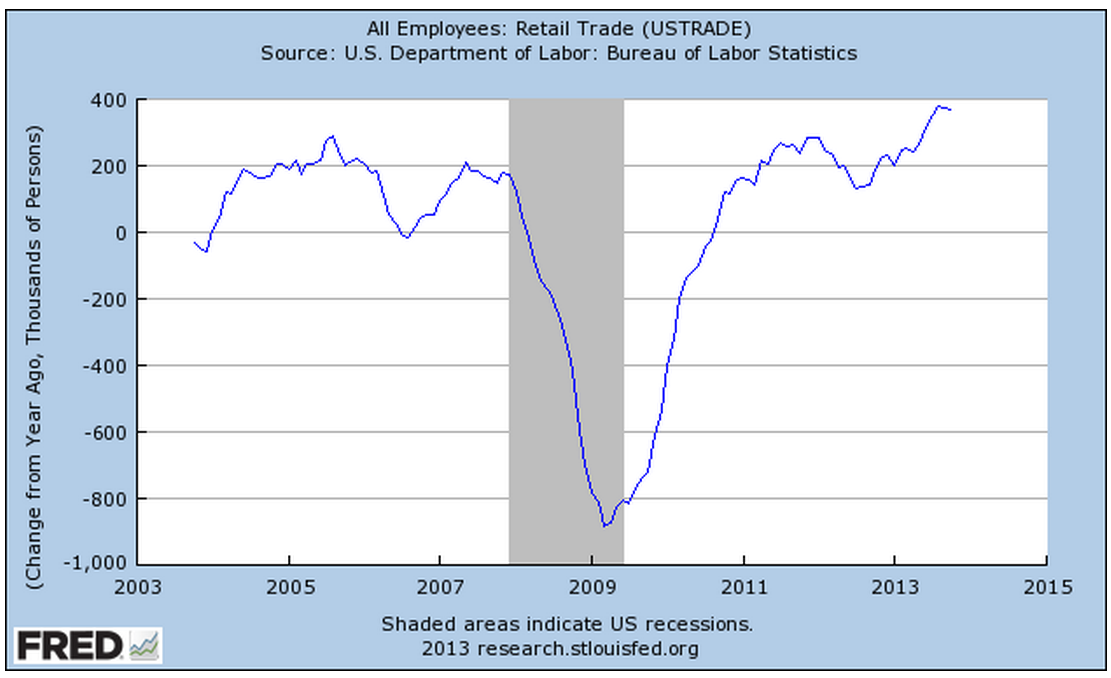

There were some strong positives as well in this report. Retailers added 44,000 jobs, above the average gains of 31,000. This year’s gains have been the strongest in fifteen years.

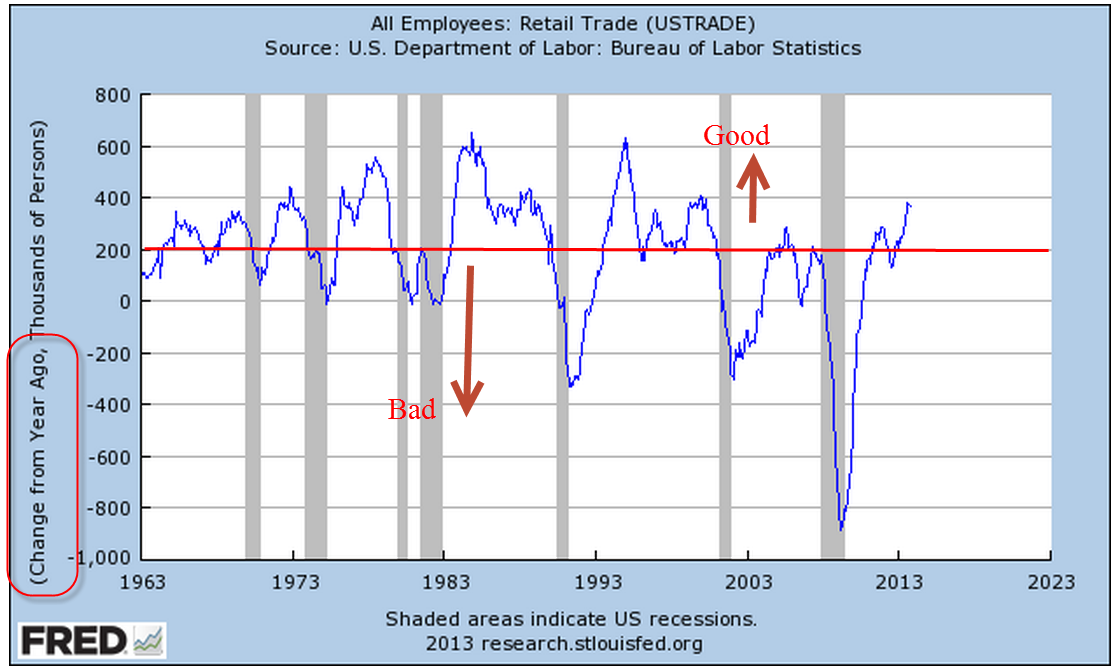

The gains are about half of the eye-popping gains of the past fifty years, but they indicate a confidence among retailers. Retail jobs are often the first job of many younger workers, who have endured persistently high unemployment during this recession. Here’s a glance at yearly job gains in the retail sector for the past fifty years.

As the holiday shopping season gets underway, all eyes will turn to the retail sector as an indicator of the consumer’s mood. The U. of Michigan Consumer Sentiment Survey, released Friday, showed a continuation of an erosion in consumer confidence. After peaking during the early summer at 85, this index has declined to 72, about the same levels as late 2009 when the economy was particularly weak. The Expectations component of this survey, which reflects confidence in employment and income, has declined to about 63. Gas prices have been declining, inflation has been near zero, and stock and home prices have been rising but this survey shows a steady decline in confidence. The government shutdown probably had some effect on the consumer mood but the budget battles are not over. This is the 7th inning stretch and few are standing up to sing “America The Beautiful.”

Professional Services and Health Care have been consistent leaders in job growth for the past few years but gains in these sectors have declined. The unemployment rate notched up to 7.3% from 7.2%.

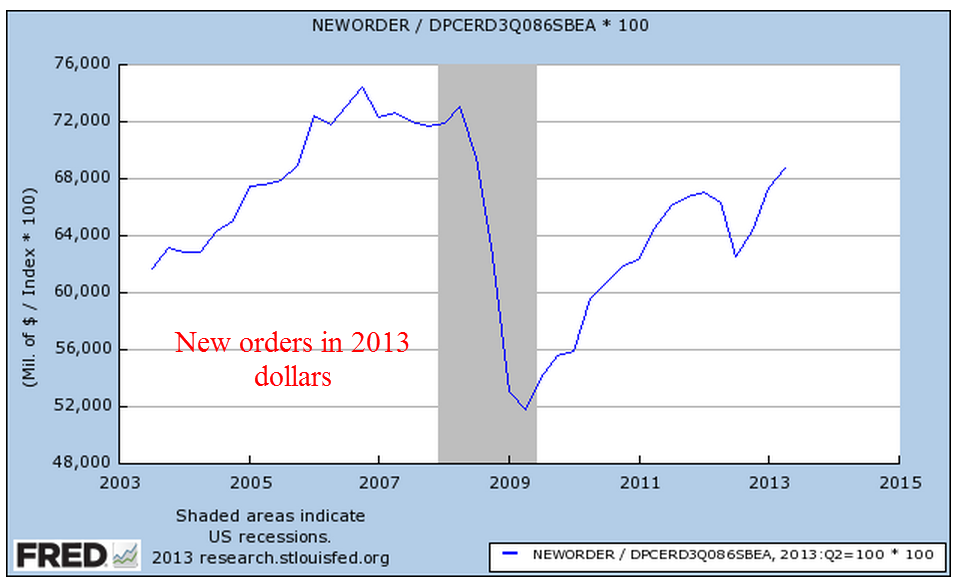

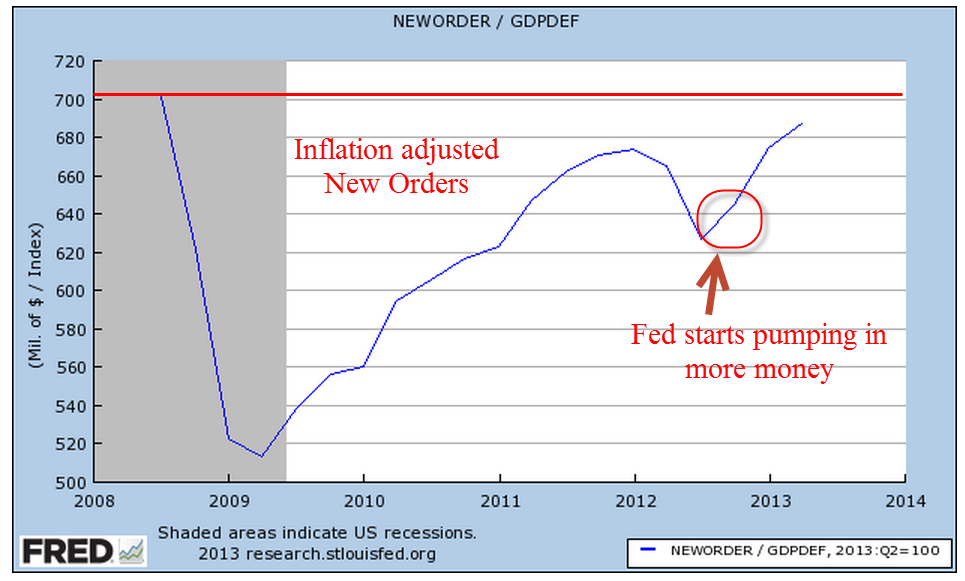

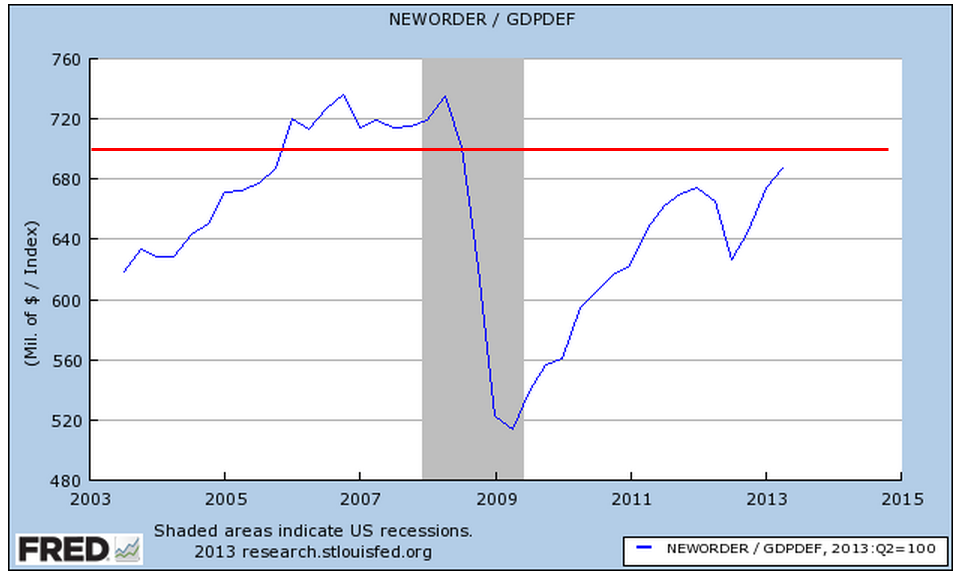

In a catch up effort after the recent government shutdown, the Dept of Commerce released data on factory orders for both August and September. While the manufacturing sector as a whole has been strong, the weakness in new orders in these two months indicates a tempering of industrial production in the near future.

When adjusted for inflation, the level of new orders is still below the levels of mid-2008.

If we zoom out ten years, we can see that we at about the same levels as late 2005.

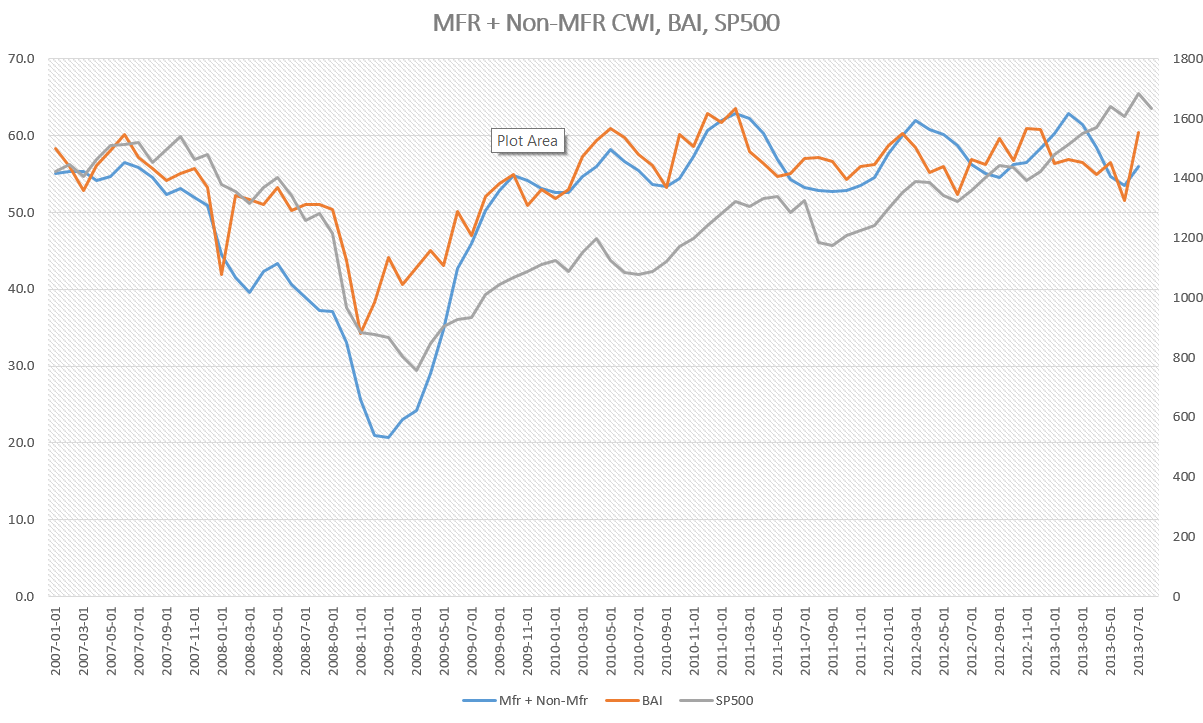

ISM released their monthly non-manufacturing survey, showing sustained and rising strong growth at just over 55, up a point for the previous month. I’ve updated the CWI that I’ve been tracking since June of this year. A three year chart shows that even the troughs are part of a sustained growth pattern. Furthermore, the span of the troughs keeps getting shorter, indicating a structural growth in the economy.

Let’s look back six years and compare this composite index of economic activity with the market.

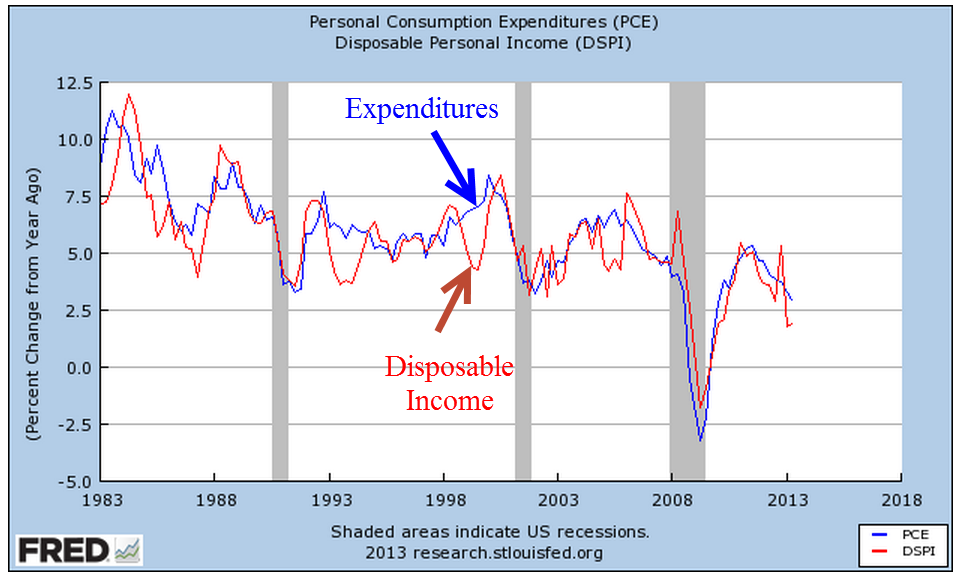

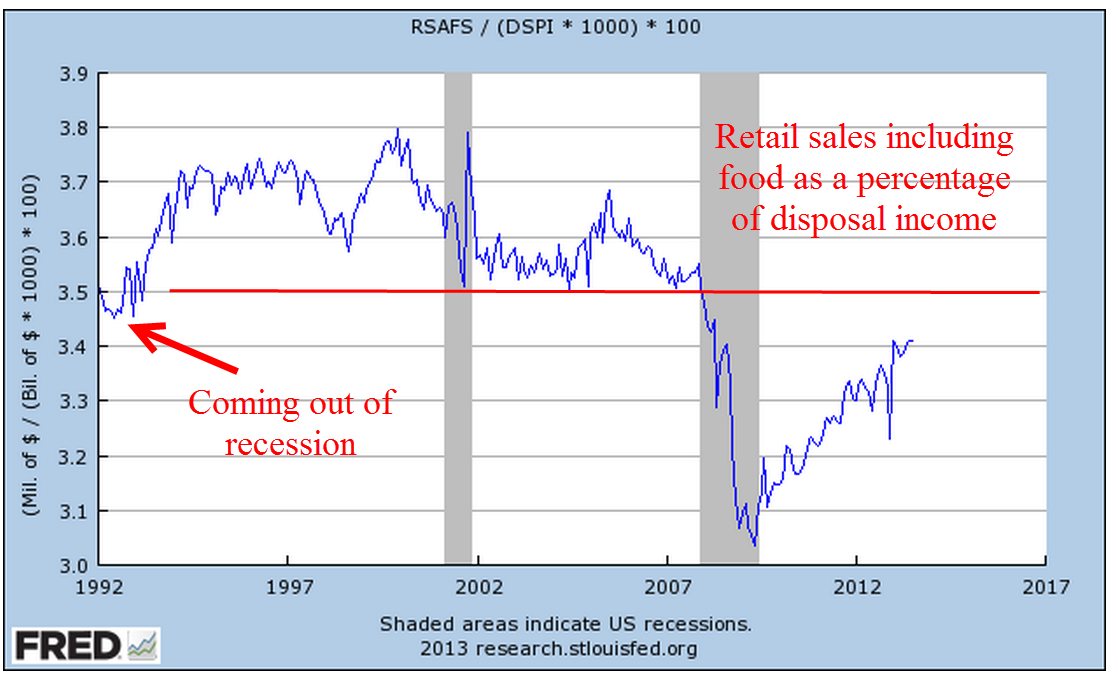

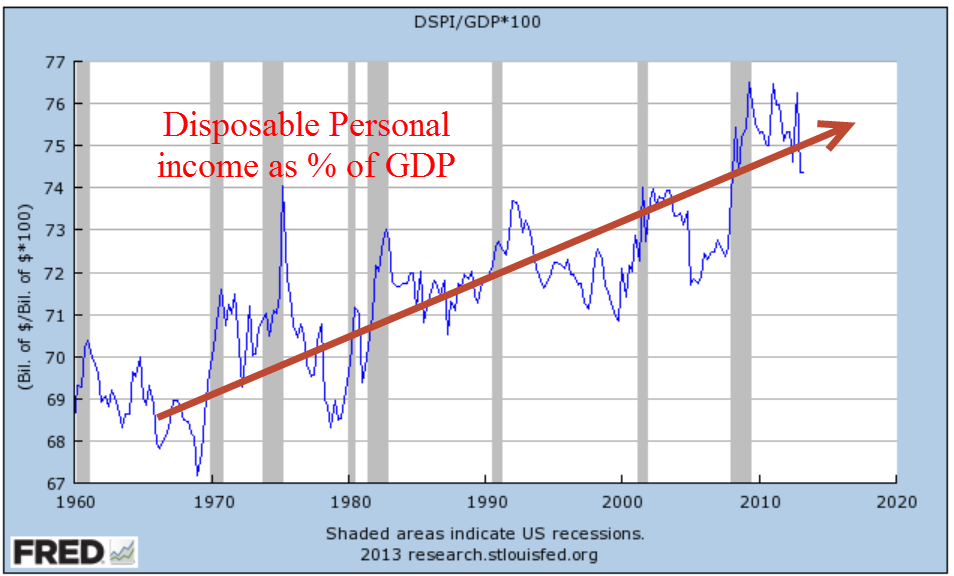

The monthly report of personal income and spending released Friday showed less than 1% inflation on a year over year basis. For the second month, incomes increased at an annualized rate of 6%, yet consumer spending remains sluggish. The chart below shows the year over year growth in spending for the past twenty years.

A longer term graph shows the current fragility in an economy whose primary component is consumer spending.

Both the manufacturing and non-manufacturing portions of the economy continue to expand. Employment has risen consistently at a level just above population growth. Inflation is tame but so is consumer spending. Income is rising. Budget battles loom. Expectations for holiday retails sales increases are modest. Will the Fed ease or not ease? The medium to long term outlook is positive, but with a watchful eye on any further declines in the momentum of consumer spending growth. The short term outlook is a bit more chaotic. We can expect further wiggles in the stock market as traders rend their garments, struggling with Hamlet’s dilemma: To buy or not buy? To sell or not sell?