Fiscal realists have often championed a Starve the Beast theory, which aims to restrain the growth of government spending by restricting or reducing the growth of tax revenue to that government. The theory intuitively makes sense. With less money to spend, politicians will be forced to lower spending. During the past thirty years, however, the exact opposite has happened at the federal level. When tax cuts were enacted, spending went up. When taxes were raised, spending went down. How to explain this curious phenomenon?

Jerry referred me to two articles written in 2004 and published by two think tanks commonly thought to be at opposite ends of the political spectrum, the libertarian leaning Cato Institute and the liberal leaning Brookings Institution. In an article at About.com, Mike Moffat cites a one page summary by William Niskanen, Chairman of the Cato Institute, of a study that Niskanen did in 2002 which examined the relationship between tax cuts and spending. He found an inverse relationship; taxes went up, spending went down and vice versa.

Two authors at the Brookings Institution, also writing in 2004, examined the voting records of mostly Republican lawmakers who had taken the “No New Taxes” pledge that year and found that the majority were, in fact, liberal spenders. In 2004, the authors predicted that the combination of tax cuts and liberal spending by a Republican majority would dramatically increase the deficits. Ballooning deficits during the following four years did lead to a doubling of the national debt, just as they predicted.

How many of the 258 original pledge signers are still in office? I don’t have time for that analysis but the Americans For Tax Reform lists 235 Representatives and 41 Senators in the upcoming Congress who have taken a reiteration of the no tax pledge, called the Taxpayer Protection Pledge.

This past weekend President Obama and Republican leaders from the upcoming Congress hammered out a “framework” of compromise over the renewal of the Bush Era tax cuts. Republicans were adamant that the top 3 – 5% of incomes retain the slightly lower tax rates of the past decade. While Democrats may ridicule Republican politicians as paid stooges for the rich, many Republicans openly took the pledge, were presumably voted or retained in office because of the pledge and are honoring that pledge to their voters.

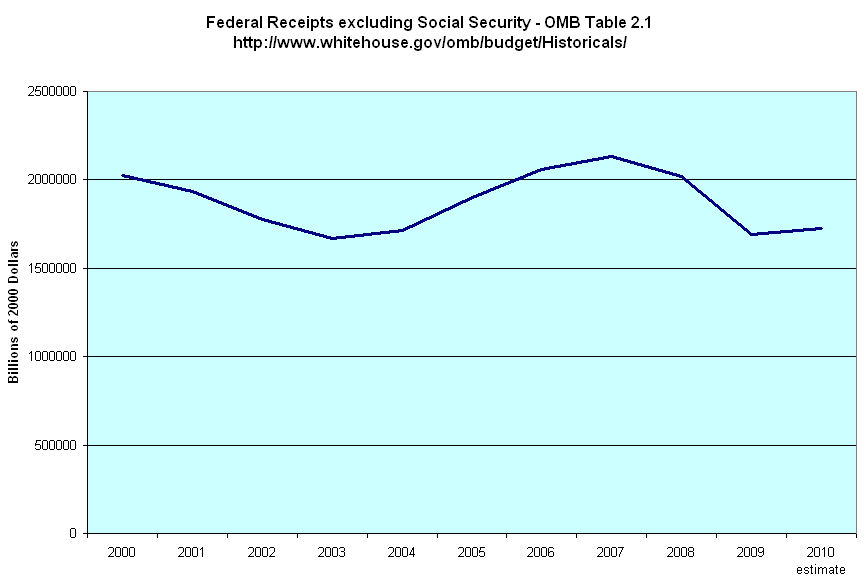

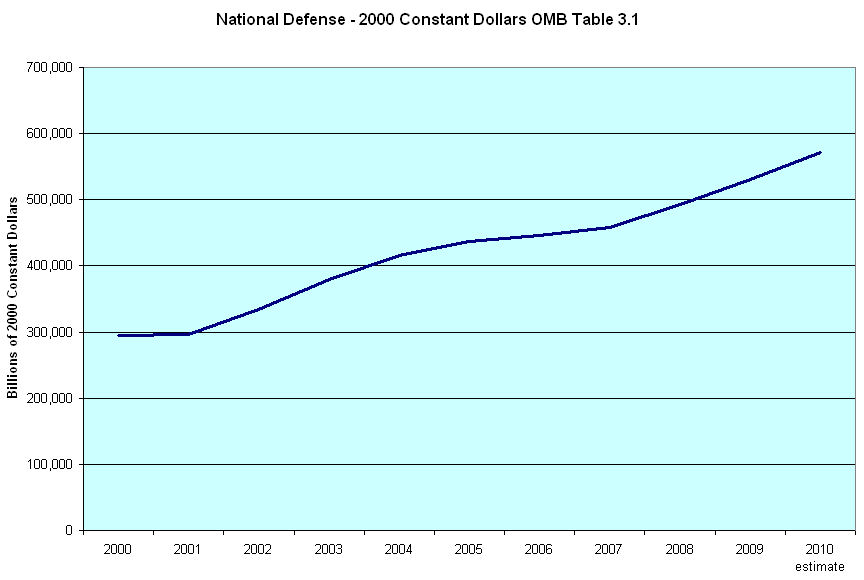

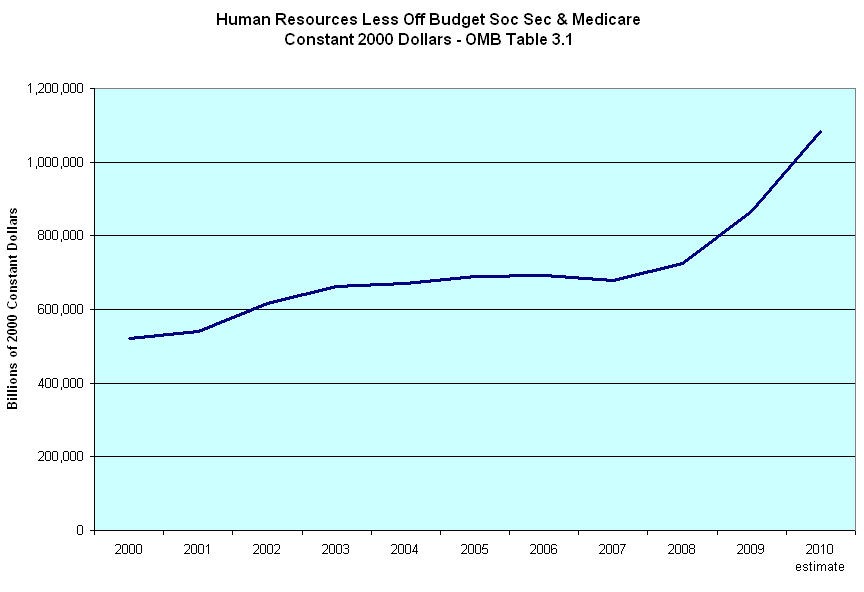

Neither Republicans or Democrats have taken a pledge to reduce spending. Below is a graph of Federal spending without transfer payments like Social Security, unemployment insurance and other social welfare programs.

Notice that leveling off in the 90s? To decrease the ballooning debt incurred during the Reagan years, taxes were increased in 1993 under the newly elected Clinton Administration. Voters balked, sending Republicans to Congress in 1994 on a pledge to cut spending, which they did. The Starve the Beast theory works in reverse. When voters have to come up with more taxes now, they demand reductions in government spending. When taxes are cut, voters lose any urgency to insist that their representatives cut spending. They talk about leaving a tax burden for their children but they don’t flood the offices of their representatives with phone calls, letters and emails. That flood happens when the tax burden for government spending falls on voters now.

Federal spending is only a third of the problem. The 50 states constitute 2/3 of total government spending. Below is a graph, in real dollars, of total government spending less transfer payments.

Tax cuts produce less real tax revenue and disincentivize voters to scrutinize the spending habits of their elected officials, thus increasing our national debt. Tax increases produce more real tax revenue and stir up a passion in voters to get spending in control, thus reducing the national debt. Over the long term, the choice should be clear – increase taxes which cuts spending.

What is the framework that Obama and Republican leaders worked out this past weekend? Provisions include a two year extension of the tax cuts for all income earners, a 2% payroll tax reduction, an extension of federal unemployment benefits and an accelerated write off of business investment. The two year cost of this is over $850B. In short, this is Stimulus 2, slightly larger in cost than the $800+ billion that Stimulus 1 cost. Stimulus 1 featured stimulus spending controlled from the commanding heights of the federal and state government. Stimulus 2, if passed, will feature spending controlled by the people and businesses of this country. The real risk of Stimulus 2 is that the receivers of these tax breaks will not spend the savings but continue to pay down accumulated debt. Businesses are already holding onto an estimated $2 trillion in cash, reluctant to invest the money until there is a sure sign that the economy is turning around and they can make some return on their investment.

Will accelerated tax deductions for investment induce businesses to loosen their purse strings? Stay tuned as the Great Recession continues….and continues.