September 16th, 2013

September marks two anniversaries that we wish had not happened. One of those is the financial crisis and the meltdown of the economy in September 2008. In the fourth quarter of 2008, GDP fell about $250 billion. By itself, this was not a disaster. However, it came on the heels of a decline in the 2nd quarter and flat growth in the 1st quarter.

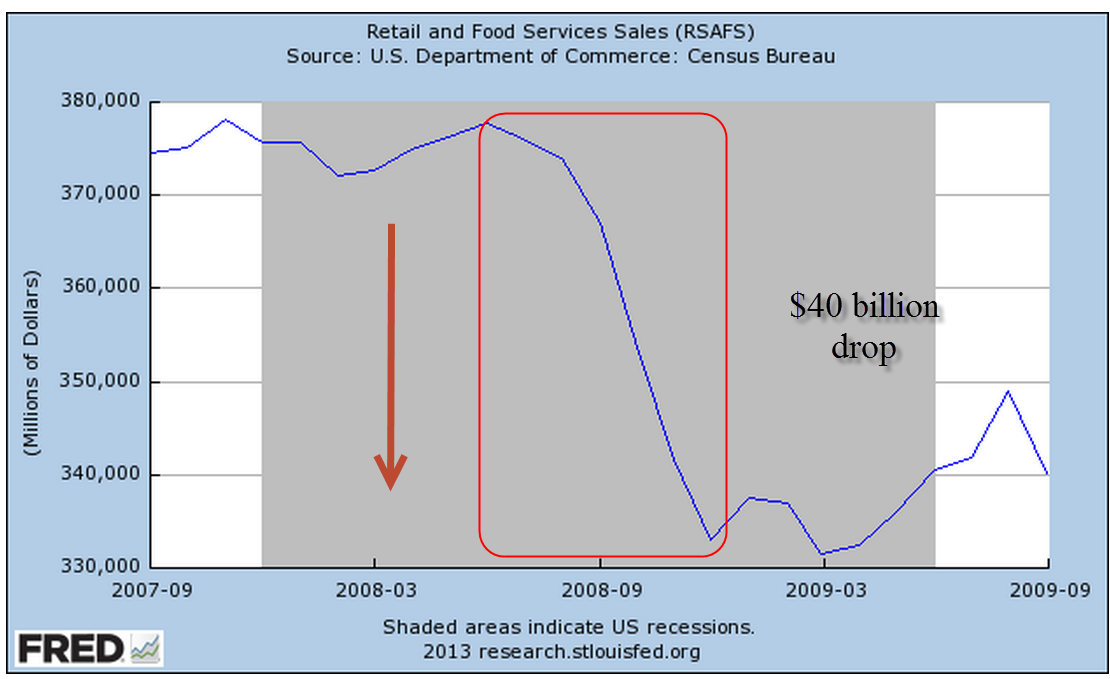

Almost overnight, consumers cut back on their spending. Retail sales dropped $40 billion, a bit more than 10%.

There was little drop in food sales – people gotta eat. All of the drop was in retail sales excluding food.

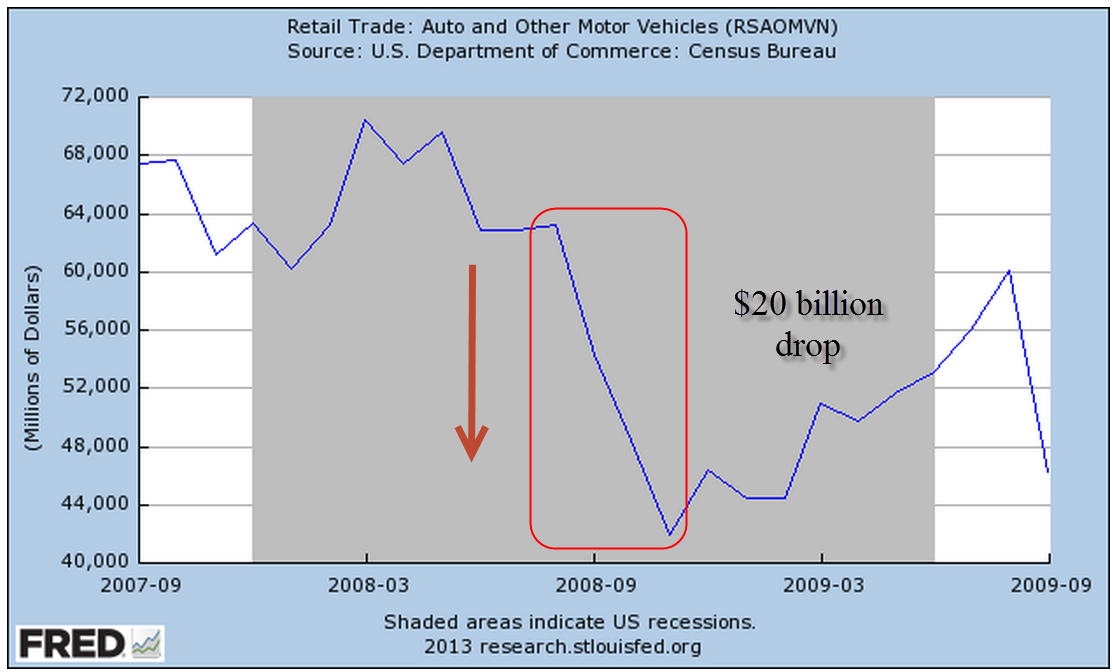

Retail sales are less than 3% of GDP. Contributing to the GDP decline was the 33% fall in auto sales, about $20 billion.

Offsetting the decline in retail sales, however, total Government spending increased $40 billion in the 4th quarter.

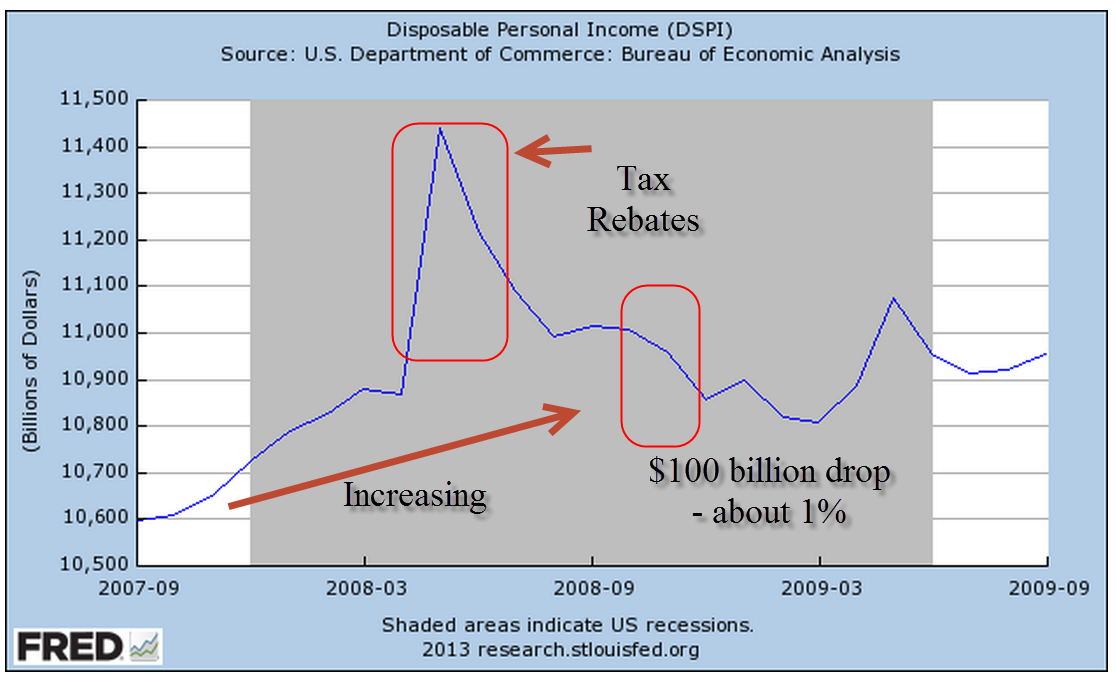

Disposable Personal Income (income after taxes) fell $100 billion, about 1%, but was still on a healthy upward trajectory during the year preceding the crisis.

We routinely import more goods and services than we export. In the national accounts of domestic production, imports are naturally treated as a negative number, while exports are positive. The difference, called net exports, is negative and reduces GDP. For all of 2008, we had about the same net exports as 2007.

Gross Private Domestic Investment declined $200 billion or 9% over the year. This includes investments in buildings, equipment and housing. Housing accounted for $150 billion of the change.

The TV news media, a visual medium, focuses on crises because it is not well suited for more thoughtful analysis. On camera interviews in a crisis do not have to be very detailed or accurate. Viewers understand that it is a crisis. But viewers are also an impatient bunch with trigger fingers on their remote controls. Video footage has to be loaded, sequenced and edited. On air interviews and several short video clips run repeatedly during a news hour will have to do. The recent flooding in Colorado is a reminder that there is only so much video footage available. TV stations simply reran the same sequences over and over. On the 9 PM local news, the station featured an on site reporter in front of a driveway heaped full with damaged belongings and furniture. At 10 PM, a different local station featured their reporter in front of the same house.

In September 2008, the media focused on the financial crisis and the implosion of stock prices. When the stock market opens up on a September morning 300 points down, what else is there to cover? It is important to understand that the economy is a big organism with a lot of moving parts. The housing decline was already two years old before the financial crisis hit in September 2008.

Fast forward to this September. A day ahead of the ISM Manufacturing report on September 4th came the news that China’s manufacturing sector has strengthened, a positive note in the Asian region where capital outflows from emerging nations have weakened the economies of other nations. The prospect of higher interest rates in the U.S. has sparked a change in money flows to the U.S., strengthening the dollar against the currencies of emerging countries. This change in flows promises to put pressure on companies in developed nations who had earlier borrowed money in U.S. dollars to take advantage of low interest rates. The stream of capital follows the deepest channel. The combination of risk and reward in each country can largely determine the depth of the channel. Countries can, by central bank policy or law, control the flows of foreign investment into and out of their country. China and India exercise some degree of control in an attempt to maintain some stability in their economies. Like other developed nations, the U.S. has few controls. In the run up of the housing bubble, foreign flows into the U.S. provided the impetus for investment banks like Goldman Sachs to initiate and bundle many thousands of mortgages into tradable financial products that met the demand by foreign investors.

Manufacturing data in the Eurozone was a big positive with several countries recording their strongest growth in over two years. The Purchasing Managers Indexes (PMI) are not strong but are showing some expansion, a turn about from the slight contraction or neutral growth of the past two years. The fragile economic growth of the Eurozone has been exacerbated by the concentration of growth in France and Germany, particularly Germany. Recent strong gains in some of the peripheral countries, those in the former Communist bloc and southern Europe, suggest that economic activity is becoming more dispersed. Dramatic differences in the economies of countries that share the same currency make the setting of monetary policy difficult and it is hoped that more even growth will take pressure off central banks in the Eurozone.

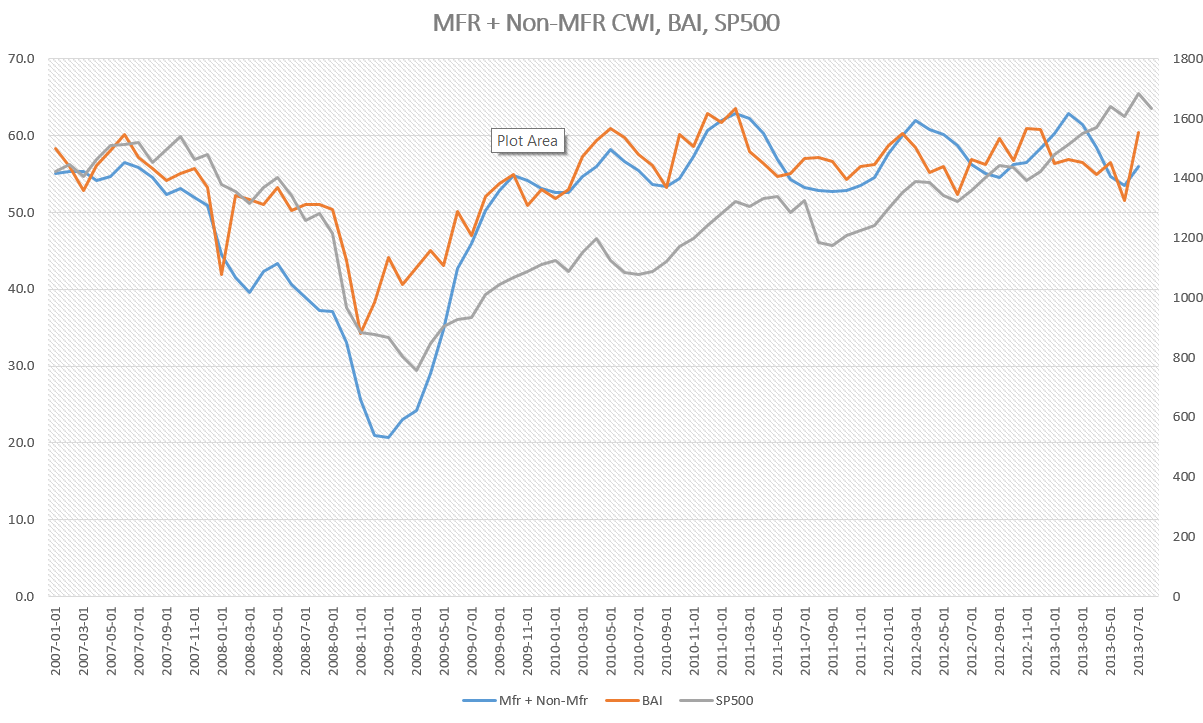

At an overall reading of 55.7, the ISM Manufacturing report released a week ago Tuesday showed even stronger growth than the previous month’s index of 55.4. 50 is the neutral mark that indicates neither expansion or contraction of manufacturing activity. New orders began a worrisome decline in the latter part of 2012 that persisted into the spring of this year, and the turnaround of the past few months forecasts a healthy manufacturing sector for the next several months. Levels above 60 in any of the components of this index indicate robust growth; both new orders and production are above that mark.

A few days later ISM reported their Non-Manufacturing composite was 58.6, indicating strong expansion in service industries which make up the bulk of the economy. The Business Activity index came in at a robust 62.2. ISM also reported that their figures for June had an incorrect seasonal adjustment. The New Orders Index for June was revised up a significant 2%. Prices were revised up 4.3%. Other changes were relatively insignificant.

The constant weighted index I have been tracking smooths the ISM data so that it responds less strongly to one month’s data but it is showing strong upward movement in both manufacturing and non-manufacturing.

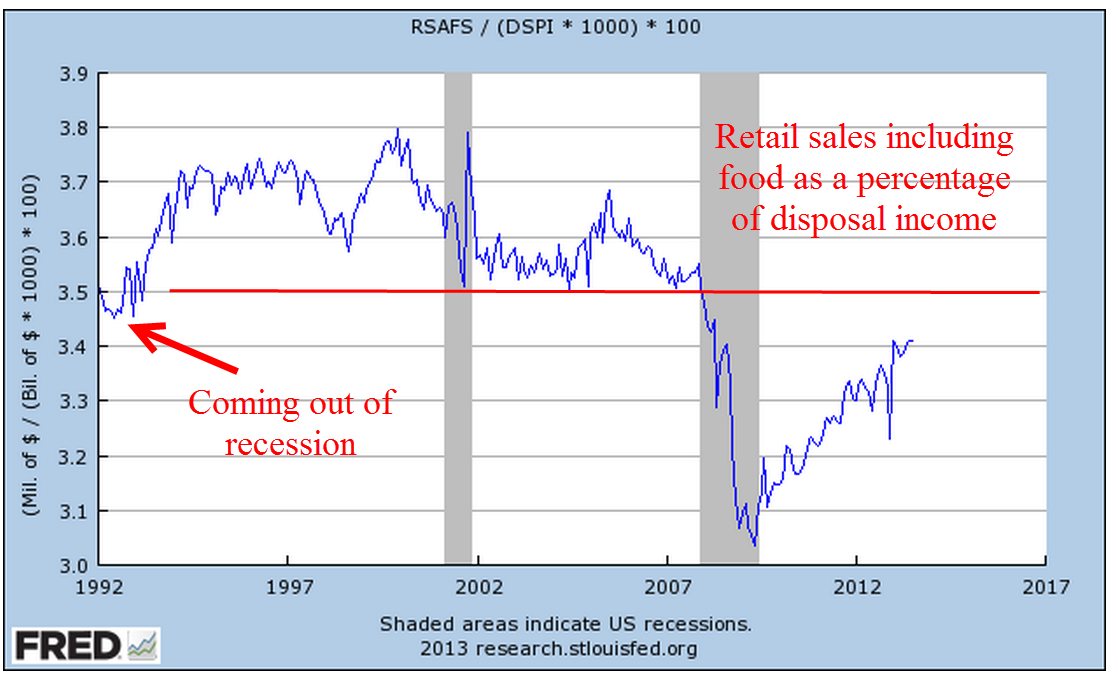

The Commerce Dept reported last Friday that Retail Sales continue to grow at a modest pace. However, let’s look at retail sales as a percent of disposable income. Consumers are still cautious.

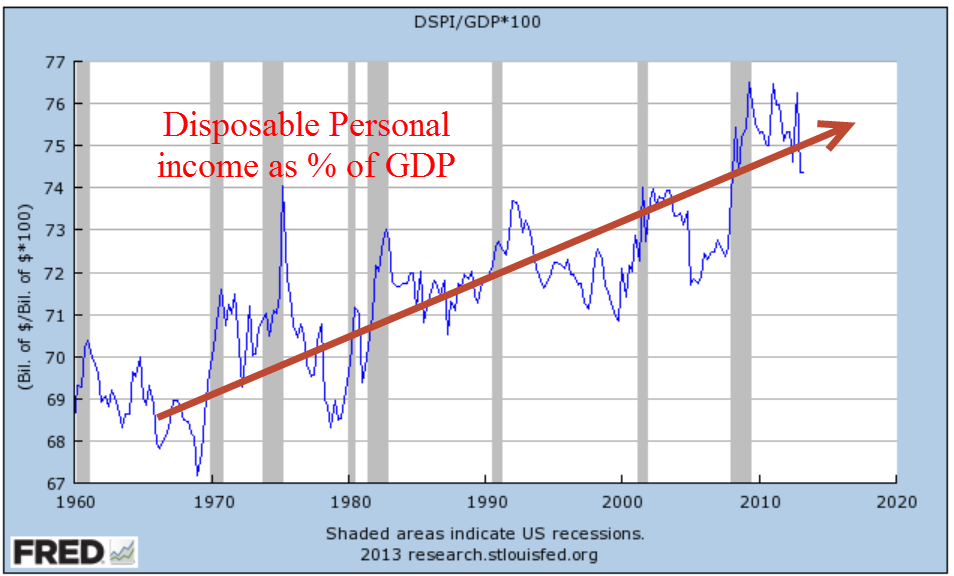

Speaking of disposable income. As we import more and export less, disposable income as a percent of GDP continues to rise. This percentage rises sharply at the onset of recessions. It is a bit troublesome that the 40 year trend is rising.