June 3, 2018

by Steve Stofka

First I will look at May’s employment report before expanding the scope to include some decades long trends that are great and potentially destructive at the same time. In the plains states of Texas, Oklahoma, Kansas, and Nebraska, summer rain clouds are a welcome sign of needed moisture for crops. That’s the good. As those clouds get heavy and dark and temperatures peak, that’s bad. Destruction is near.

May’s employment survey was better than expected. The average of the BLS and ADP employment surveys was 203K job gains. The headline unemployment rate fell to an 18 year low. African-American unemployment is the lowest recorded since the BLS started including that metric in their surveys more than thirty years ago. As a percent of employment, new unemployment claims were near a 50-year low when Obama left office and are now setting records each month.

During Obama’s tenure, Mr. Trump routinely called the headline unemployment rate “fake.” It’s one of many rates, each with its own methodology. Now that Mr. Trump is President, he takes credit for the very statistic that he formerly called fake. The contradiction, so typical of a veteran politician, shows that Mr. Trump has innate political instincts. A President has little influence on the economy but the public likes to keep things simple, and pins the praise or blame on the President’s head.

The wider U-6 unemployment rate includes discouraged and other marginally attached workers who are not included in the headline unemployment rate. Included also are involuntary part-time workers who would like a full-time job but can’t find one. Mr. Trump can be proud that this rate is now better than at the height of the housing boom. Only the 2000 peak of the dot com boom had a better rate.

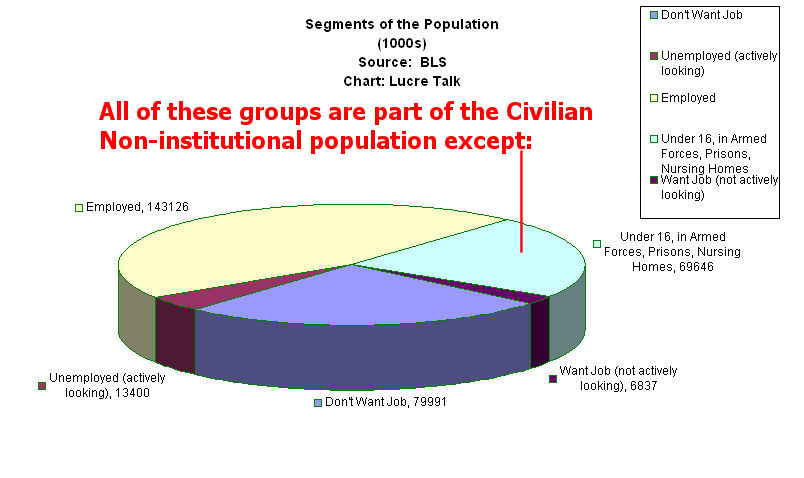

Let’s look at a key ratio whose current value is both terrific and portentous, like a summer’s rain clouds. First, some terms. The Civilian Labor Force includes those who are working and those who are actively seeking work. The adult Civilian Population are those that can legally work. This would include an 89-year old retiree and a 17-year old high school student. Both could work if they wanted and could find a job, so they are part of the Civilian Population, but are not counted in the Labor Force because they are not actively seeking a job. The Civilian Labor Force Participation Rate is the ratio of the Civilian Labor Force to the Civilian Population. Out of every 100 people in this country, almost 63 are in the Labor Force.

While that is often regarded as a key ratio, I’m looking at a ratio of two rates mentioned above: the Labor Force Participation Rate divided by the U-3, or headline, Unemployment Rate. That ratio is the 3rd highest since the Korean War more, ranking with the peak years of 1969 and 2000. That is terrific. Let’s look at the chart of this ratio to understand the portentous part.

Whenever this ratio gets this high, the labor economy is very imbalanced. Let’s look at some previous peaks. After the 1969 peak, the stock market endured what is called a secular bear market for 13 years. The price finally crossed above its 1969 beginning peak in 1982. In inflation-adjusted prices, the bear market lasted till 1992 (SP500 prices). Imagine retiring at 65 in 1969 and the purchasing power of your stock funds never recovers for the rest of your life. Let’s think more pleasant thoughts!

For those in the accumulation phase of their lives, who are saving for retirement, a secular bear market of steadily lower asset prices is a boon. Unfortunately, bear markets are accompanied by higher unemployment rates. The loss of a job may force some savers to cash in part of their retirement funds to support themselves and their families. Boy, I’m just full of cheery thoughts this week!

After the 2000 peak, stock market prices recovered in 2007, thanks to low interest rates, mortgage and securities fraud. Just as soon as the price rose to the 2000 peak, it fell precipitously during the 2008 Financial Crisis. Finally, in the first months of 2013, stock market prices broke out of the 13-year bear market.

We have seen two peaks, followed by two secular bear markets that lasted thirteen years. The economy is still in the process of building a third peak. Will history repeat itself? Let’s hope not.

May’s annual growth of wages was 2.7%, strengthening but still below the desirable rate of 3%. The work force, and the economy, is only as strong as the core work force aged 25-54. This age group raises families, starts companies, and buys homes. For most of 2017, annual employment growth of the core fell below 1%. It crossed above that level in November 2017 and continues to stay above that benchmark.

Overall, this was a strong report with job gains spread broadly across most sectors of the economy. Mr. Trump, go ahead and take your bow, but put your MAGA hat on first so you don’t mess up your hair.

///////////////////////////////

Executive Clemency

This week President Trump pardoned the filmmaker Dinesh D’Souza, serving a five-year probation after a 2014 conviction for breaking election finance laws. He helped fund a friend’s 2012 Senate campaign by using “straw” contributions. D’Souza complains that he was targeted by then President Obama and General Attorney Holder for being critical of the administration. A judge found no evidence for the claim but if he didn’t see the conspiracy against D’Souza, then he was part of the conspiracy, no doubt. I reviewed the 2016 movie in which D’Souza unveiled the perfidious history of the Democratic Party and its high priestess, Hillary Clinton.