November 3, 2019

by Steve Stofka

Think the days of packaging subprime loans together is gone? Nope. They are called asset-backed securities, or ABS. The 60-day delinquency rate on subprime loans is now higher than it was during the financial crisis (Richter, 2019). The dollar amount of 90-day delinquencies has grown more than 60% above the high delinquencies during the financial crisis. Recently Santander U.S.A. was called out for the poor underwriting practices of its subprime loans. In this case, Santander must buy back loans that go into early default because of fraud and poor standards.

Credit card delinquencies issued by small banks have more than doubled since Mr. Trump took office (Boston, Rembert, 2019). Did a more relaxed regulatory environment encourage these banks to take on more risk to boost profits?

In the last century, geologists have developed new measuring and analytical tools to better understand the structure of the Earth. GPS technology can now detect movements of the earth’s crust as little as ¼” (USGS, n.d.). The same can’t be said for human foolishness. During the past half-century, financial analysts and academics have developed an amazing array of statistical and analytical tools to understand and measure risk. Despite that sophistication, the Federal Reserve has mismanaged interest rate policy (Hartcher, 2006). Government regulators have misunderstood risks in the banking and securities markets.

Earthquake threats happen deep underground. I suspect that the same is true about financial risks. To gain a competitive advantage, companies try to hide their strategies and the details of their financial products. On the last pages of quarterly and annual reports, we find a lot of mysterious details in the notes. After the Arthur Anderson accounting scandal in 2002, the Sarbanes-Oxley Act was passed to bring greater transparency and accountability to financial reporting. Six years later, the financial crisis demonstrated that there was a lot of risk still hiding in dark corners.

The financial crisis exposed a lot of malfeasance and foolishness. Some folks think that investors are now more alert. After the crisis, corporate board members and regulators are more active and aware of risk exposures. Are those risks behind us? I doubt it. Believing in the power of their risk models, underwriters, bankers and traders become victims of their own overconfidence (Lewis, 2015).

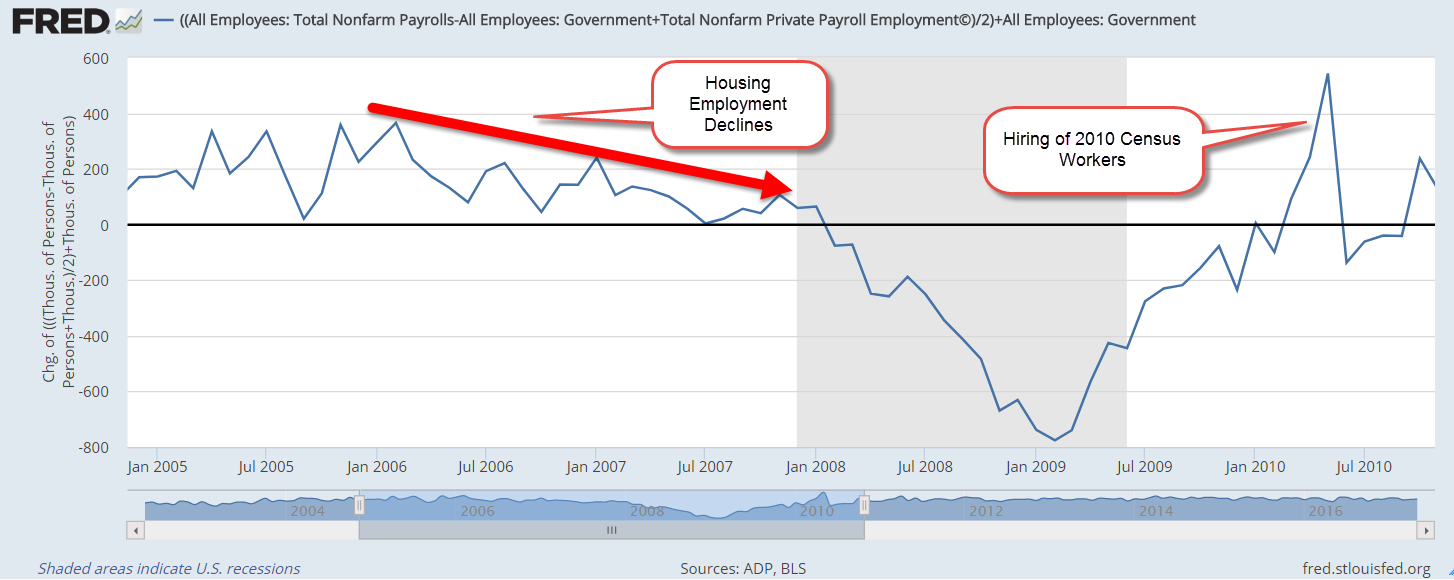

Each decade California experiences a quake that is more than 6.0 on the Richter scale. Following the quake come the warnings that California will split away from the North American continent. Still waiting. The recession was due to arrive eight years ago. We did experience a mini-recession in 2015-16, but it wasn’t labeled a recession. The slowdown wasn’t slow enough and long enough. Eventually we will have a recession, and all those people who predicted a recession in 2011 and subsequent years will claim they were right. In many areas of life, being right is all about timing. Few of us are that kind of right.

The data demonstrates the difficulty of financial fortune telling. The Callan Periodic Table of Investment Returns shows the returns and rank of ten asset classes over the past two decades (Callan, 2019). An asset class that does well one year doesn’t fare as well the following year. An investor who can read the past doesn’t need to read the future. Does an investor need to diversify among all ten asset classes? Many investors can achieve some reasonable balance between risk and reward with four to six index funds and leave their ouija boards in the closet.

///////////////////////

Notes:

Boston, C. and Rembert, E. (2019, October 28). Consumer Cracks Emerge as Banks Say Everything Looks Fine. Bloomberg. [Web page]. Retrieved from https://www.bloomberg.com/news/articles/2019-10-28/consumer-cracks-emerge-as-banks-say-everything-looks-fine

Callan. (2019). Periodic Table of Investment Returns. [Web page]. Retrieved from https://www.callan.com/periodic-table/

Hartcher, P. (2006). Bubble man: Alan Greenspan & the missing 7 trillion dollars. New York: W.W. Norton & Co.

Lewis, M. (2015). The Big Short. New York: Penguin Books.

Richter, W. (2019, October 25, 2019). Subprime auto loans blow up. [Web page]. Retrieved from https://wolfstreet.com/2019/10/25/subprime-auto-loans-blow-up-60-day-delinquencies-shoot-past-financial-crisis-peak

Szeglat, M. (n.d.) Photo of lava flow at Kalapana, HI, U.S. [Photo]. Retrieved from https://unsplash.com/photos/NysO5Rdn7Mc

USGS. (n.d.). About GPS. [Web page]. Retrieved from https://earthquake.usgs.gov/monitoring/gps/about.php