December 15, 2024

by Stephen Stofka

This is fifth in a series of debates on various issues. The debates are voiced by Abel, a Wilsonian with a faith that government can ameliorate social and economic injustices to improve society’s welfare, and Cain, who believes that individual autonomy, the free market and the price system promote the greatest good.

Cain said, “Last week, after our discussion on healthcare, you asked what kind of public good our group likes. Education is a proper role for government.”

Abel asked, “Our group thinks both healthcare and education are public goods. Why do you agree on one and not the other?”

Cain replied, “What’s a public good? Something that benefits an entire group of people but the market undersupplies.”

Abel interrupted, “Like healthcare.”

Cain disagreed, “Education is different than healthcare because learned skills are portable and transferable.”

Abel countered, “Our group would argue that healthy people are more productive. Good health is a transferable skill as well.”

Cain shrugged, “I’ll grant you that. But there’s a difference. Education transforms human beings. Healthcare is restorative. Education can be traced to a source that bears the expense of training. Good health has multiple sources.”

Abel interjected, “Wait. Let me get these distinctions you’re making. Transformative versus restorative. Single source versus multiple source. Ok, got it.”

Cain continued, “There’s a cost benefit paradox. Let’s say a company trains some people at their own expense. In the middle ages and Renaissance, a trade or craft guild trained their apprentices. They controlled advancement to the ranks of journeyman and master and where their guild members worked.”

Abel said, “In the 15th century, London public schools taught students basic reading and math skills so they could be admitted to a trade or craft guild. Even then, education was understood as a role of government.”

Cain replied, “Ok, but even under the guild system, the masters paid their apprentices less to recover the costs of training. Let’s imagine a more modern system where guilds do not dictate where a person can work. An employee learns that they can earn more at a competing company whose business model is hiring trained employees from other companies. The training benefits the employees and the competitor but not the company that does the training. No company wants to train their employees unless everyone does it. That’s an ideal role for government.”

Abel replied, “Ok, so your group acknowledges the role of government in providing education. How much education? Who pays for that expense? Those are policy decisions that are outside the price system.”

Cain nodded. “How much meaning how many years? Grade school, high school, college?”

Abel replied, “Yes. I would include trade schools.”

Cain said, “Our group advocates for school choice, a voucher system that allows parents to decide what school is best for their children. Our K-12 system was designed in the 19th century when many parents had little formal education and could not evaluate a school’s practices. That is no longer true.”

Abel argued, “That approach can lower standards. Schools would learn to cater to parents. For instance, a high school might offer a diploma without the need to take geometry or algebra class. A parent whose child was not good in math would be attracted to such a school.”

Cain replied, “There would have to be some standards, of course.”

Abel responded, “But setting standards requires a governing body to set those standards. How are those people appointed? Are they elected? Again, the price system cannot achieve a desired allocation of resources.”

Cain shook his head. “Sure, there will be parents who game the system, but they will be a small minority. Don’t use those few to invalidate an entire framework.”

Abel said, “It’s not just a few. During the 1980s, some online colleges became ‘diploma mills’, enabling students to acquire diplomas with little effort. In some fields like the law, a diploma is a credential that enables a person to get a license to practice the law. That diploma is a direct factor of production. In the humanities, a diploma can be more of a signaling device. In markets like that, the price system invites abuse.”

Cain nodded. “I’ll grant you there is a need for standards.”

Abel continued, “Many of the products we consume are subject to standards that were set by some governing body over a century ago. In the 19th and 20th century, groups like yours with libertarian sentiments opposed such standards.”

Cain said, “OK, I get your point. Our point is that such intervention, which is subject to political ideologies and alliances, should be kept to a minimum.”

Abel replied, “A college certification or degree is not an electrical appliance that can be easily tested. Some trade certifications are only awarded after a hands-on or clinical test. But some disciplines like sociology have no testable application. In that case, only the rigor of the curriculum can be evaluated. A school must submit its curriculum to an accrediting body.”

Cain said, “An who evaluates the accrediting body? The Department of Education. Some advocacy organizations like Veterans Education Success have questioned the legitimacy of an accrediting agency.”

Abel nodded. “Agreed. There will always be a political element in any market. Your group wants to look at the price system in isolation. It is skeptical of government institutions. Our group sees those institutions as vital to functioning markets as umpires are to the game of baseball. The price system cannot survive without strong government institutions that people respect or at least tolerate. When those institutions seem to be biased to a particular group, they lose credibility, and the price system invites abuse.”

Cain replied, “Let’s agree that a market is like a game. It needs some governing body to set the rules, and it needs umpires or referees to make sure players abide by the rules. Our group opposes government agencies setting rules to force a particular outcome. Baseball fans are used to it. The dimensions of the strike zone are changed to advantage batters and promote higher scoring games. That’s fine for an entertainment sport like baseball. It’s not fine for the private economy. Regulators might change the rules to promote a more equal distribution of income. The people who are attracted to government are attracted to power. A rule change is like pulling a big lever on the economic machine.”

Abel shook his head. “There you go again. Your group assumes that people in the market have benign self-serving intentions. You assume that people in government, on the other hand, have suspicious motives. They are villains twirling their long moustaches and plotting the end of a free republic.”

Cain laughed. “There are few adaptable constraints on their behavior. We are not saying that people in the private market are saints. Adam Smith’s point about the invisible hand was that the sum of individual self-serving action promoted an overall good. Each of us serving our own needs acts as a constraint on others.”

Abel interjected, “Adam Smith also pointed out that businessmen were constantly colluding to subvert the price system and the public good.”

Cain nodded. “Fair enough. My point is that politics is a dangerous game because there are so few players. The Constitution specifically gives the House and Senate the ability to set their own rules. State and federal legislatures regularly change those rules to promote their own party power. Gerrymandering congressional districts is an example of changing the dimensions of the strike zone. They change the rules to achieve a specific outcome.”

Abel said, “In the cause of promoting higher education for everyone, policymakers want to change the rules to give everyone a chance at a higher education. That includes funding for school and guidelines that promote more diversity on campus.”

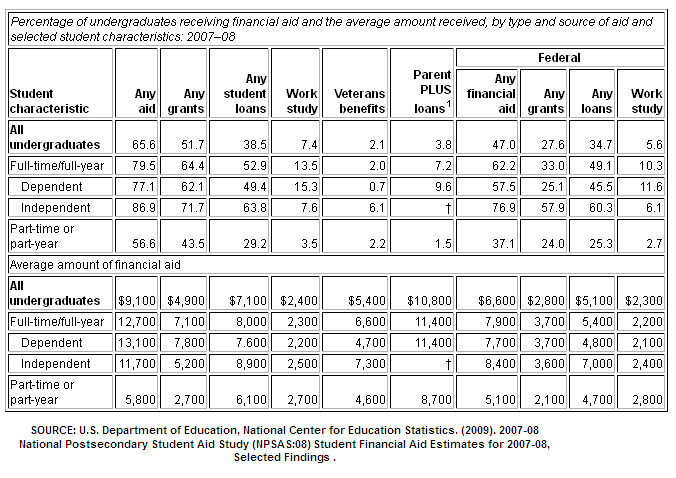

Cain argued, “Like everything else government touches, they make the process of getting financial aid complicated. Many parents and students need help with the labyrinth of information and regulation that the financial aid form – FAFSA – requires.”

Abel replied, “The Department of Education needs to assess the financial need of each student. They want to make sure that a student from a high-income family is not tapping the pool of funds that could be helping a student from a low-income family.”

Cain said, “That’s the problem with needs-based frameworks. Some government agency has to assess a student’s need. Imagine if a restaurant owner charged different prices for a meal based on their customers’ incomes.”

Abel shook his head. “An education is not a restaurant meal. At any rate, colleges and universities usually publish the same price per semester. Based on ability and financial need, a student gets scholarships or grants. If you want to use the restaurant meal analogy, those grants are like having a discount coupon off a meal. The complicated part is figuring out who gets the coupons and how much the coupons are worth. Your group doesn’t like complications.”

Cain replied, “In our economic system, students are aspiring suppliers of skills and knowledge to the marketplace. They attend college to acquire those skills and knowledge. The schools should supply them with those skills and relevant knowledge. I emphasize the word ‘relevant’. The government’s role is not to fund teachers spreading their Marxist ideologies or to be an advocate for gay issues.”

Abel argued, “Students in a sociology class might be interested in a career as a law enforcement officer, public administration or the practice of law. The treatment of gay people in different cultural backgrounds would provide helpful background in their jobs. Remember the 80-20 rule. We use only 20% of what we learn in school to do our job. The other 80% enables us to understand that 20% we do use.”

Cain nodded. “Professors are there to present information, not their normative perspective. They take advantage of students who are at an impressionable age. Too many professors treat the classroom as their personal pulpit. The taxpayers shouldn’t be funding some professor’s personal political religion.”

Abel shook his head. “Taxpayers help fund Christian Colleges and Bible Colleges. Are you suggesting that the government should support some perspectives and censor others?”

Cain said, “Our group believes that states and local communities should have more of a say in how their taxes are spent.”

Abel replied, “Alaska and Rhode Island receive the most in federal grants on a per-capita basis. Residents of New York and California pay the most in taxes. Should taxpayers in New York City have a say in how Alaska spends its federal grants? We are a republic of fifty states. Our finances are interconnected and that creates conflicts in our common and individual interests. Governing those diverse interests makes it difficult to apply a cohesive set of principles.”

Cain argued, “Transparent principles are essential to good governance. Discretionary public policy invites abuse and corruption.”

Abel nodded, “James Madison, the primary architect of the Constitution, thought that conflicts in regional interests would cause the nation to fracture and fail. As rigid as the Constitution is, we keep patching the contracts and alliances that form our union.”

Cain threw up his hands. “We seem no closer to an agreement on education policy.”

Abel replied, “The path to compromise is paved with disagreements.”

Cain nodded. “We’ll talk next week.”

Abel said, “See you then.”

/////////////////////

Photo by The Oregon State University Collections and Archives on Unsplash

A comparison of training done in medieval guilds with the current university system. https://onlinelibrary.wiley.com/doi/full/10.1111/hequ.12305

In 15th century London, public schools taught basic reading and arithmetic skills which were necessary for admittance to the guilds. https://www.thoughtco.com/medieval-child-the-learning-years-1789122

A history of “diploma mills” https://en.wikipedia.org/wiki/Diploma_mills_in_the_United_States. Veterans Education Success advocates for veterans in higher education. Here is a complaint they filed with the Department of Education https://vetsedsuccess.org/our-letter-to-the-department-of-education-on-hlc/